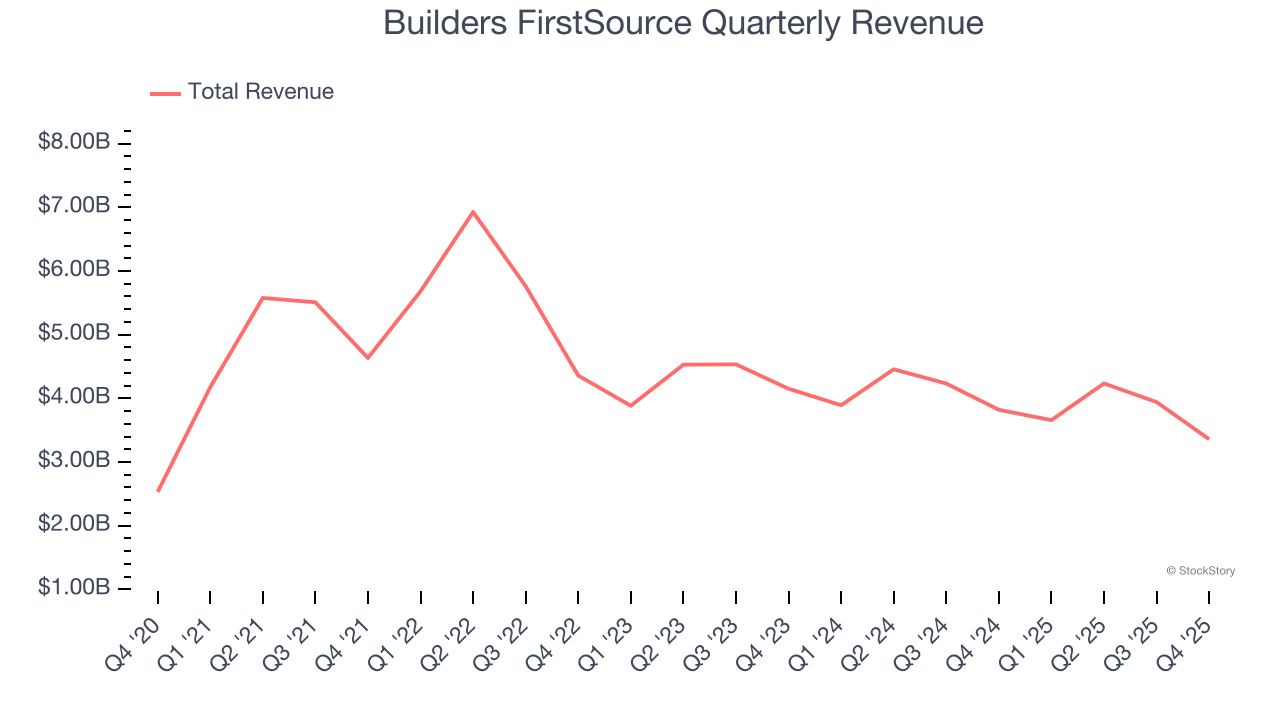

Building materials company Builders FirstSource (NYSE: BLDR) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 12.1% year on year to $3.36 billion. On the other hand, the company’s full-year revenue guidance of $15.3 billion at the midpoint came in 1.1% above analysts’ estimates. Its non-GAAP profit of $1.12 per share was 12.3% below analysts’ consensus estimates.

Is now the time to buy Builders FirstSource? Find out by accessing our full research report, it’s free.

Builders FirstSource (BLDR) Q4 CY2025 Highlights:

- Revenue: $3.36 billion vs analyst estimates of $3.45 billion (12.1% year-on-year decline, 2.8% miss)

- Adjusted EPS: $1.12 vs analyst expectations of $1.28 (12.3% miss)

- Adjusted EBITDA: $274.9 million vs analyst estimates of $336.4 million (8.2% margin, 18.3% miss)

- EBITDA guidance for the upcoming financial year 2026 is $1.5 billion at the midpoint, in line with analyst expectations

