On one side, Amazon (AMZN) is pouring nearly $200 billion into capital expenditures, doubling down on AI chips, cloud infrastructure, satellites, and ultra-fast delivery. On the other, Walmart (WMT) just crossed $700 billion in annual sales, is gaining share from higher-income households, and is turning advertising and memberships into powerful profit engines. Both are investing heavily in artificial intelligence (AI) and expanding their business at a rapid pace.

But if you are buying one stock to hold for the next decade, one has the stronger long-term case.

Let’s break it down.

The Bull Case for Amazon

Over the last ten years, Amazon stock has returned 622%. And while Amazon started its journey as an e-commerce giant, it has now evolved into a technology-powered growth engine fueled by cloud computing, AI, advertising, and logistics innovation.

In the most recent fourth quarter, Amazon reported $213.4 billion in revenue, up 12% year-over-year (YOY), with $25 billion in operating income. Net income rose 4.8% to $1.95 per share. On the retail side, the everyday essentials segment grew nearly twice as fast as other categories in the U.S., and Amazon delivered nearly 70% more same-day items YOY. Prime members enjoyed the exclusive benefits and received over eight billion same- or next-day items in the U.S. in 2025.

However, Amazon’s real story isn’t retail anymore; it’s Amazon Web Services. Notably, AWS revenue grew 24% YOY, reaching a $142 billion annualized run rate. Management emphasized that this growth is happening on a massive base, adding more incremental revenue than competitors. For the quarter, AWS added $2.6 billion in revenue and nearly $7 billion for the year. Management boasted that AWS added more data center capacity in 2025 than any other company globally. In the global cloud computing market, AWS maintains its leading position with a 28% market share. Additionally, its chips business (Graviton and Trainium) is now at a $10 billion plus annual revenue run rate, growing triple digits.

The $200 billion in capital expenditure in 2026 is intended mainly for AWS due to the massive demand.

“Customers really want AWS for core and AI workloads. And we are monetizing capacity as fast as we can install it,” management stated on its most recent earnings call.

Beyond cloud, Amazon’s advertising division brought in $21.3 billion in fourth-quarter revenue, marking a 22% increase from the prior year. Meanwhile, Prime Video’s ad-supported audience has expanded to 315 million viewers worldwide. In addition, Amazon introduced Alexa Plus and continues development on Amazon LEO satellite connections, with 180 satellites launched and a commercial rollout planned for 2026.

Analysts anticipate that Amazon's earnings will climb by 8.5% to $7.78 per share in 2026, followed by a 19.6% increase in 2027. Despite its growth profile, cloud dominance, and AI-driven goals, Amazon stock remains reasonably valued, trading at 27.45 times forward earnings.

