Since August 2020, the S&P 500 has delivered a total return of 90.8%. But one standout stock has more than doubled the market - over the past five years, Crane has surged 223% to $197.31 per share. Its momentum hasn’t stopped as it’s also gained 17% in the last six months thanks to its solid quarterly results, beating the S&P by 11.6%.

Is now the time to buy Crane, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Crane Will Underperform?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why there are better opportunities than CR and a stock we'd rather own.

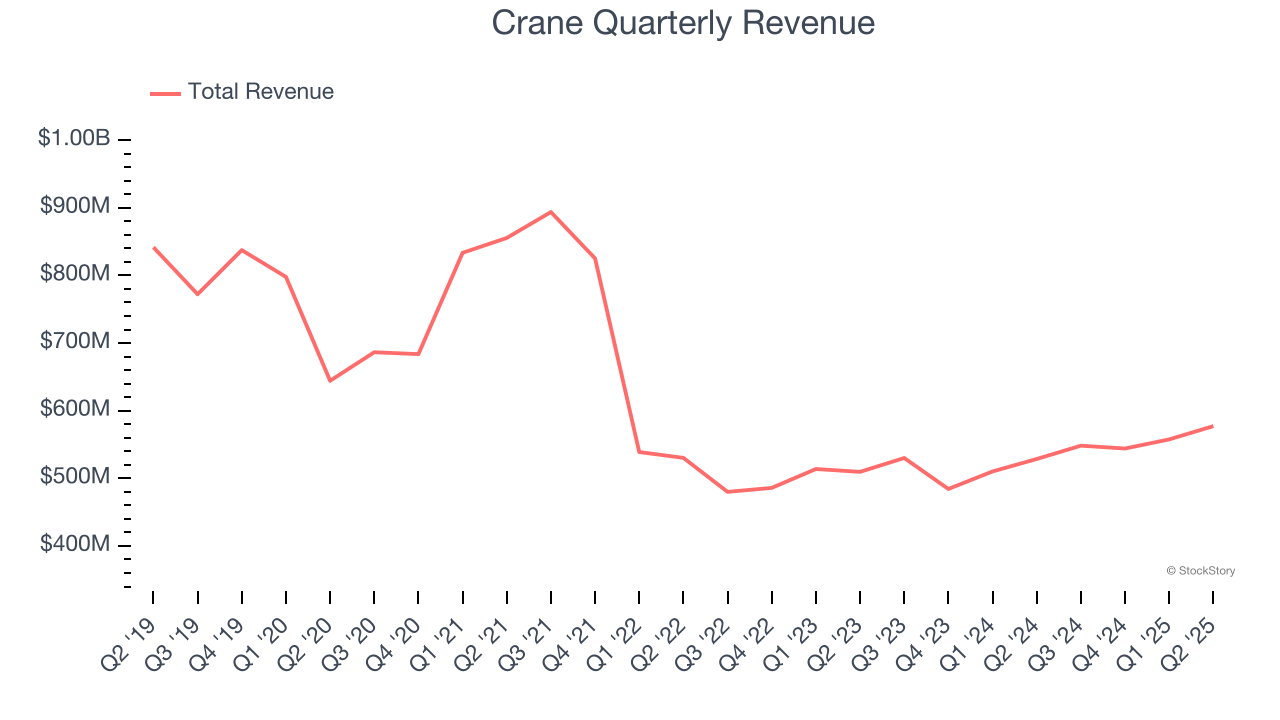

1. Revenue Spiraling Downwards

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Crane’s demand was weak and its revenue declined by 6.1% per year. This wasn’t a great result and is a sign of poor business quality.

