It’s been a volatile start to Q4 for the Gold Miners Index (GDX) with the gold price (GLD) crashing down through the psychological $1,800/oz level last week. The sell-off has been exacerbated by uncertainty surrounding future stimulus, which was expected earlier this quarter, and may not come until early next year.

However, for investors hoarding cash to prepare for some deals in the sector, we’ve finally seen some deals show up in the sector over the past week. One way to play the sector is through the GDX, which holds a basket of over 60 miners, but with over 30 high-cost producers in the index, one can be diluted by the laggards. The better way to play the index is the individual names, but it’s key to focus on which have the best margins and strongest earnings going forward. Let’s take a look at a few standout names below:

(Source: TC2000.com)

The three miners we’ll cover today are all million-ounce producers with predominantly Tier-1 and Tier-2 operating jurisdictions, making them relatively safe in a world where jurisdiction is becoming more important each year. This is because we’ve seen countries like the Philippines shut down operations, countries like Africa continue to increase government royalties on projects and be subject to violent attacks, and countries like Greece that have a history of nationalization.

Fortunately, Newmont (NEM), Agnico Eagle (AEM), and Gold Fields (GFI) all have more than 40% of their production coming from Tier-1 jurisdictions, with Agnico Eagle being the leader with more than 80% of its production coming from solely Canada and Finland. However, the most exciting part about these companies is their earnings growth, with average annual earnings per share growth of over 85% for these 3 names. Let’s begin with AEM below.

(Source: YCharts.com, Author’s Chart)

For those unfamiliar, Agnico Eagle is one of the premier gold producers in the sector with operations in Canada, Finland, and Mexico. The company is on track to produce just over 1.70~ million ounces of gold this year despite temporary shutdowns in Q2 related to COVID-19 and generated near-record revenue of $981~ million last quarter. This significant jump in revenue combined with increasing margins due to a higher gold price and moderate production growth as new projects come online has set the company up for massive annual EPS growth going forward.

As shown in the chart above, AEM saw minimal progress in annual EPS for several years as the gold price worked its way out of a devastating bear market between 2012 and 2017. However, with all of AEM’s mines firing on all cylinders and a near-record gold price in FY2020, AEM is on track to more than double earnings this year ($2.02 vs. $0.96). This is great news and certainly deserves praise, but FY2020’s earnings are now in the rear-view mirror with us entering the month of December.

However, what is noteworthy is the FY2021 annual EPS estimates which are currently sitting at $4.08. Assuming AEM can hit these forecasts, this would translate to two consecutive years in a row of triple-digit annual EPS growth, making AEM a top-100 growth stock on the US Market. While the stock has had a nice run the past week after finding a low near $60.00, I would expect any pullbacks below the $65.00 to be buying opportunities as the stock would dip below 16x FY2021 annual EPS estimates.