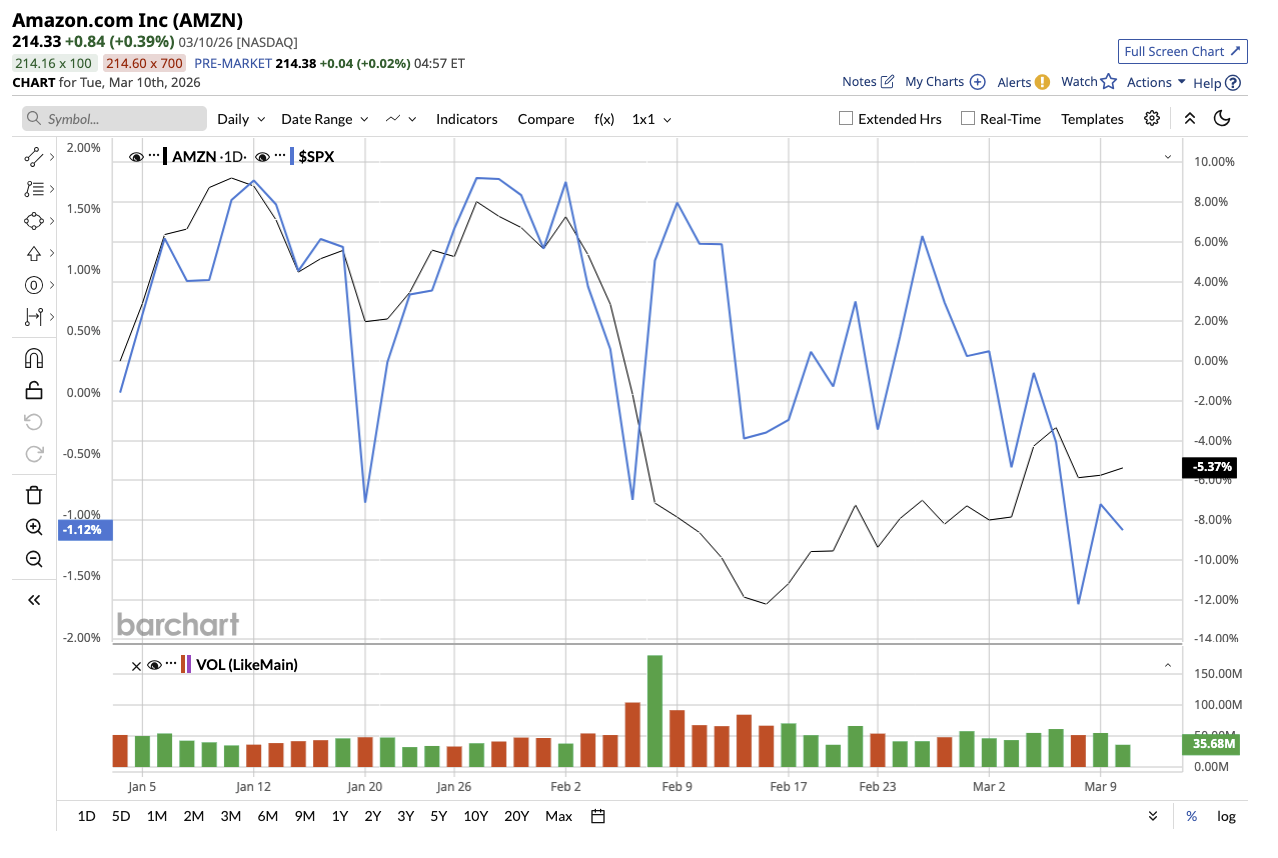

AMZN stock is down 7.87% year-to-date (YTD), compared to the S&P 500 Index ($SPX) dip of 1%. Nonetheless, Wall Street forecasts the stock surging 34% from current levels if it hits its mean target price of $284.75. Plus, its high target price of $360 implies an upside potential of 69% over the next year.

