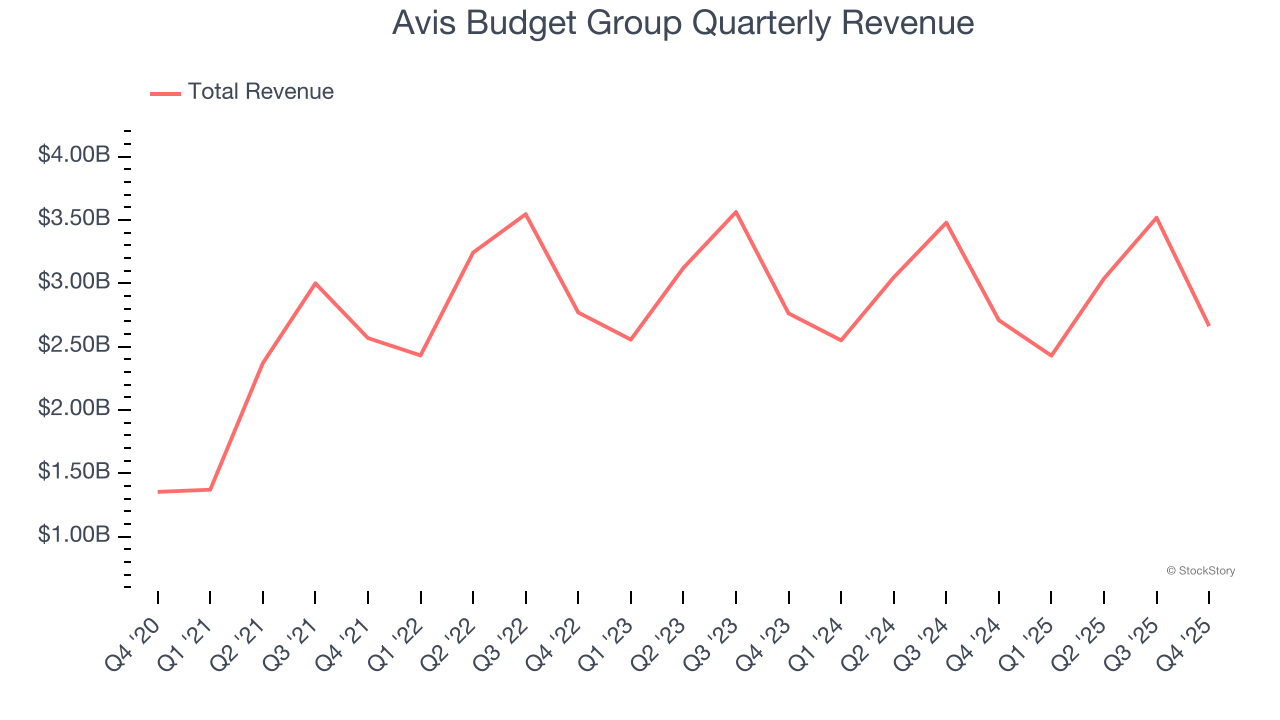

Car rental services provider Avis (NASDAQ: CAR) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 1.7% year on year to $2.66 billion. Its GAAP loss of $21.25 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Avis Budget Group? Find out by accessing our full research report, it’s free.

Avis Budget Group (CAR) Q4 CY2025 Highlights:

- Revenue: $2.66 billion vs analyst estimates of $2.74 billion (1.7% year-on-year decline, 2.9% miss)

- EPS (GAAP): -$21.25 vs analyst estimates of -$0.19 (significant miss)

- Adjusted EBITDA: $5 million vs analyst estimates of $145.8 million (0.2% margin, 96.6% miss)