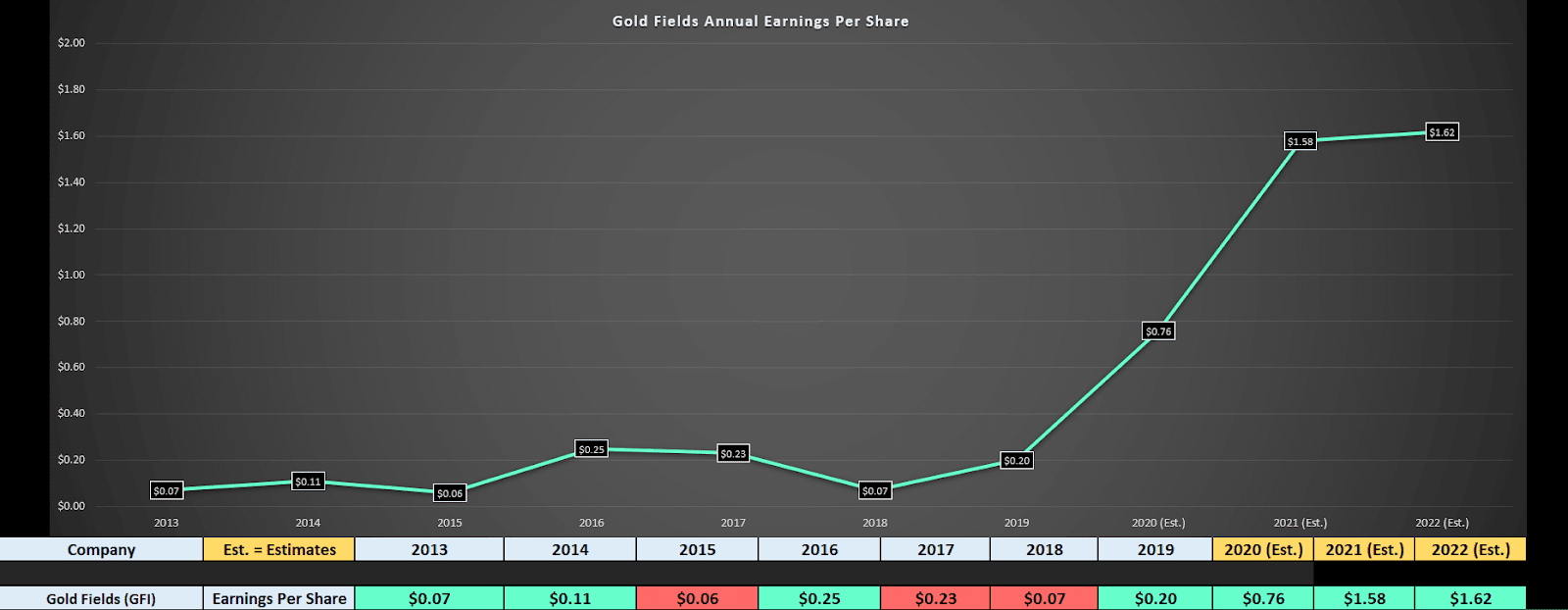

(Source: Gold Fields Company Presentation)

The next name on the list is Gold Fields, and the company is a little riskier as it's got some of its mines in less desirable locations like West Africa, South Africa, and Peru. However, more than 40% of the company's production comes from the #1 mining jurisdiction in the world (Australia), and the company is currently building a new mine in Chile, another Tier-1 operating jurisdiction.

The Chilean project that's under construction is a game-changer for the company, with Salaries Norte set to produce over 400,000 ounces of gold per year for its first five years at costs below $550/oz. This would lead to a massive increase in Gold Fields' margins, with the company's current costs coming in above $950/oz. Early estimates for FY2023 annual EPS once Salares Norte is online are sitting at $2.00, a significant boost from the $0.76 estimates for FY2020.

(Source: YCharts.com, Author’s Chart)

However, for investors who don’t have two years to wait, it’s worth noting that the growth over the next two years is expected to be exceptional. As shown above, Gold Fields is set to report a year with 270% annual EPS growth ($0.76 vs. $0.20), and FY2021 annual EPS estimates are sitting at $1.58 due to the improving margins the company is enjoying. Based on a share price of $9.00, the company is trading at a dirt-cheap valuation of less than 6x forward earnings while paying a 2% yield. This is one of the most compelling valuations in the sector currently, suggesting that the stock is a steal below $9.00.