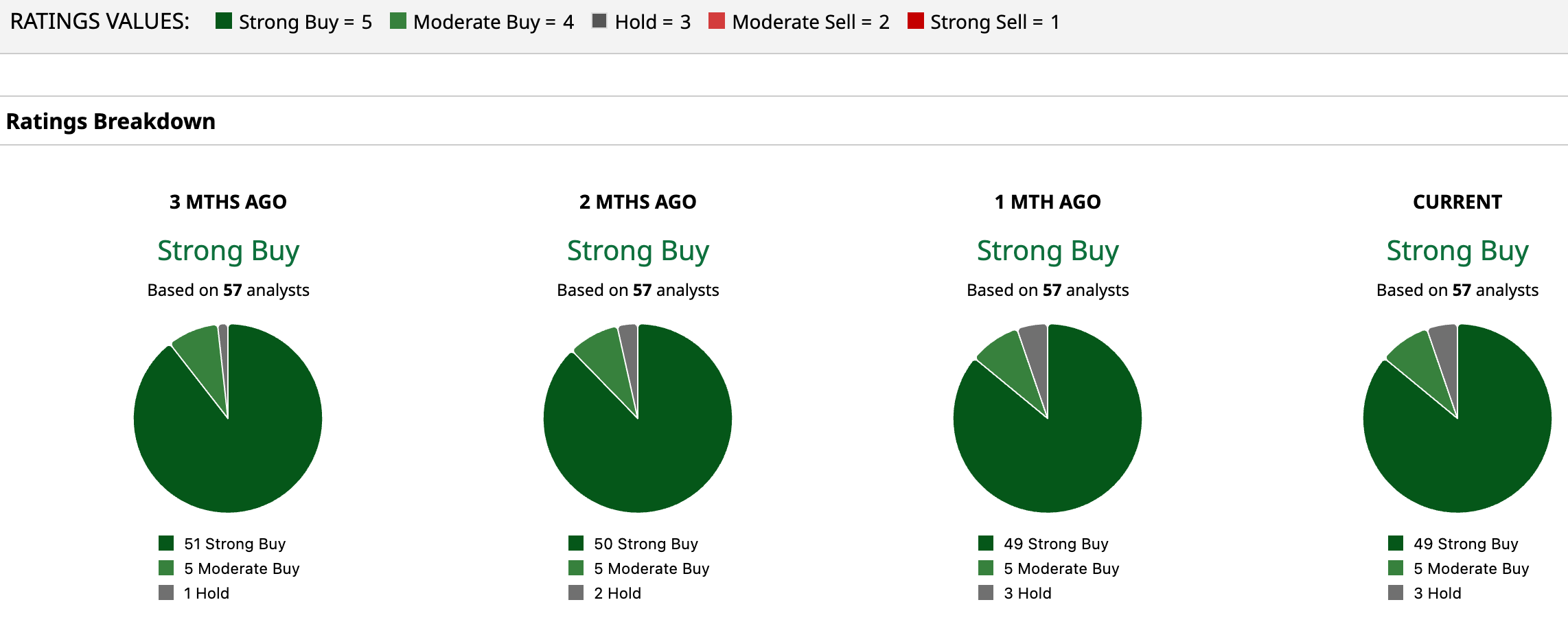

Overall, Wall Street is strongly bullish about Amazon stock. Of the 57 analysts covering the stock, 49 rate it a “Strong Buy,” five say it is a “Moderate Buy,” and three rate it a “Hold.”

The Bull Case for Walmart

In the past decade, Walmart stock has returned 448.05%, and it remains the largest U.S. retailer, with unmatched physical scale. With over 10,900 stores worldwide and a presence in 19 countries, Walmart serves roughly 280 million customers weekly.

While margins are lower than Amazon’s cloud business, Walmart offers something Amazon doesn’t. It thrives even during economic downturns, with its defensive grocery business and pricing power during inflation. Growing steadily but at a slower pace, WMT is driven mostly by same-store sales, e-commerce expansion, and membership programs.

In the fourth quarter, total revenue grew 4.5% with 10.5% growth in adjusted operating income. For the full year, Walmart surpassed $700 billion in total revenue. Adjusted earnings rose 12.1% in Q4 and 5.2% for the full year to $2.64 per share. Digital sales exceeded $150 billion, contributing 23% to total revenue. One of the biggest shifts in Walmart’s model is the rise of higher-margin revenue streams such as advertising and membership. Advertising sales totaled $6.4 billion for the year, while membership income increased by more than 15%. This diversification minimizes reliance on low-margin retail sales.

Also, Walmart is actively using AI across multiple parts of its business. It has partnered with OpenAI to let customers shop directly through AI chat interfaces like ChatGPT, enabling conversational purchasing and instant checkout. And, it's using AI to manage inventory more efficiently and improve logistics across its stores and distribution centers globally.

One of Walmart’s key characteristics is that it is a reliable dividend stock. By paying and increasing dividends for 52 years, Walmart is now part of the elite group of “Dividend Kings.” Recently, the company increased its annual dividend by 5% to $0.99 per share for fiscal 2027. For conservative investors, this dividend stability gives a defensive exposure during volatile times.