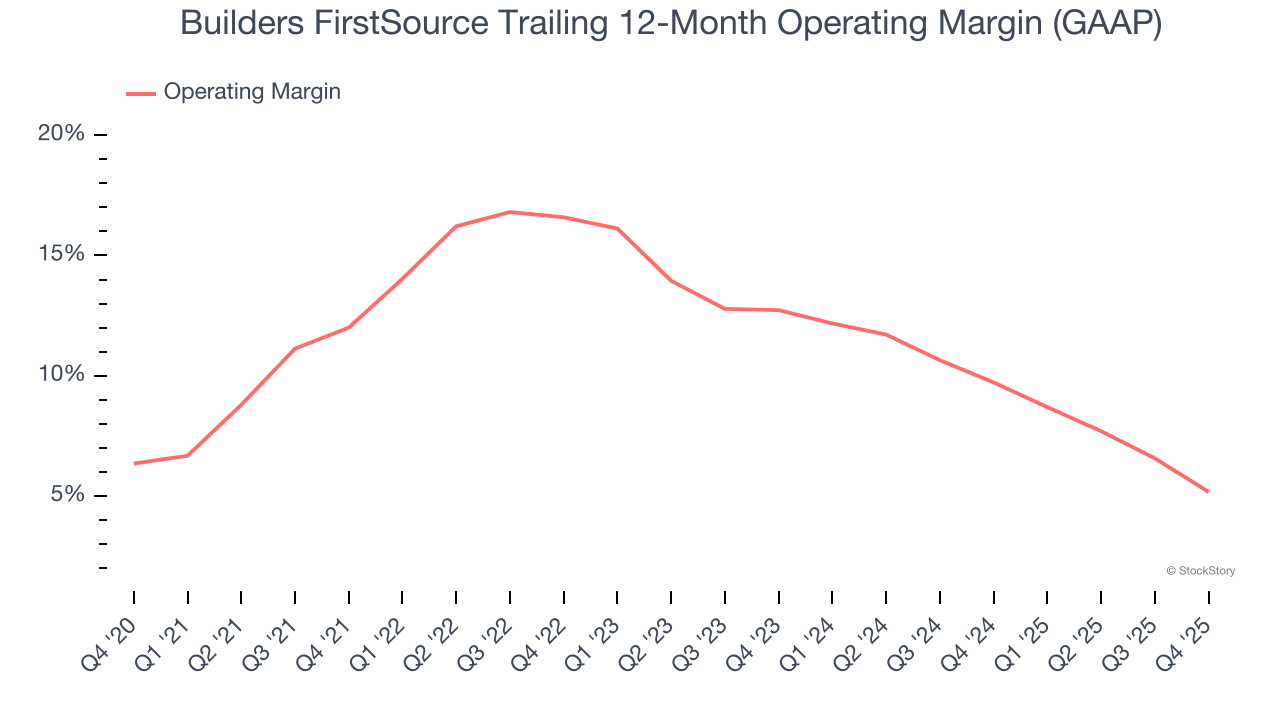

- Operating Margin: 1.8%, down from 8% in the same quarter last year

- Free Cash Flow Margin: 3.2%, down from 7.2% in the same quarter last year

- Market Capitalization: $12.69 billion

“Driven by focused execution and close customer partnerships, we successfully navigated 2025 despite ongoing housing affordability challenges, weak consumer confidence, and depressed commodity prices. We remain committed to reducing barriers to affordable housing and driving a more efficient, integrated supply chain. Our ability to perform effectively through each phase of the business cycle reflects the strength of our differentiated value-added solutions, industry-leading technology, and unique operating model,” commented Peter Jackson, CEO of Builders FirstSource.

Company Overview

Headquartered in Irving, TX, Builders FirstSource (NYSE: BLDR) is a construction materials manufacturer that offers a variety of lumber and lumber-related building products.

