Despite continued chatter of lower rates for longer from the Federal Reserve, the recent waffling on the stimulus bill has led to some volatility in the precious metals space, with the Silver Miners Index (SIL) falling nearly 25% from its August highs. While valuations across the sector are beginning to get more interesting, the key is focusing on quality, as there are over 20 names in the index, and only five are truly worth owning.

The key to hunting down the superior names is looking for those with the highest likelihood of dividend growth, as well as those with annual earnings per share either at or heading to new all-time highs. Currently, there are three names in the sector that fit these criteria, and we’ll take a look at them in a little more detail below:

(Source: TC2000.com)

Many of the speculators in the precious metals space are chasing the lowest-priced names that are yet to build mines as they believe that these will provide the highest reward if the silver price (SLV) does hit $50.00/oz again.

While they may be correct in terms of upside potential, the best reward to risk is in the silver producers as they pay investors to wait, and they are shielded from downside given their earnings power. Currently, Pan American Silver (PAAS), Fortuna Silver (FSM), and Hecla Mining (HL) have one thing in common, and that’s explosive earnings growth.

As of October’s earnings estimates, the average annual EPS growth rate for FY2021 for these three companies is 386%, which dwarfs the sector average annual EPS growth rate of 42%. Therefore, while some of these stocks might look expensive on a trailing P/E basis, they’re actually becoming dirt-cheap after this sell-off on a forward earnings basis. Let’s take a look:

Hecla Mining is one of the few primary silver producers, and it’s one of the only silver producers operating out of only Tier-1 jurisdictions. As those familiar with the silver sector know, the majority of silver mines have a significant base metal component and most of the world’s silver mines lie in either South America or Mexico. Hecla is an exception as it has mines in Alaska, Idaho, and Quebec, and the company is finally turning things around after strikes have been settled at its Lucky Friday Mine in Idaho.

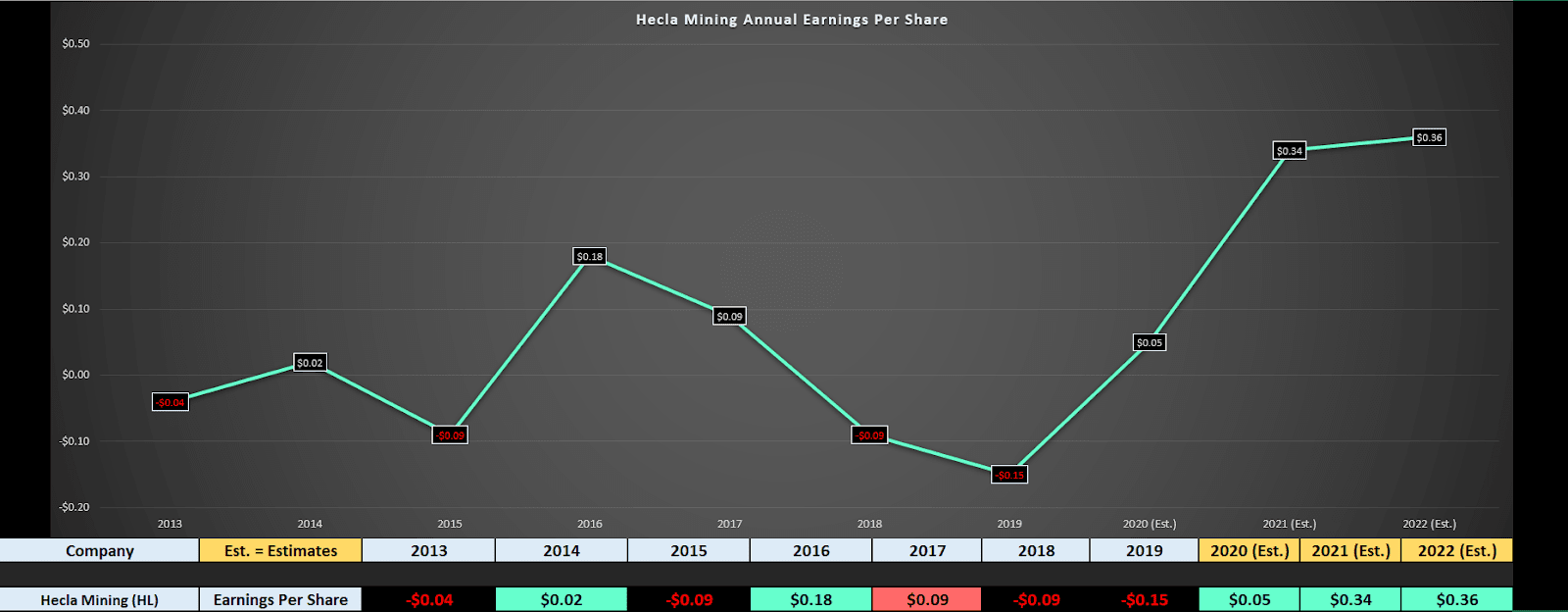

(Source: YCharts.com, Author’s Chart)

As the chart above shows, Hecla Mining’s earnings trend has been dismal for the past decade, though partially affected by the multi-year bear market we saw in silver prices. However, FY2020 is expected to mark a significant improvement in this earnings trend, with FY2021 earnings estimates predicting an earnings breakout for the company.