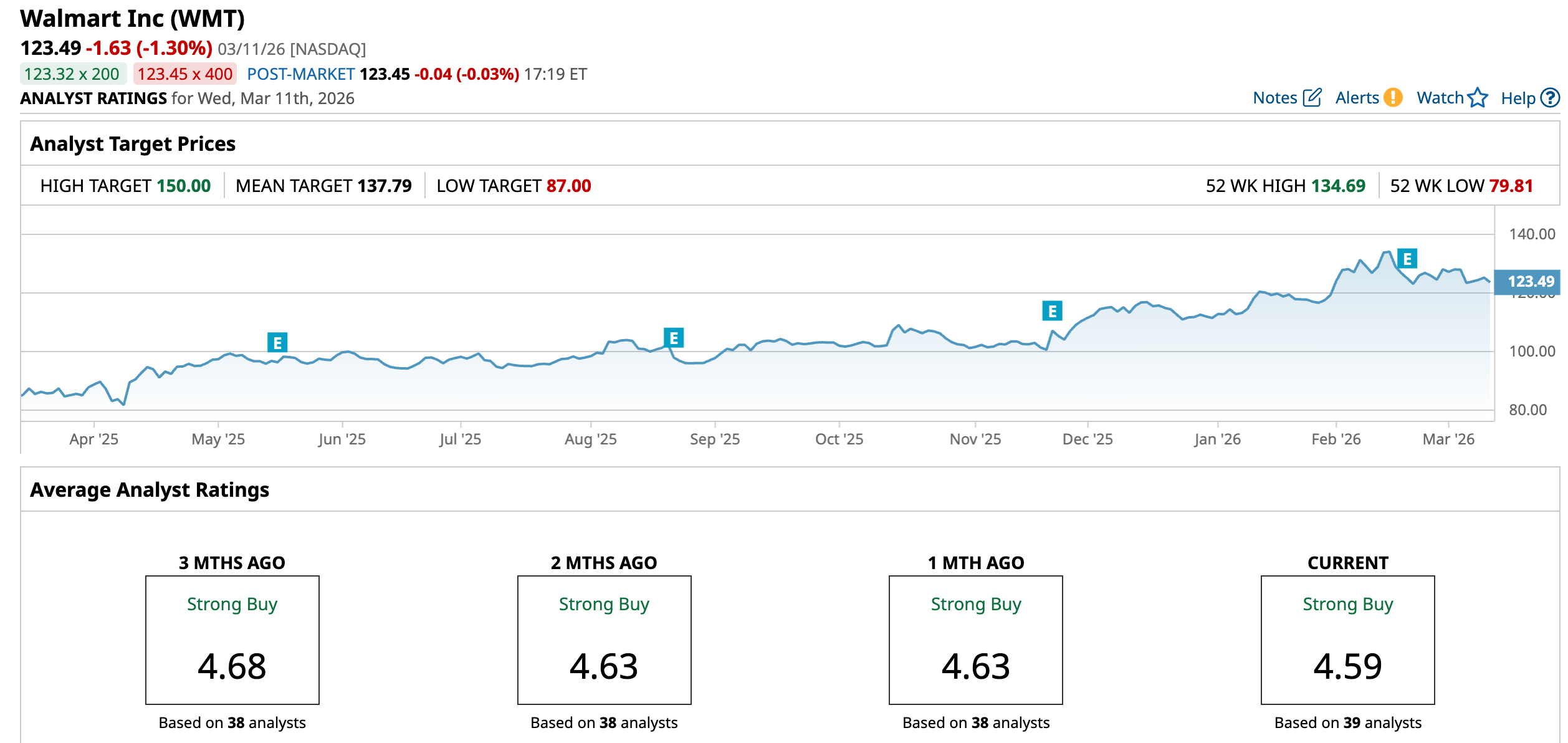

Analysts predict a 9.5% increase in earnings to $2.89 per share in fiscal 2027, followed by a 12.8% increase in fiscal 2028. Valued at 43.02 times forward earnings, WMT is trading at a premium now.

