The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Mueller Water Products (NYSE: MWA) and the rest of the water infrastructure stocks fared in Q1.

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 5 water infrastructure stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 11.8%.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

Mueller Water Products (NYSE: MWA)

As one of the oldest companies in the water infrastructure industry, Mueller (NYSE: MWA) is a provider of water infrastructure products and flow control systems for various sectors.

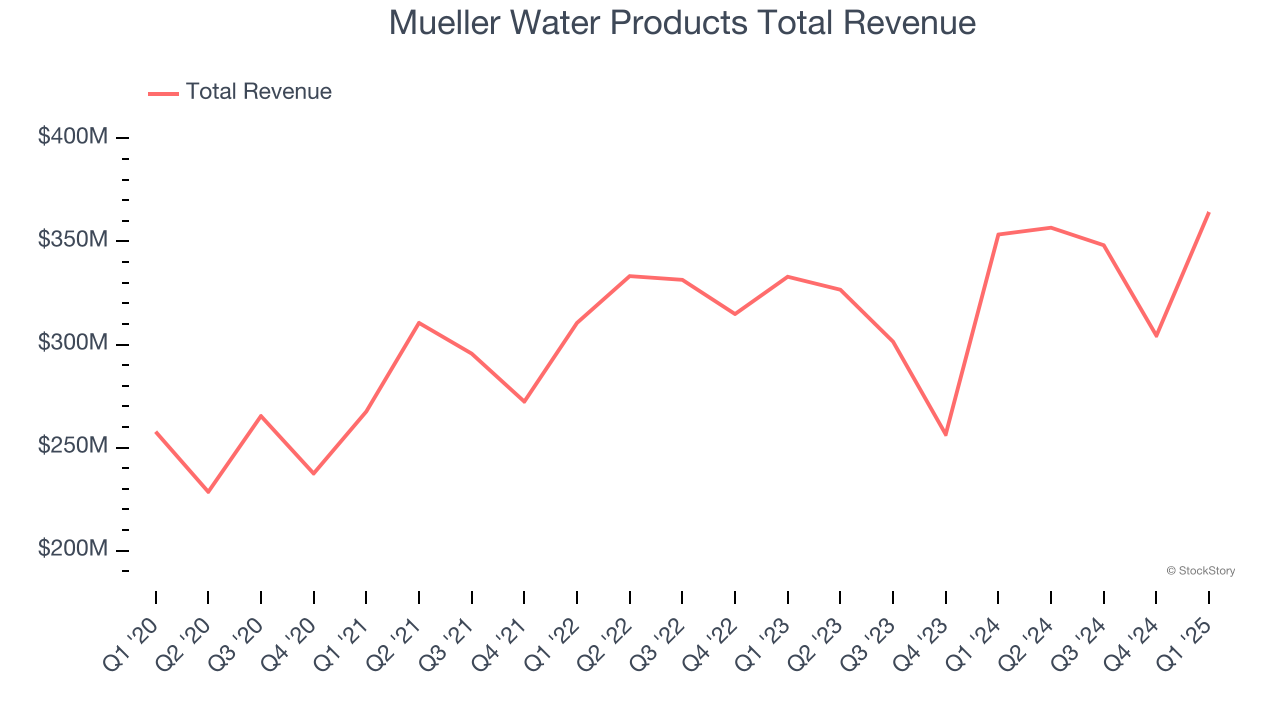

Mueller Water Products reported revenues of $364.3 million, up 3.1% year on year. This print exceeded analysts’ expectations by 2.9%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EBITDA estimates.

“We delivered a solid performance in our second quarter. Our focused execution enabled us to benefit from healthy order levels during the quarter supported by continued resilient end-market demand. As a result, we achieved quarterly records for our consolidated net sales, adjusted EBITDA and adjusted net income per share. I am grateful for our teams’ dedication to delivering exceptional customer service, improving operational excellence and maintaining cost discipline which contributed to these results,” said Martie Edmunds Zakas, Chief Executive Officer of Mueller Water Products.

Mueller Water Products achieved the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 9.9% since reporting and currently trades at $24.37.

Is now the time to buy Mueller Water Products? Access our full analysis of the earnings results here, it’s free.