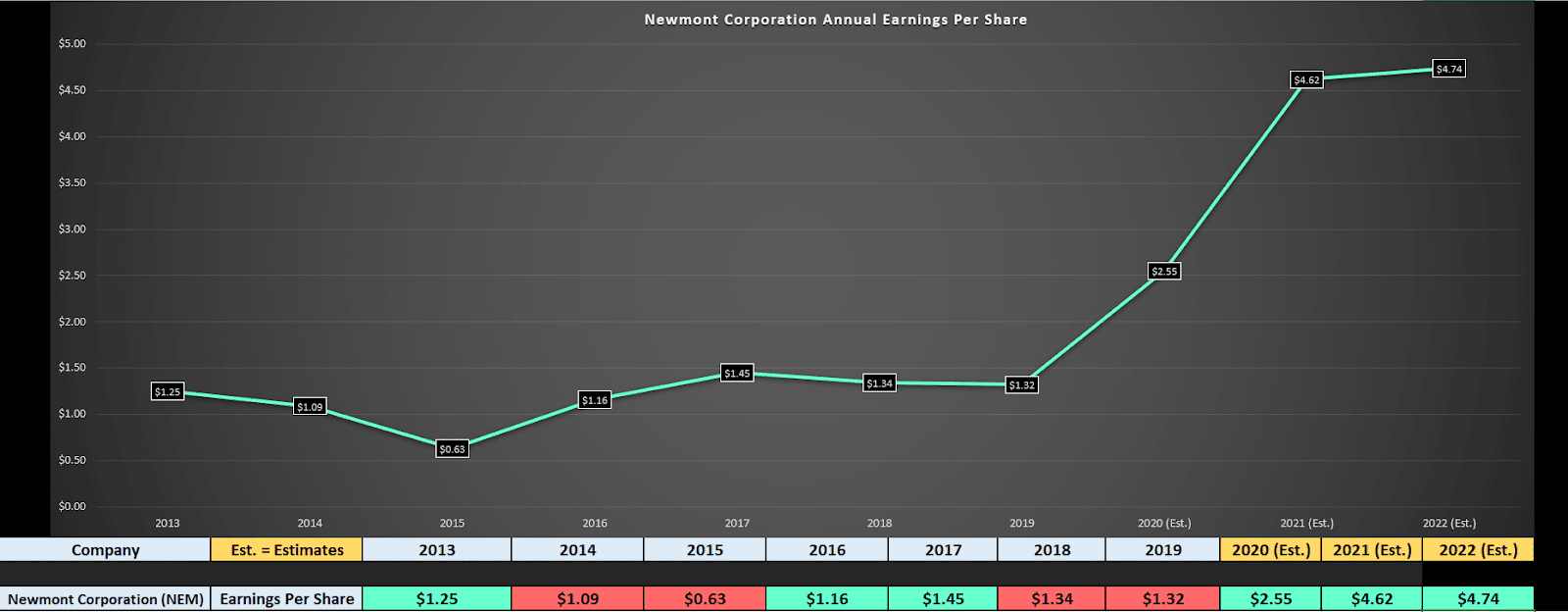

(Source: Locata.com, Newmont Gold)

The final name on the list is Newmont Corporation, one of the world’s top-3 gold producers. The company boasts one of the highest yields in the sector currently, with a dividend yield of 2.70%, almost double the dividend yield of the S&P-500 of 1.60%. However, while the company is certainly high on most value lists after the recent correction from $73.00 - $57.00, it’s just as impressive from a growth standpoint. As shown below, NEM is on track to nearly double annual EPS in FY2020 ($2.55 vs. $1.32) thanks to well-timed share buybacks last year and near-record gold prices.

However, FY2021 annual EPS estimates are sitting at $4.62 on average, suggesting the stock is ready to grow annual EPS by 80% next year despite lapping a year of triple-digit growth. In a market where it’s hard to find growth at a reasonable price, Newmont certainly checks the boxes at less than 13x FY2021 annual EPS forecasts. However, the company also offers value simultaneously, with a yield of nearly 2.70% ($1.60 per share). While this doesn’t preclude the stock from re-testing its recent lows near $57.00, I believe this is a low-risk area to start a position in the stock below $59.50.

(Source: YCharts.com, Author’s Chart)

The Gold Miners Index rarely offers both growth and value as miners destroyed a significant amount of shareholder value in the past bull market and were forced to suspend their dividends when investors needed them most between 2013 to 2016. However, this new bull market in gold has brought with it stronger and more responsible management teams and a rare opportunity to buy a sector that ranks high on growth and also high on yield at reasonable prices.

While prices got ahead of themselves briefly in August, investors are now offered the opportunity to get in at more reasonable prices with many names trading at above 2% yields with triple-digit earnings growth. Therefore, for investors looking to add an inflation hedge to their portfolios, I believe now is the time to put NEM, AEM, and GFI at the top of one’s shopping list.

Disclosure: I am long NEM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

9 “MUST OWN” Growth Stocks for 2021

NEM shares were trading at $59.51 per share on Thursday afternoon, down $0.45 (-0.75%). Year-to-date, NEM has gained 38.46%, versus a 15.65% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold Miners With Explosive Earnings Growth Potential for Next Year appeared first on StockNews.com