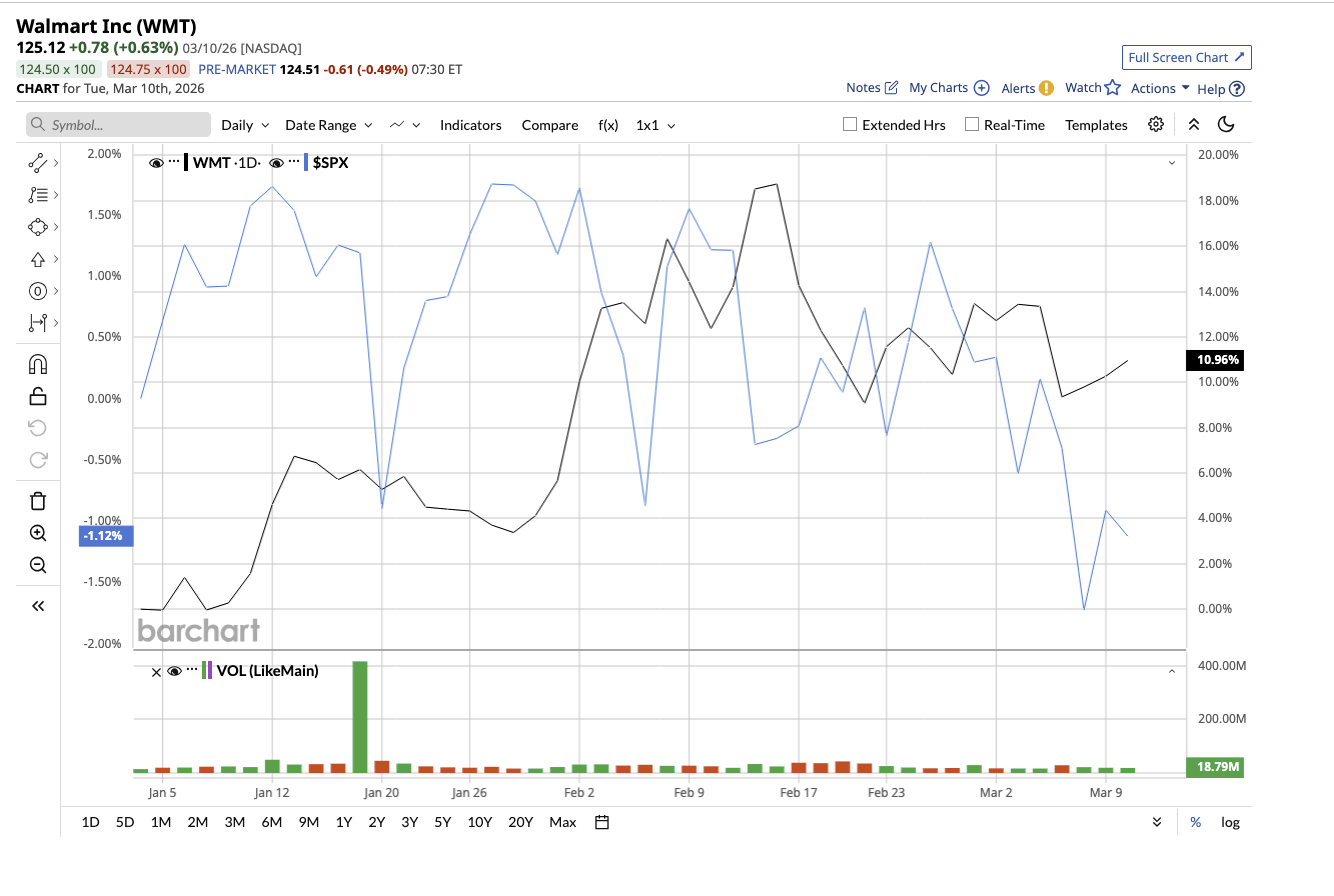

WMT stock is up 10.84% YTD, outperforming the overall market. Wall Street forecasts the stock surging 11.58% from current levels if it hits its mean target price of $137.79. Plus, its high target price of $150 implies an upside potential of 21.47% over the next year.