Revenue Growth

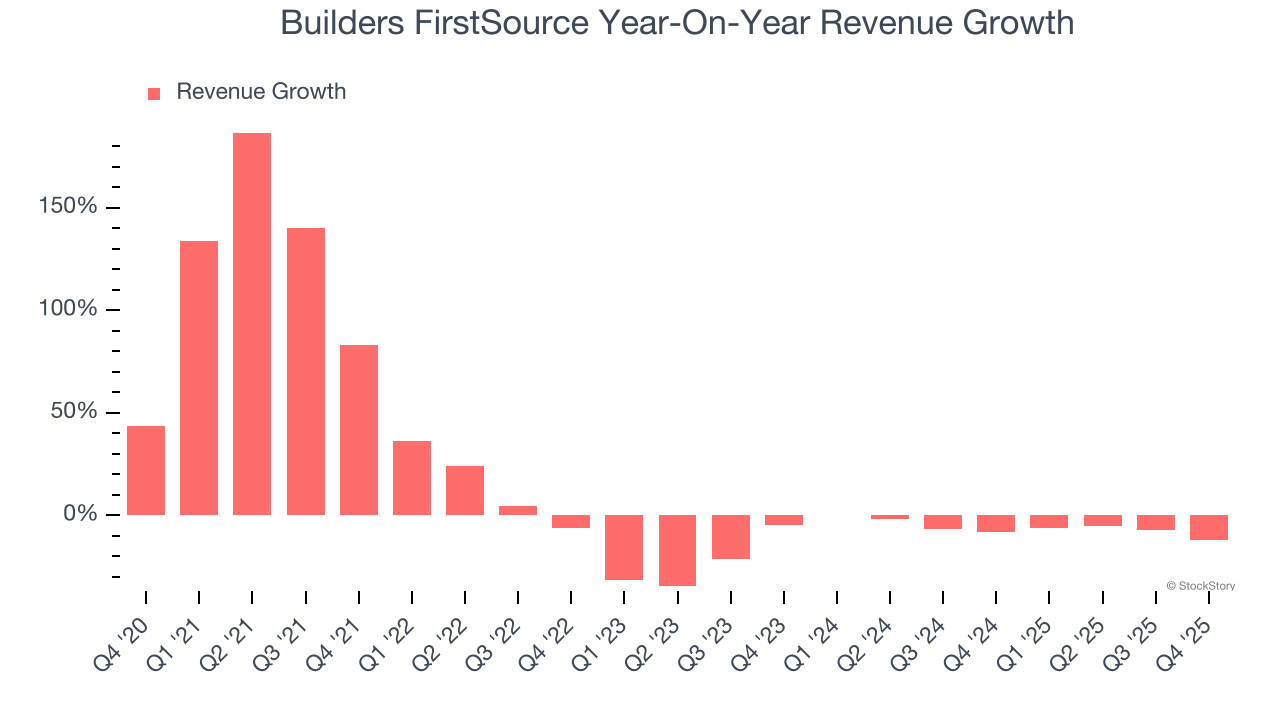

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Builders FirstSource’s 12.2% annualized revenue growth over the last five years was excellent. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Builders FirstSource’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 5.7% over the last two years.