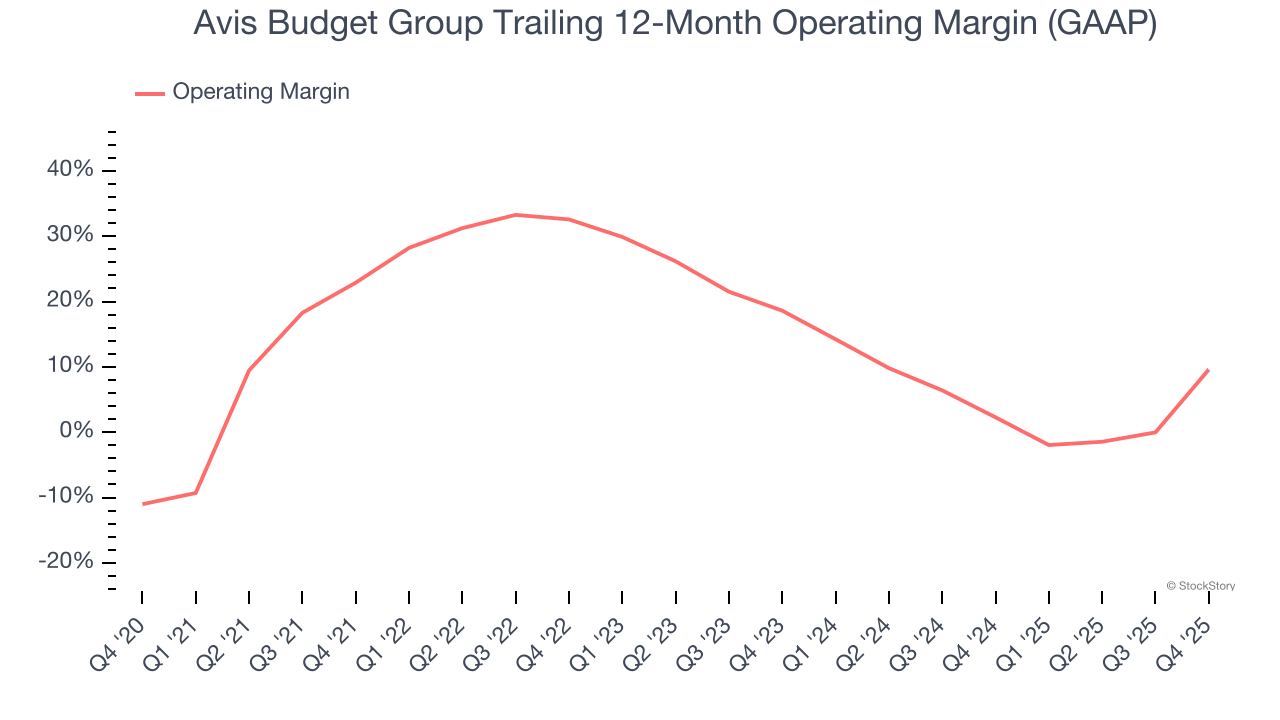

- Operating Margin: 33%, up from -9% in the same quarter last year

- Free Cash Flow was -$181 million compared to -$579.3 million in the same quarter last year

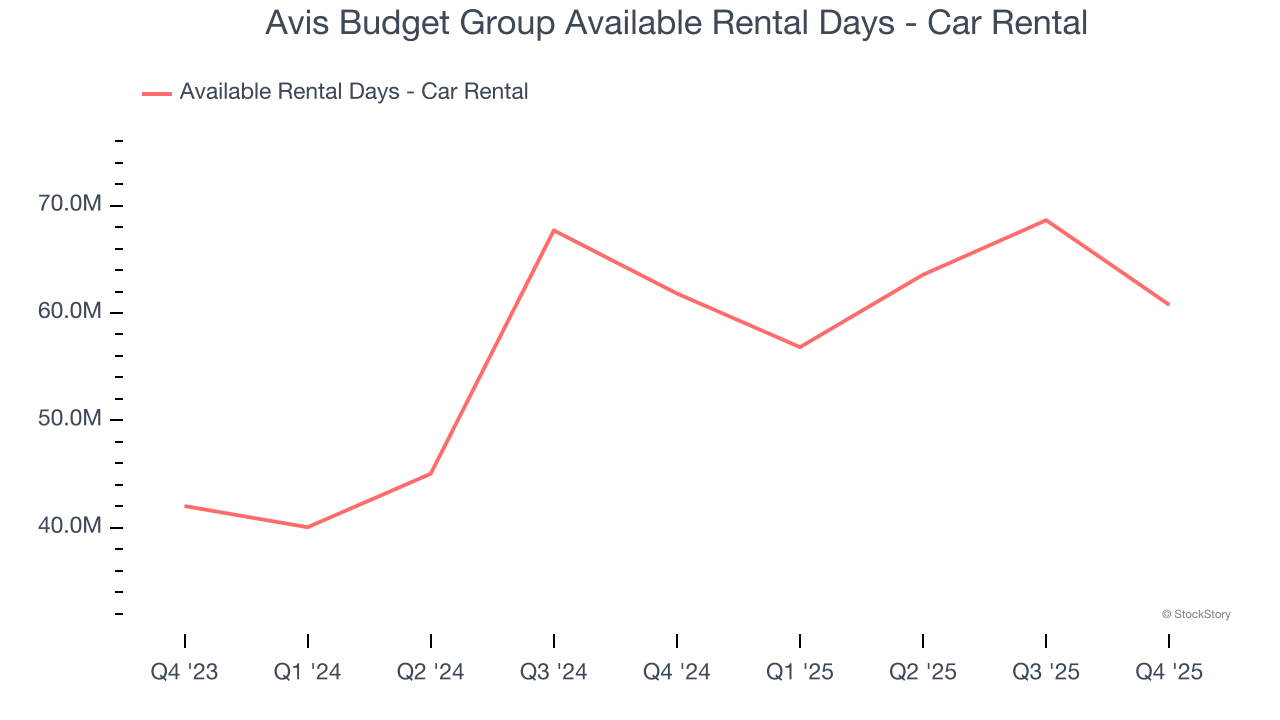

- Available rental days - Car rental: 60.76 million, down 1.06 million year on year

- Market Capitalization: $4.30 billion

“As we enter 2026, we’ve repositioned the business and turned a challenging fourth quarter into a catalyst for meaningful change,” said Brian Choi, Avis Budget Group CEO.

Company Overview

The parent company of brands such as Zipcar and Budget Truck Rental, Avis (NASDAQ: CAR) is a provider of car rental and mobility solutions.

Revenue Growth

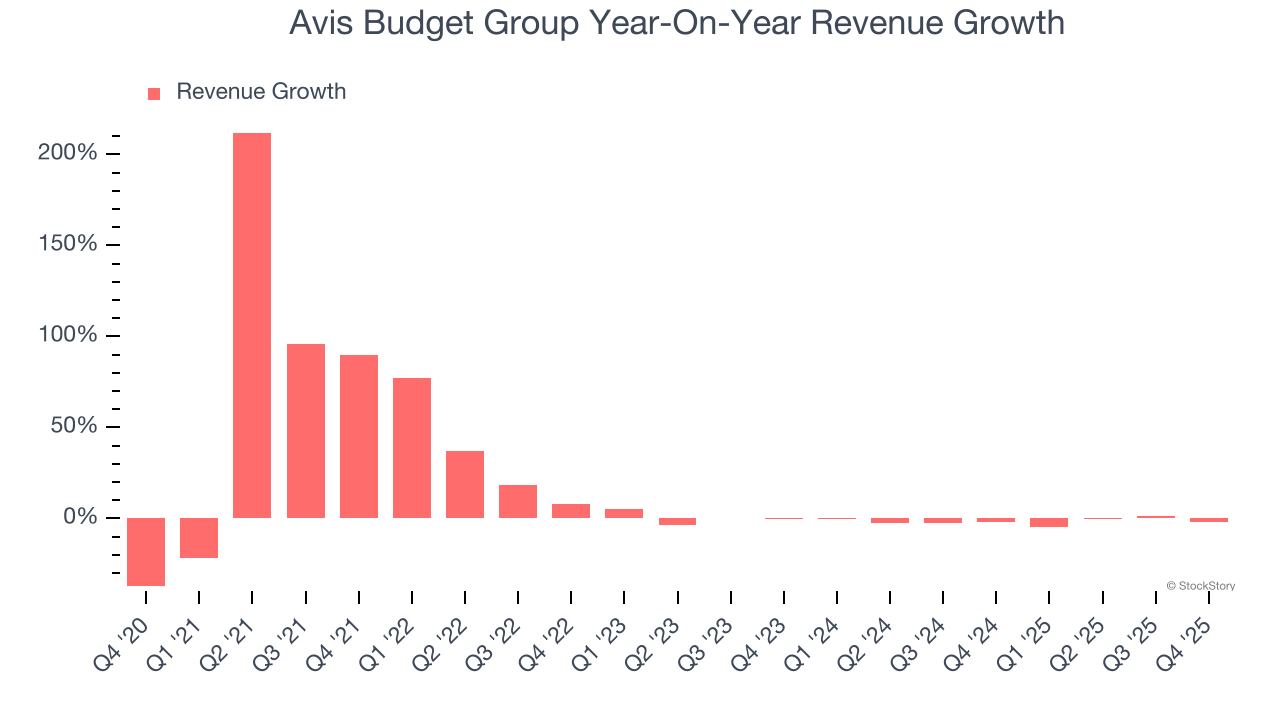

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Avis Budget Group grew its sales at an incredible 16.6% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Avis Budget Group’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.5% over the last two years.

