As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the payment processing industry, including Fiserv (NASDAQ: FISV) and its peers.

Payment processors facilitate transactions between merchants, consumers, and financial institutions. Growth comes from e-commerce expansion, declining cash usage globally, and value-added services beyond basic processing. Headwinds include margin pressure from merchant negotiating power, rapid technological change requiring investment, and emerging competition from technology companies entering the payments ecosystem.

The 4 payment processing stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 49.7% below.

In light of this news, share prices of the companies have held steady as they are up 1.2% on average since the latest earnings results.

Fiserv (NASDAQ: FISV)

Powering over 1 billion accounts and processing more than 12,000 financial transactions per second globally, Fiserv (NASDAQ: FISV) provides payment processing and financial technology solutions that enable merchants, banks, and credit unions to accept payments and manage financial transactions.

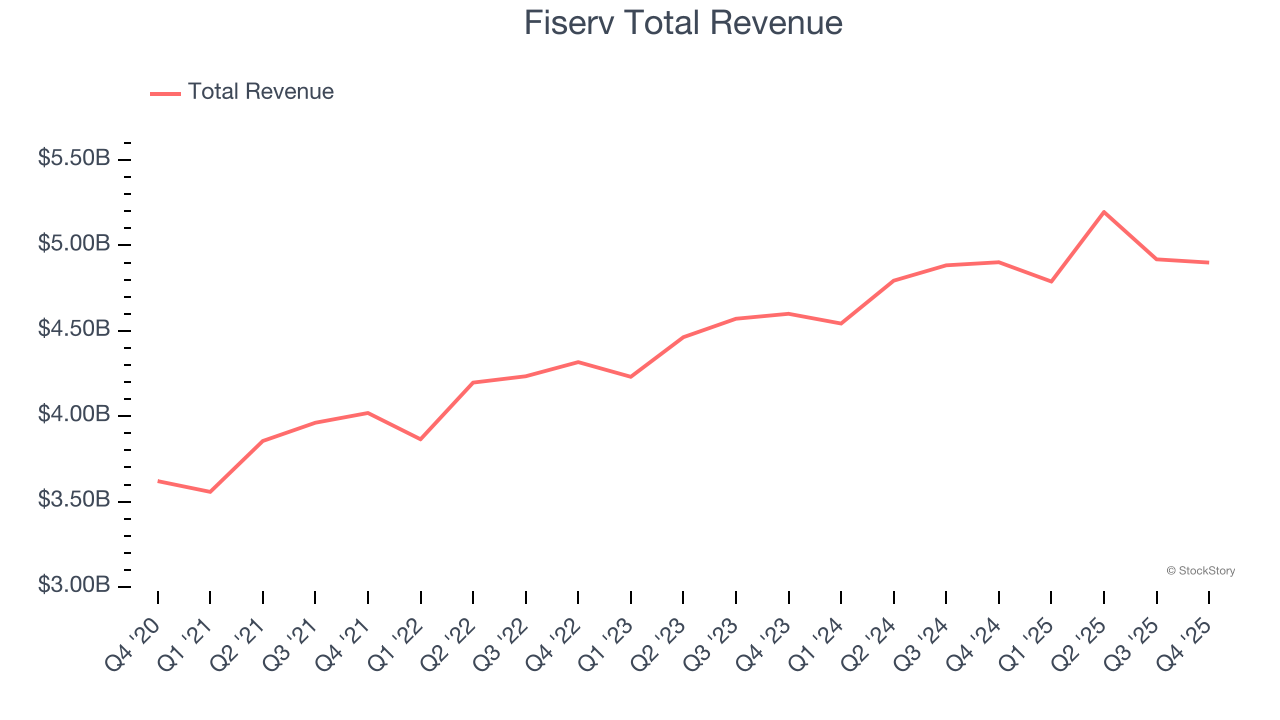

Fiserv reported revenues of $4.9 billion, flat year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with a decent beat of analysts’ EBITDA estimates but full-year EPS guidance meeting analysts’ expectations.

“During the fourth quarter, which marked the first full quarter executing the One Fiserv plan, the team took decisive steps and achieved several meaningful milestones and client wins, while also delivering performance in line with our expectations,” said Mike Lyons, Chief Executive Officer of Fiserv.

Fiserv delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. Interestingly, the stock is up 4.3% since reporting and currently trades at $62.72.

Read our full report on Fiserv here, it’s free.

Best Q4: EVERTEC (NYSE: EVTC)

Operating one of Latin America's leading PIN debit networks called ATH, EVERTEC (NYSE: EVTC) is a payment transaction processor and financial technology provider that enables merchants and financial institutions across Latin America and the Caribbean to accept and process electronic payments.

