What a fantastic six months it’s been for Dillard's. Shares of the company have skyrocketed 69.7%, hitting $600.08. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Dillard's, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Is Dillard's Not Exciting?

We’re glad investors have benefited from the price increase, but we're swiping left on Dillard's for now. Here are three reasons there are better opportunities than DDS and a stock we'd rather own.

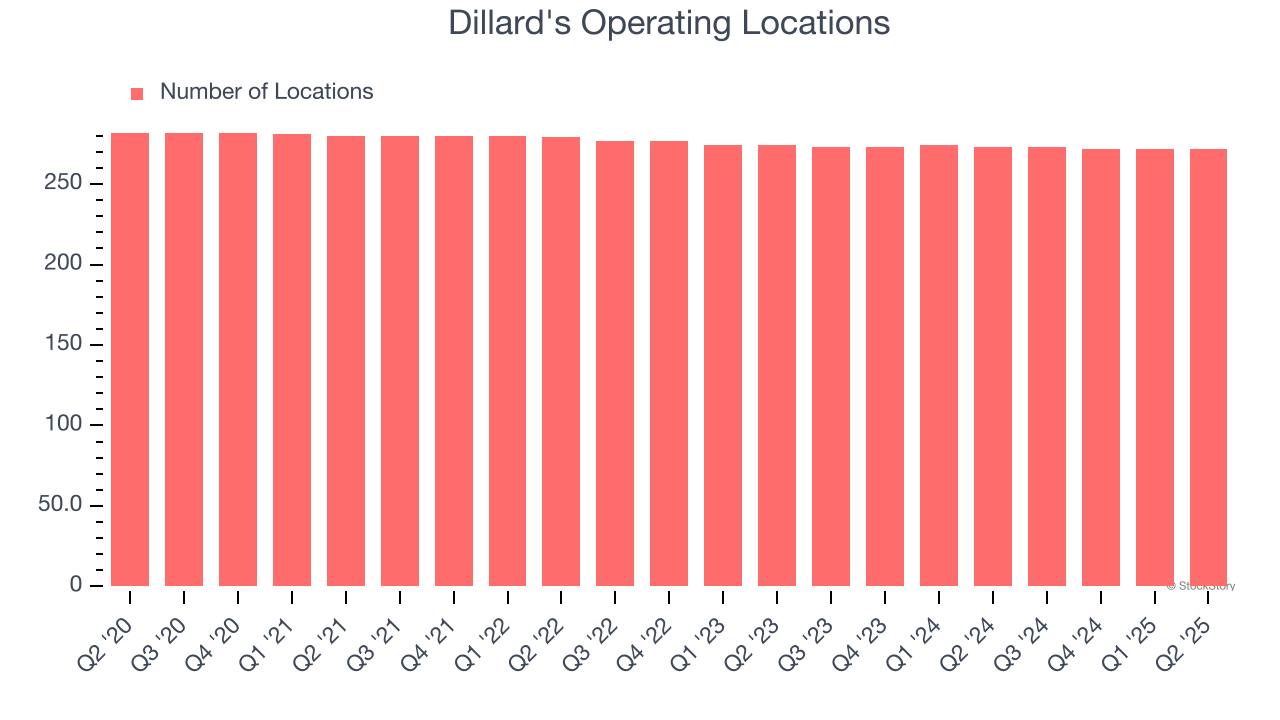

1. Lack of New Stores, a Headwind for Revenue

A retailer’s store count often determines how much revenue it can generate.

Dillard's listed 272 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

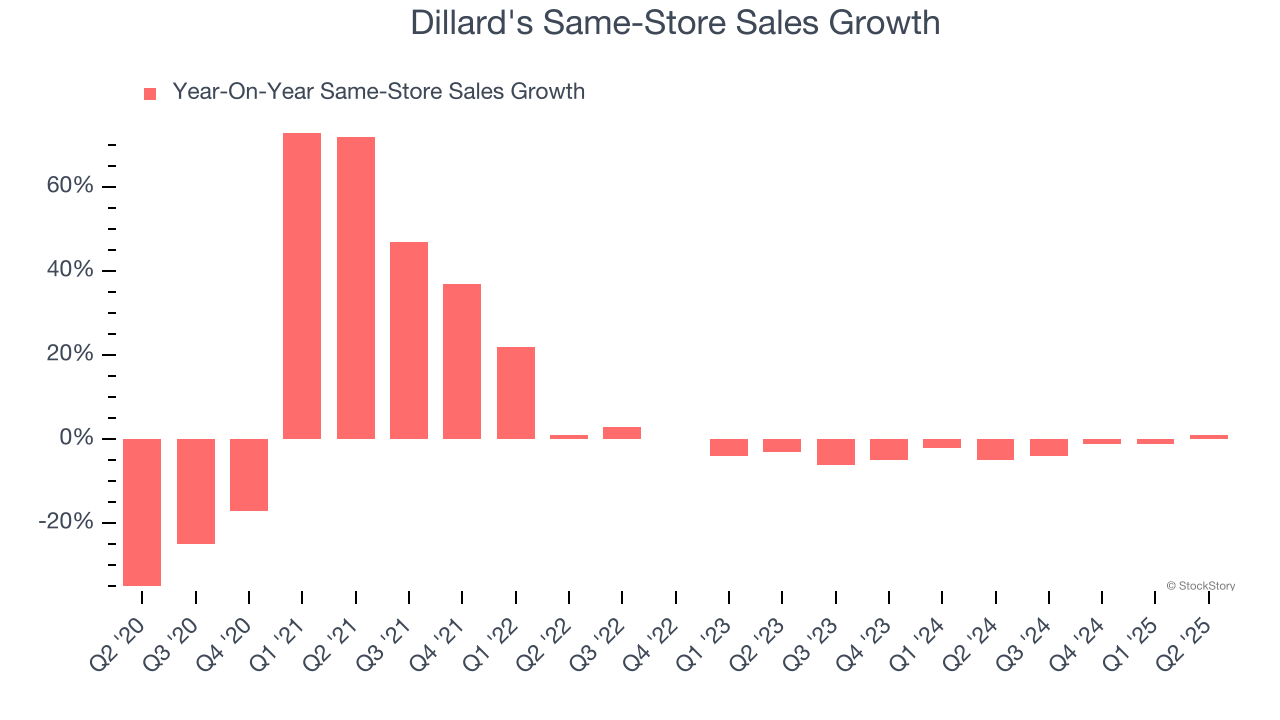

2. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Dillard’s demand has been shrinking over the last two years as its same-store sales have averaged 2.9% annual declines.

3. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Dillard’s revenue to drop by 2.1%, a decrease from This projection is underwhelming and suggests its products will face some demand challenges.

Final Judgment

Dillard’s business quality ultimately falls short of our standards. Following the recent rally, the stock trades at 21.8× forward P/E (or $600.08 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than Dillard's

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.