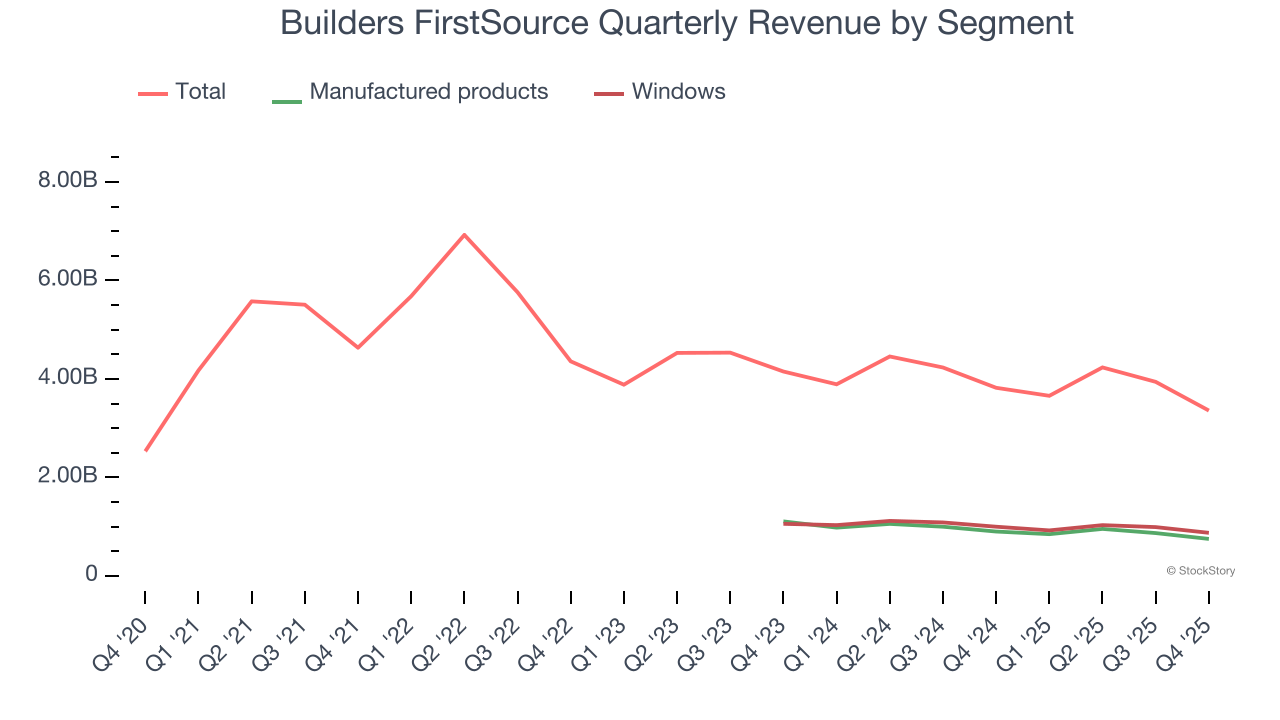

We can better understand the company’s revenue dynamics by analyzing its most important segments, Manufactured products

and Windows, doors & millwork

, which are 22.3% and 26% of revenue. Over the last two years, Builders FirstSource’s Manufactured products

revenue (floors, wall panels, and engineered wood) averaged 14.3% year-on-year declines while its Windows, doors & millwork

revenue (self explanatory) averaged 9% declines.

This quarter, Builders FirstSource missed Wall Street’s estimates and reported a rather uninspiring 12.1% year-on-year revenue decline, generating $3.36 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Builders FirstSource has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.7%.

Looking at the trend in its profitability, Builders FirstSource’s operating margin decreased by 6.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Builders FirstSource generated an operating margin profit margin of 1.8%, down 6.1 percentage points year on year. Since Builders FirstSource’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

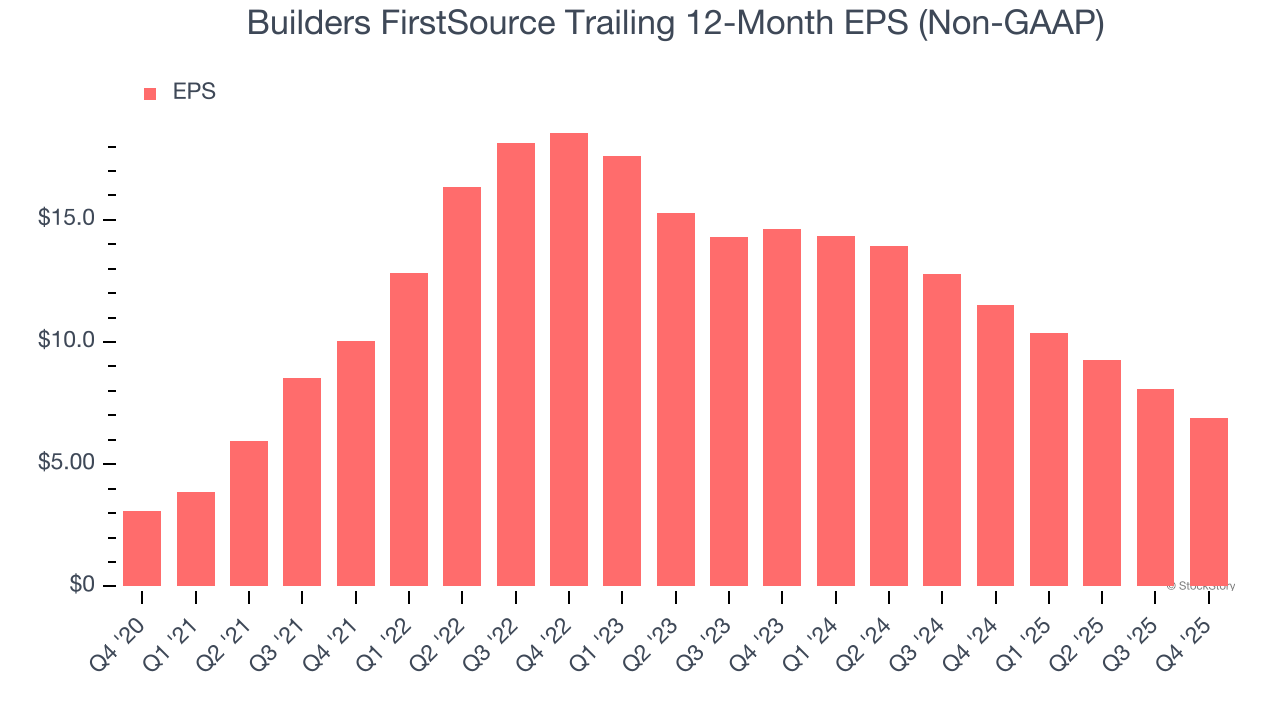

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Builders FirstSource’s EPS grew at a spectacular 17.4% compounded annual growth rate over the last five years, higher than its 12.2% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