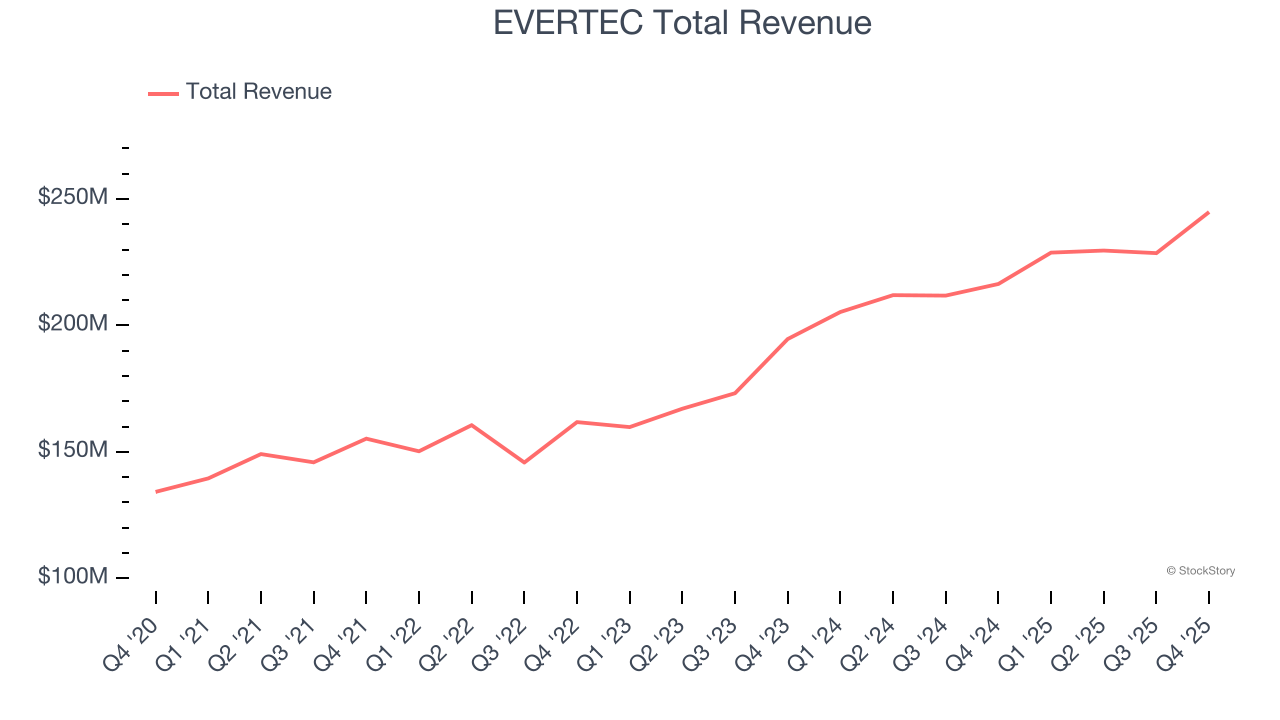

EVERTEC reported revenues of $244.8 million, up 13.1% year on year, outperforming analysts’ expectations by 3.3%. The business had a very strong quarter with full-year revenue guidance exceeding analysts’ expectations and full-year EPS guidance exceeding analysts’ expectations.

EVERTEC achieved the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 11.9% since reporting. It currently trades at $28.83.

Is now the time to buy EVERTEC? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Shift4 (NYSE: FOUR)

Starting as a payment gateway provider in 1999 and now processing over $200 billion in annual payment volume, Shift4 Payments (NYSE: FOUR) provides integrated payment processing solutions and software that help businesses accept and manage transactions across in-store, online, and mobile channels.

Shift4 reported revenues of $1.19 billion, up 34% year on year, in line with analysts’ expectations. It was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EPS guidance meeting analysts’ expectations.

Shift4 delivered the fastest revenue growth but had the weakest full-year guidance update in the group. As expected, the stock is down 13% since the results and currently trades at $49.88.

Read our full analysis of Shift4’s results here.

Jack Henry (NASDAQ: JKHY)

Founded in 1976 by two entrepreneurs who saw the need for specialized banking software in the early days of financial computing, Jack Henry & Associates (NASDAQ: JKHY) provides technology solutions that help banks and credit unions innovate, differentiate, and compete while serving the evolving needs of their accountholders.

Jack Henry reported revenues of $611.2 million, up 6.7% year on year. This print beat analysts’ expectations by 1.3%. It was a very strong quarter as it also put up a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Jack Henry achieved the highest full-year guidance raise among its peers. The stock is up 1.5% since reporting and currently trades at $168.70.

Read our full, actionable report on Jack Henry here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.