Since September 2025, Wells Fargo has been in a holding pattern, posting a small return of 4.1% while floating around $82.37.

Is there a buying opportunity in Wells Fargo, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Wells Fargo Not Exciting?

We're cautious about Wells Fargo. Here are three reasons why WFC doesn't excite us and a stock we'd rather own.

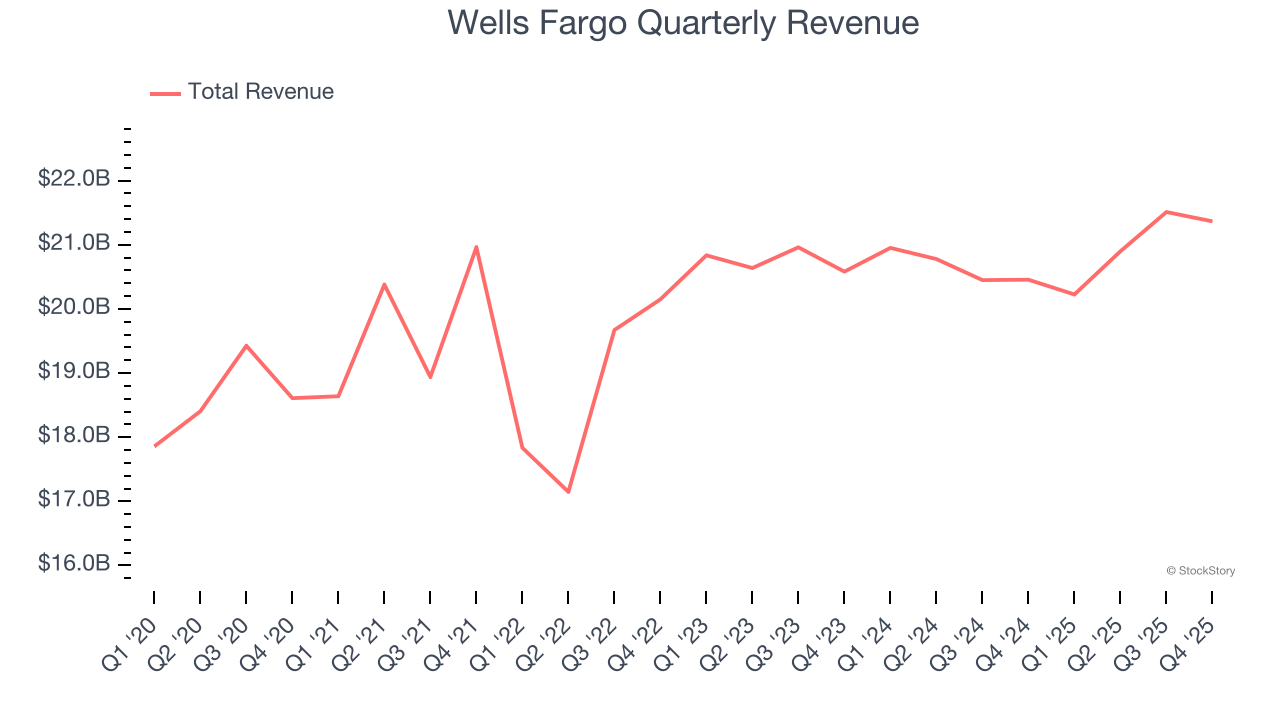

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Regrettably, Wells Fargo’s revenue grew at a sluggish 2.5% compounded annual growth rate over the last five years. This fell short of our benchmarks.