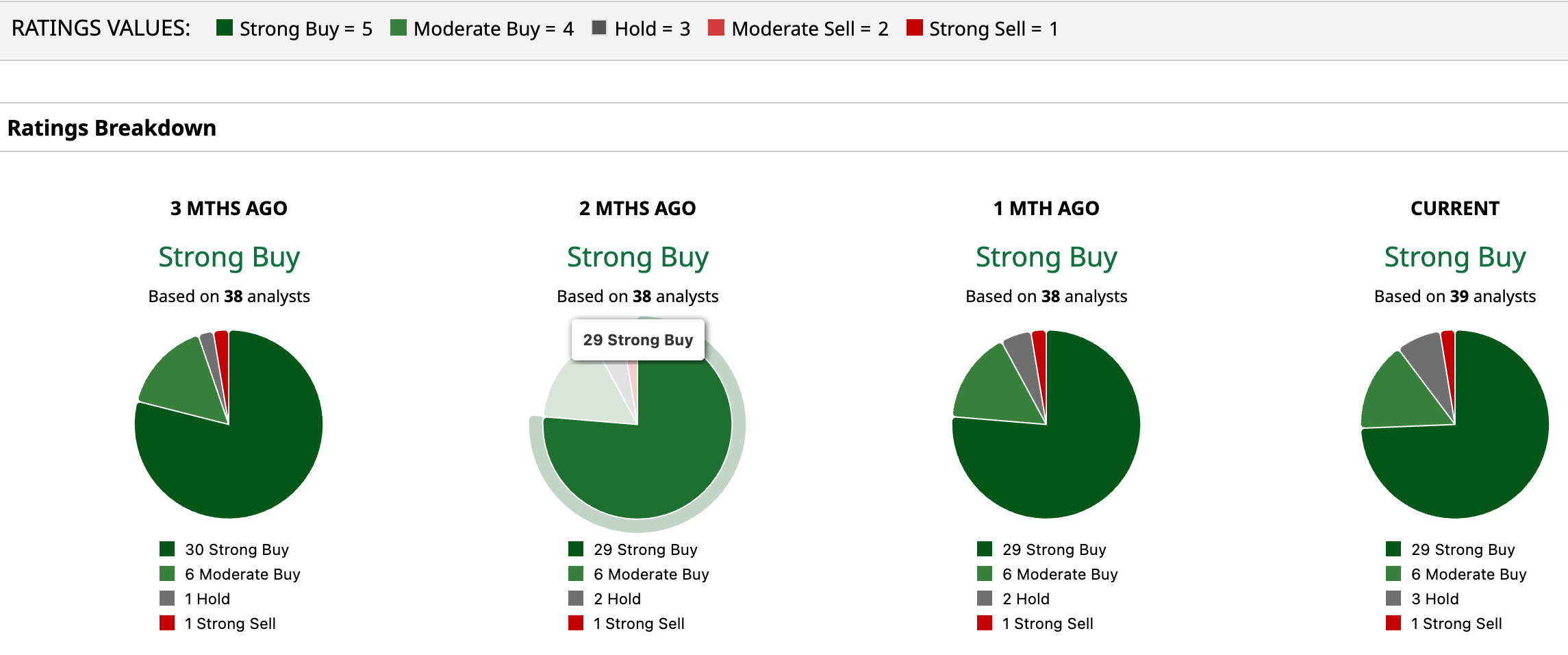

Overall, Wall Street is strongly bullish about Walmart stock. Of the 39 analysts covering the stock, 29 rate it a “Strong Buy,” six say it is a “Moderate Buy,” three rate it a “Hold,” and one says it is a “Strong Sell.”

Which is the Better Buy?

In a diversified portfolio, both stocks fit well, as Amazon is the growth compounder while Walmart is the defensive giant. But if forced to choose one for the next decade, I would lean toward Amazon. If AI spending and cloud infrastructure remain powerful secular trends, Amazon’s scale in AWS, custom silicon, and high-margin advertising gives it a structural edge.

For investors willing to tolerate volatility in exchange for multiple long-term growth engines, Amazon offers the stronger return potential over the next ten years.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart