As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the regional banks industry, including First BanCorp (NYSE: FBP) and its peers.

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

The 105 regional banks stocks we track reported a mixed Q1. As a group, revenues missed analysts’ consensus estimates by 1.6%.

Thankfully, share prices of the companies have been resilient as they are up 7.3% on average since the latest earnings results.

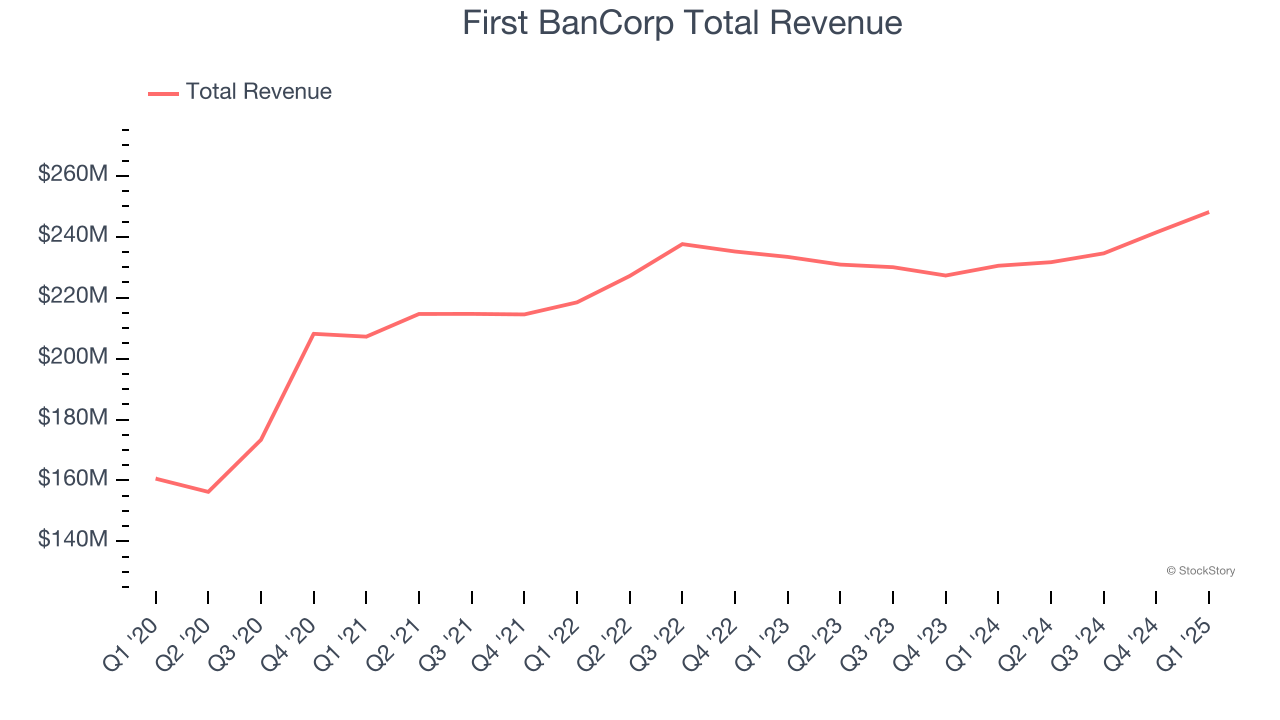

First BanCorp (NYSE: FBP)

Tracing its roots back to 1948 in San Juan, First BanCorp (NYSE: FBP) is a bank holding company that provides commercial banking, consumer financing, mortgage services, and insurance products across Puerto Rico, the U.S. mainland, and the Caribbean.

First BanCorp reported revenues of $248.1 million, up 7.6% year on year. This print exceeded analysts’ expectations by 2.8%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ tangible book value per share estimates and a decent beat of analysts’ EPS estimates.

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $21.06.

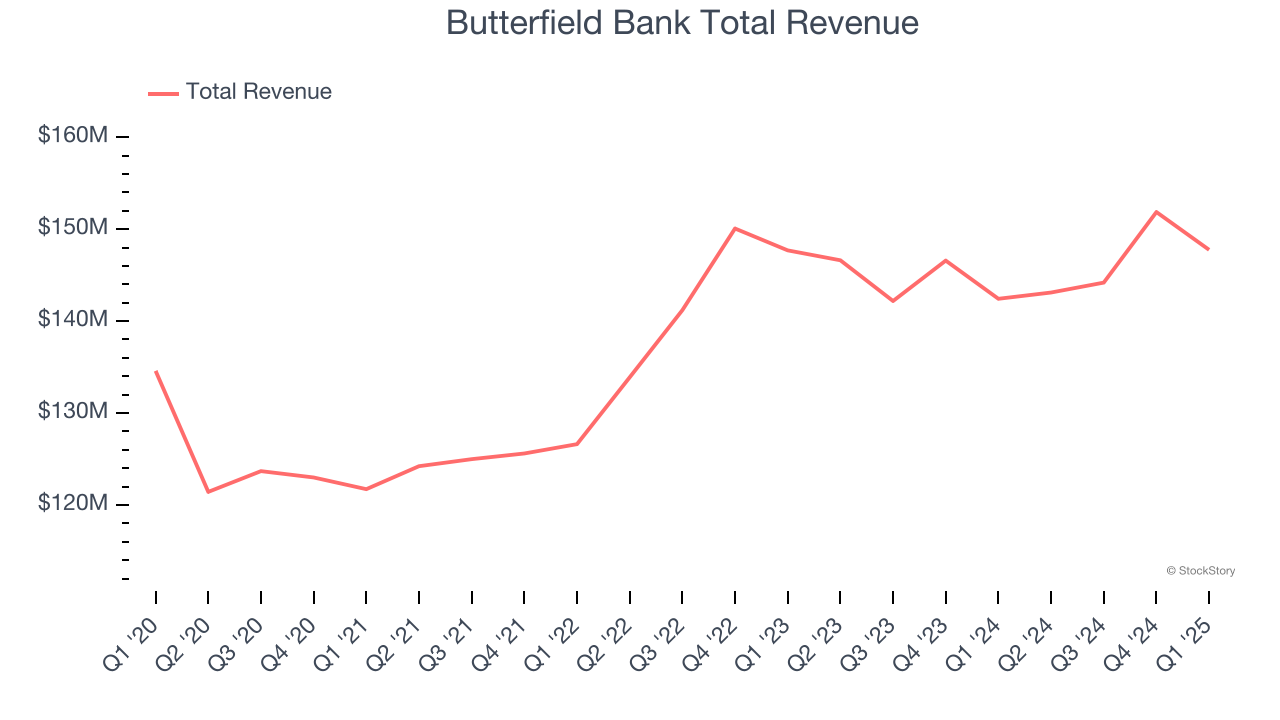

Best Q1: Butterfield Bank (NYSE: NTB)

Founded in 1784 as one of the oldest banks in the Western Hemisphere, Butterfield Bank (NYSE: NTB) provides banking, wealth management, and trust services to individuals and businesses in select offshore financial centers including Bermuda, Cayman Islands, and the Channel Islands.

Butterfield Bank reported revenues of $147.8 million, up 3.7% year on year, outperforming analysts’ expectations by 4.4%. The business had a stunning quarter with an impressive beat of analysts’ net interest income estimates and a solid beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 5.9% since reporting. It currently trades at $44.91.

Is now the time to buy Butterfield Bank? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Triumph Financial (NASDAQ: TFIN)

Originally focused on traditional banking before pivoting to serve the transportation sector, Triumph Financial (NASDAQ: TFIN) provides specialized financial services to the trucking industry, including payments processing, factoring, banking, and data intelligence solutions.

Triumph Financial reported revenues of $100.8 million, flat year on year, falling short of analysts’ expectations by 3.8%. It was a disappointing quarter as it posted a significant miss of analysts’ tangible book value per share and net interest income estimates.

Interestingly, the stock is up 14.3% since the results and currently trades at $56.95.

Read our full analysis of Triumph Financial’s results here.

United Bankshares (NASDAQ: UBSI)

With roots dating back to 1982 and a strong presence in the Mid-Atlantic region, United Bankshares (NASDAQ: UBSI) is a bank holding company that provides commercial and retail banking services through its United Bank subsidiary across multiple states.

United Bankshares reported revenues of $289.6 million, up 13.7% year on year. This result beat analysts’ expectations by 4.1%. It was a stunning quarter as it also produced a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ net interest income estimates.

The stock is flat since reporting and currently trades at $36.76.

Read our full, actionable report on United Bankshares here, it’s free.

Comerica (NYSE: CMA)

Founded in 1849 during the California Gold Rush era, Comerica (NYSE: CMA) is a financial services company that provides commercial banking, retail banking, and wealth management services to businesses and individuals.

Comerica reported revenues of $829 million, up 5.7% year on year. This print met analysts’ expectations. Overall, it was a strong quarter as it also recorded a solid beat of analysts’ tangible book value per share estimates and a decent beat of analysts’ EPS estimates.

The stock is up 11.6% since reporting and currently trades at $59.08.

Read our full, actionable report on Comerica here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.