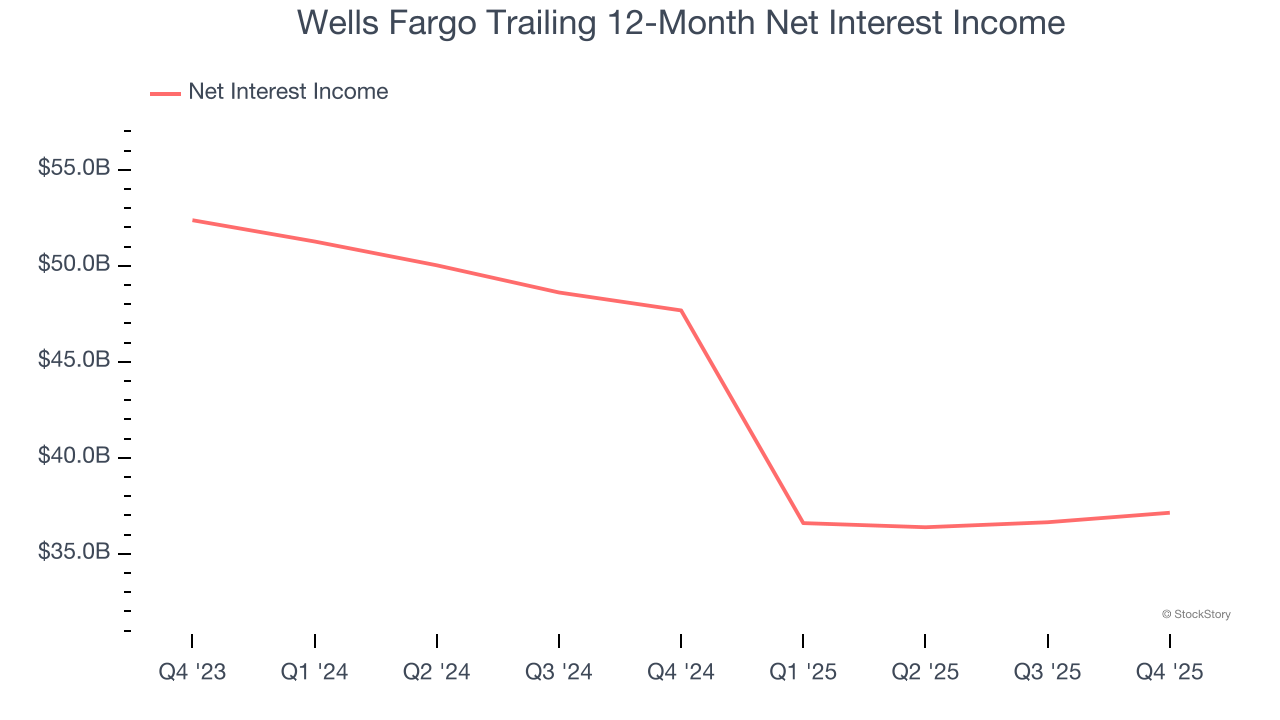

2. Declining Net Interest Income Reflects Weakness

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Wells Fargo’s net interest income has declined by 1.5% annually over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

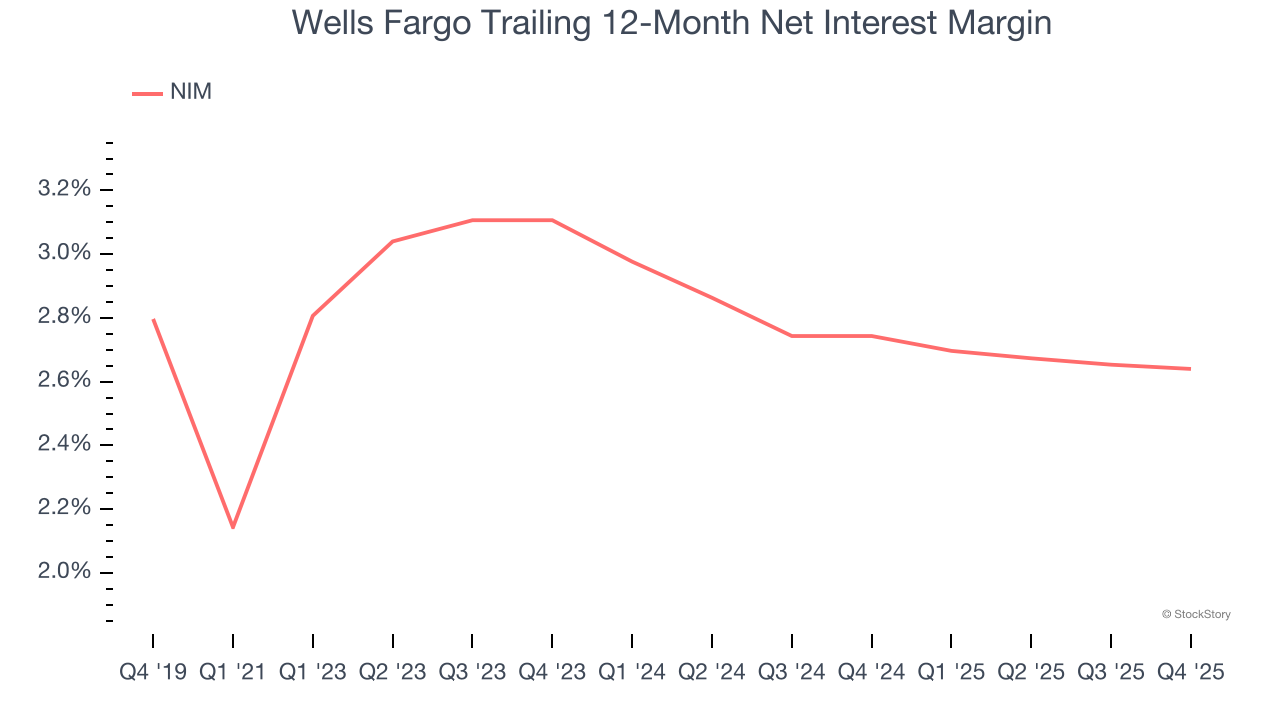

3. Net Interest Margin Dropping

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Wells Fargo’s net interest margin averaged 2.7%. Its margin also contracted by 46.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean that Wells Fargo either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

Final Judgment

Wells Fargo isn’t a terrible business, but it isn’t one of our picks. That said, the stock currently trades at 1.5× forward P/B (or $82.37 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than Wells Fargo

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.