Best Q1: Watts Water Technologies (NYSE: WTS)

Founded in 1874, Watts Water (NYSE: WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

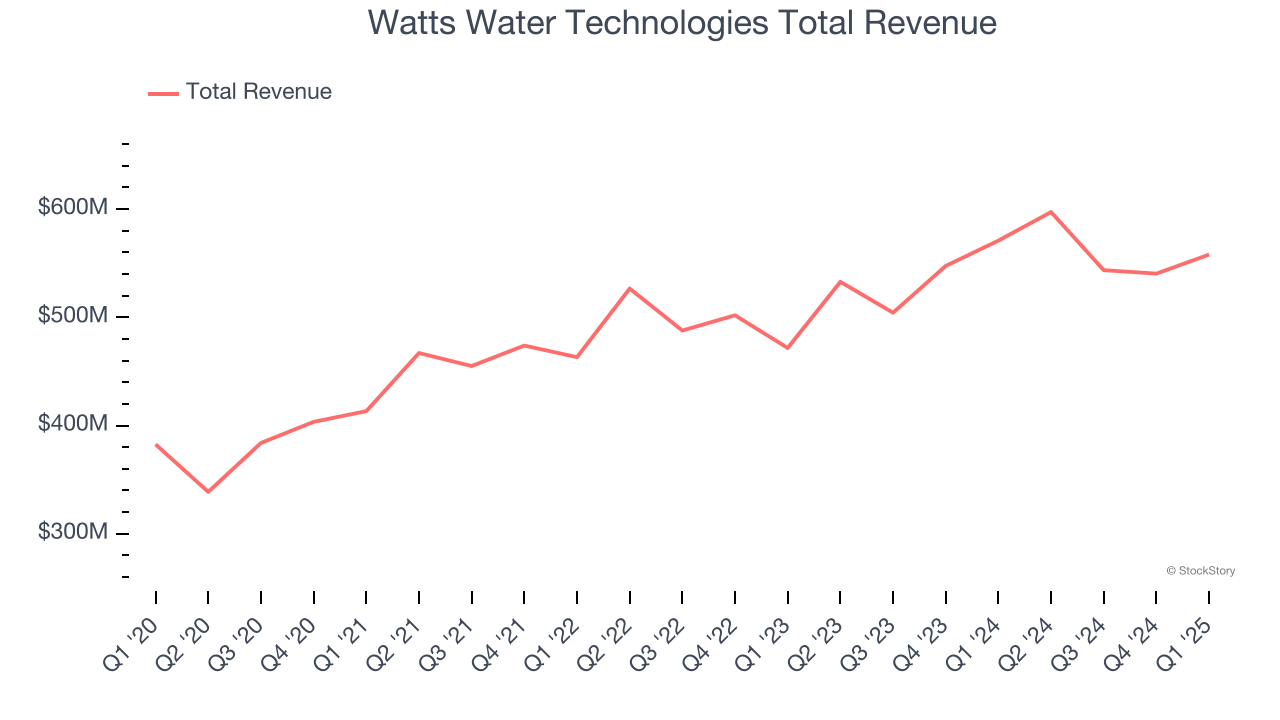

Watts Water Technologies reported revenues of $558 million, down 2.3% year on year, outperforming analysts’ expectations by 1.9%. The business had an exceptional quarter with a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 13.8% since reporting. It currently trades at $240.79.

Is now the time to buy Watts Water Technologies? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Energy Recovery (NASDAQ: ERII)

Having saved far more than a trillion gallons of water, Energy Recovery (NASDAQ: ERII) provides energy recovery devices to the water treatment, oil and gas, and chemical processing sectors.

Energy Recovery reported revenues of $8.07 million, down 33.3% year on year, falling short of analysts’ expectations by 63.3%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Energy Recovery delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 16.8% since the results and currently trades at $12.51.

Read our full analysis of Energy Recovery’s results here.

Xylem (NYSE: XYL)

Formed through a spinoff, Xylem (NYSE: XYL) manufactures and services engineered products across a wide variety of applications primarily in the water sector.

Xylem reported revenues of $2.07 billion, up 1.8% year on year. This result beat analysts’ expectations by 1.5%. Overall, it was a very strong quarter as it also logged an impressive beat of analysts’ EBITDA estimates.

The stock is up 9.4% since reporting and currently trades at $126.66.

Read our full, actionable report on Xylem here, it’s free.

Tennant (NYSE: TNC)

As the world’s largest manufacturer of autonomous mobile robots, Tennant (NYSE: TNC) designs, manufactures, and sells cleaning products to various sectors.

Tennant reported revenues of $290 million, down 6.8% year on year. This number missed analysts’ expectations by 2.2%. It was a softer quarter as it also recorded a significant miss of analysts’ EBITDA and EPS estimates.

Tennant had the weakest full-year guidance update among its peers. The stock is up 1.8% since reporting and currently trades at $73.37.

Read our full, actionable report on Tennant here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.