We can dig further into the company’s revenue dynamics by analyzing its number of available rental days - car rental, which reached 60.76 million in the latest quarter. Over the last two years, Avis Budget Group’s available rental days - car rental averaged 26% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Avis Budget Group missed Wall Street’s estimates and reported a rather uninspiring 1.7% year-on-year revenue decline, generating $2.66 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Avis Budget Group has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Avis Budget Group’s operating margin decreased by 13.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Avis Budget Group generated an operating margin profit margin of 33%, up 41.9 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

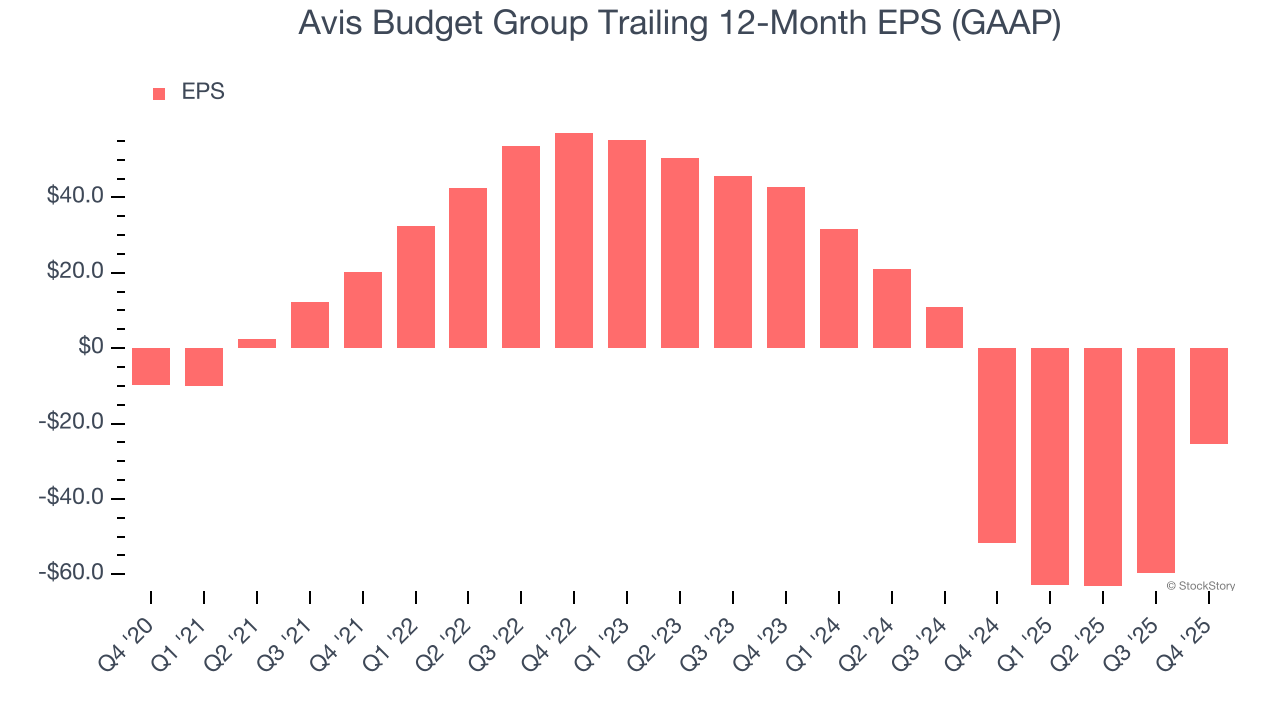

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Avis Budget Group’s earnings losses deepened over the last five years as its EPS dropped 21.2% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Avis Budget Group’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Avis Budget Group, its EPS declined by more than its revenue over the last two years, dropping 61.1%. This tells us the company struggled to adjust to shrinking demand.

In Q4, Avis Budget Group reported EPS of negative $21.25, up from negative $55.63 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Avis Budget Group’s full-year EPS of negative $25.37 will flip to positive $8.80.

Key Takeaways from Avis Budget Group’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.1% to $110.70 immediately following the results.

Avis Budget Group underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).