If we look at FY2020 estimates, they’re currently projected to come in at $0.05, and FY2021 estimates are sitting at $0.34. Based on estimates of $0.05, Hecla Mining looks insanely expensive at a share price of $5.05 with no dividend yield.

However, I would argue that FY2020 estimates are about as stale as it gets with 580% earnings growth expected next year. If we use the FY2021 estimates of $0.34, the stock is trading at a much more reasonable 15x earnings, and would get very interesting below $4.50. Therefore, if we do see some turbulence as we head into the election, I would expect any pullbacks below $4.50 to be a low-risk area to begin nibbling on the stock.

(Source: Hecla Mining Company Presentation)

The next company on the list is Pan American Silver (PAAS), a name that’s had tremendous success and was founded by mining mogul Ross Beaty. Unlike Hecla, Pan American Silver operates out of some less favorable jurisdictions, but the company is one of the only names in the sector paying a dividend (0.60% currently).

Given that the company is reporting record profits and is one of less than 30 companies in the US Market expected to post two consecutive years of triple-digit earnings growth, the company is a must-own in my opinion. Many critics have pointed out that PAAS’ rally this year has left the stock at a lofty valuation, trading at $32.00 vs. trailing earnings of $0.49. However, this is a very strange way to value a company with triple-digit earnings growth.

(Source: YCharts.com, Author’s Chart)

As we can see in the chart above, FY2020 is expected to an earnings breakout year for Pan American Silver, with annual EPS set to hit a new all-time high. Current estimates for FY2020 are sitting at $1.00, projecting 104% growth, and FY2021 estimates are expected earnings to double yet again, with estimates sitting at $2.56. Given that we’re already almost halfway through Q4, it makes little sense to value Pan American based on FY2020 numbers, and investors should instead be placing lots of weight on the FY2021 figures. At a share price of $32.00 and FY2021 estimates of $2.56, PAAS is trading at a very reasonable 12.5x earnings despite a growth rate that dwarfs even the highest-octane growth stocks in the market currently. While this doesn’t preclude further weakness in the stock into the election, I believe any pullbacks below $31.25 would be low-risk buying opportunities.

Last, but not least on the list of silver stocks with explosive growth is Fortuna Silver Mines (FSM), another turnaround story like Hecla Mining (HL). I purposely ignored Fortuna for several years due to a very high capex phase while it completed studies and developed its Lindero Gold Project in Argentina. However, after many delays and a couple of cost overruns that hurt past shareholders, the project has finally come to fruition and poured its first gold.

The new Lindero Mine is projected to produce over 130,000 ounces of gold per year at costs below $900/oz, which translates to 50% margins at current gold prices. As the company’s earnings trend shows below, this is expected to have a dramatic positive effect on Fortuna’s bottom line.

(Source: YCharts.com, Author’s Chart)

While Fortuna has had an uninspiring earnings trend the past several years, FY2020 is expected to mark the end of declining annual EPS, with FY2021 estimates continuing to climb. Currently, FY2021 estimates are sitting at $0.98, and this would translate to 475% earnings growth next year assuming FSM earns $0.19 this year. This is incredible growth that is the 2nd highest in the sector currently, and this recent pullback has left FSM sitting at just 7.5x FY2021 annual EPS estimates.

It’s important to note that this discount to peers is justified as FSM has a lower mine life at its Mexican silver mine, but the discount is beginning to get a little overdone here. If we were to see the stock trade down below $6.50, I believe this would be an area to begin to nibble on the stock for investors comfy with smaller-cap names. Ultimately, Lindero has the potential to transform FSM into a higher-margin producer than most of its peers, and the market doesn’t seem to be recognizing this yet.

While the Silver Miners Index is one to play higher silver prices, I believe the best way to play the sector is by owning small positions in the miners with the highest earnings growth. PAAS, FSM, and HL are three names with exponential earnings growth and a strong probability of dividend growth in the next 15 months, and I expect all three to make exceptional investments as long as silver stays above $21.50/oz.

Given PAAS’ high margins and costs below $10.00/oz, the company is the lowest risk among the group as it’s insulated against a sharp drop in silver. For investors looking to add some silver exposure to their portfolio, the above three names are worth keeping at the top of one’s shopping list.

Disclosure: I am long GLD, PAAS

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Want More Great Investing Ideas?

Top 11 Picks for Today’s Market

Dangerous Outlook for Stocks Into Election

5 WINNING Stocks Chart Patterns

PAAS shares were trading at $33.54 per share on Thursday afternoon, down $0.62 (-1.81%). Year-to-date, PAAS has gained 42.41%, versus a 8.51% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Silver Miners With EXPLOSIVE Growth Potential appeared first on StockNews.com