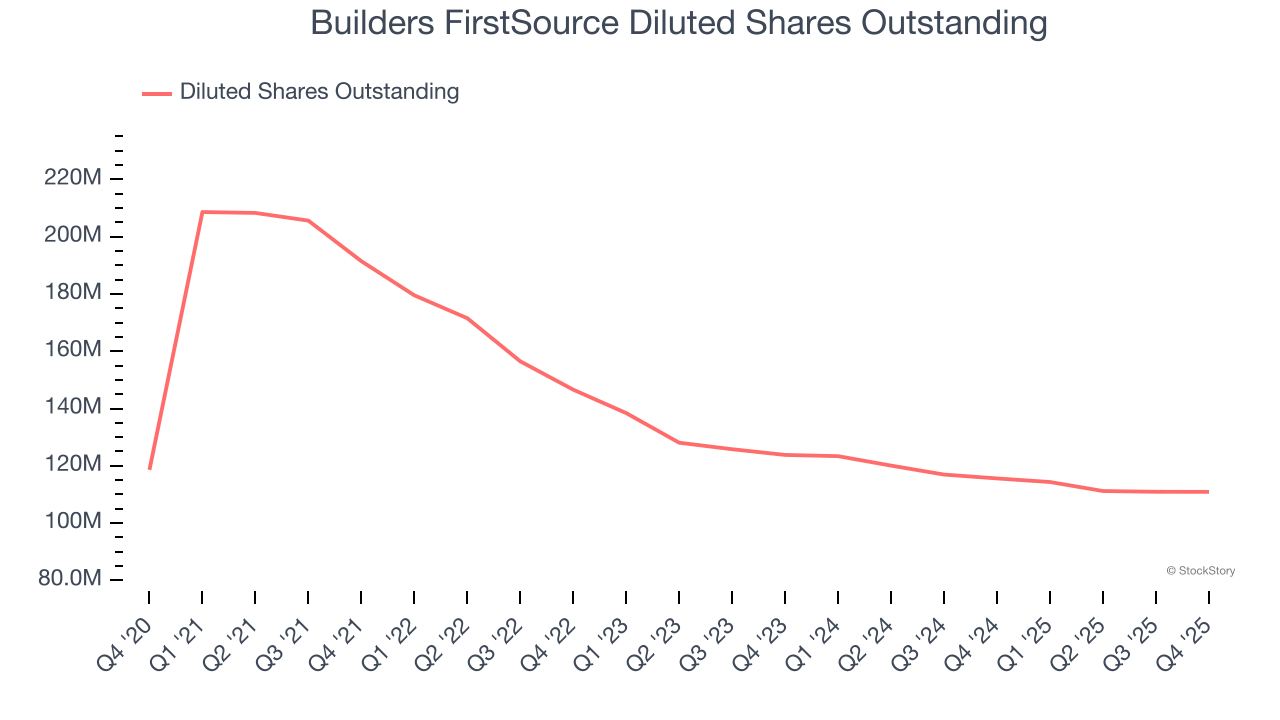

Diving into the nuances of Builders FirstSource’s earnings can give us a better understanding of its performance. A five-year view shows that Builders FirstSource has repurchased its stock, shrinking its share count by 6.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Builders FirstSource, its two-year annual EPS declines of 31.4% mark a reversal from its (seemingly) healthy five-year trend. We hope Builders FirstSource can return to earnings growth in the future.

In Q4, Builders FirstSource reported adjusted EPS of $1.12, down from $2.31 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Builders FirstSource’s full-year EPS of $6.89 to shrink by 9.9%.

Key Takeaways from Builders FirstSource’s Q4 Results

It was good to see Builders FirstSource provide full-year revenue guidance that slightly beat analysts’ expectations. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $115.71 immediately after reporting.

So do we think Builders FirstSource is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).