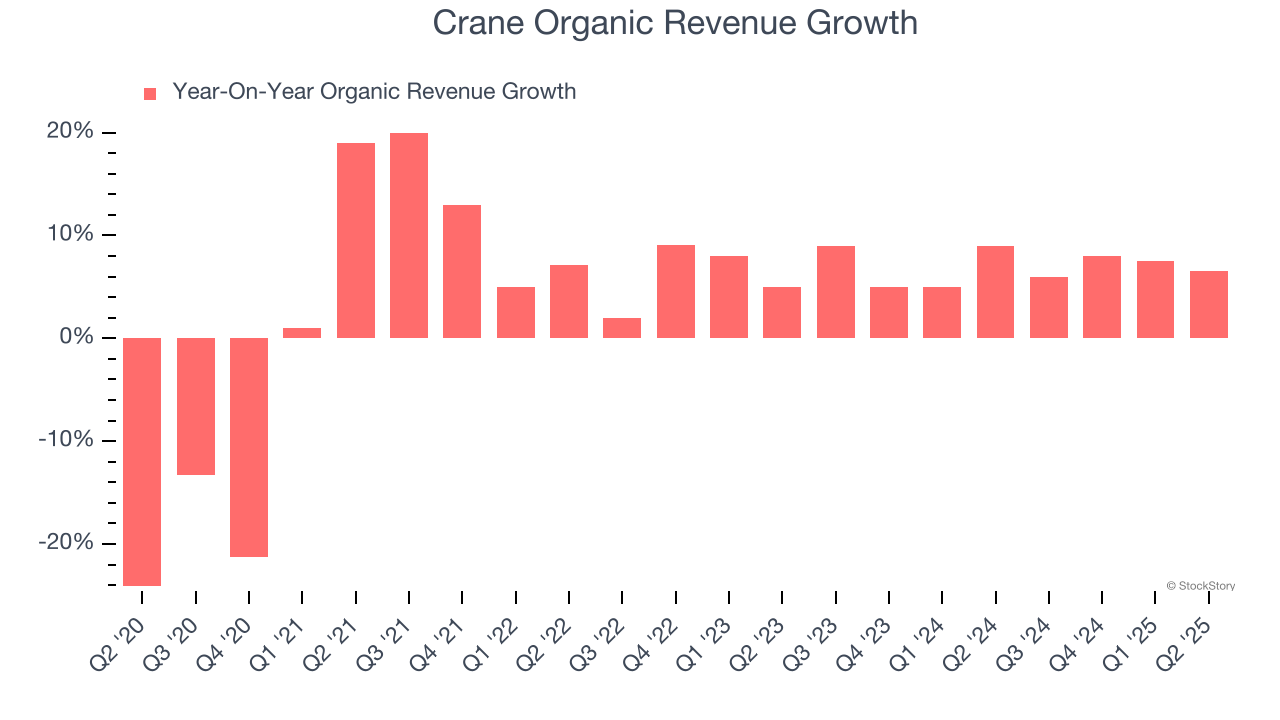

2. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand General Industrial Machinery companies by analyzing their organic revenue. This metric gives visibility into Crane’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Crane’s organic revenue averaged 7% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

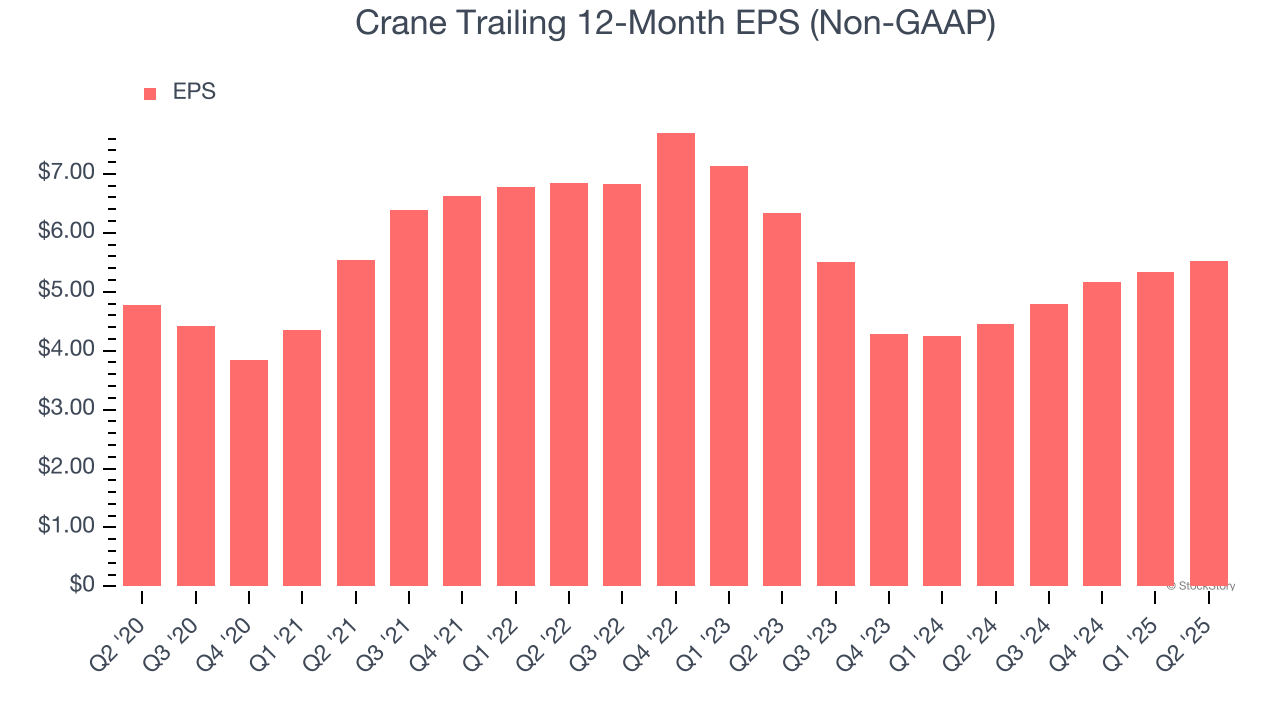

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Crane’s EPS grew at a weak 3% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 6.1% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

We see the value of companies helping their customers, but in the case of Crane, we’re out. With its shares beating the market recently, the stock trades at 33.6× forward P/E (or $197.31 per share). At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Crane

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.