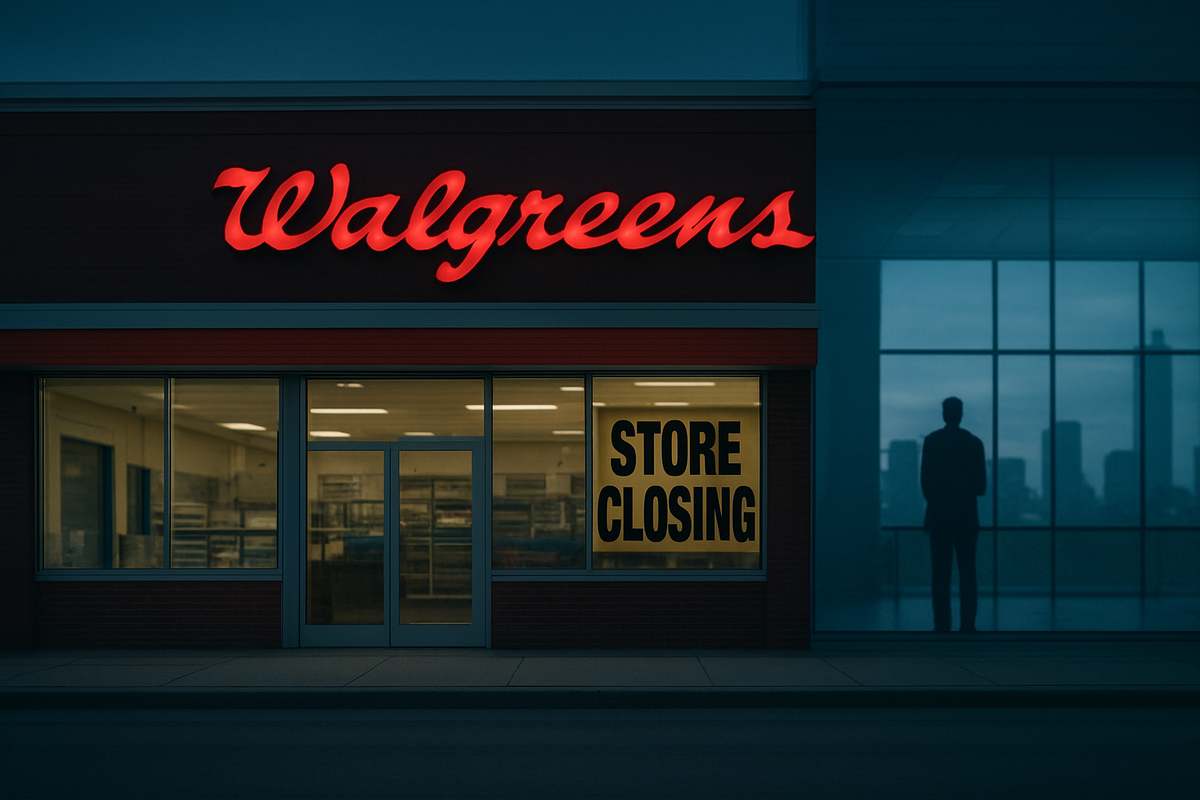

DEERFIELD, IL — February 23, 2026 — In a move that underscores the continued volatility of the American retail pharmacy landscape, the newly private Walgreens Boots Alliance has announced a significant expansion of its workforce reductions and a finalized timeline for its massive store closure initiative. Under the leadership of the private equity firm Sycamore Partners, which completed a landmark $10 billion acquisition of the company in August 2025, Walgreens is slashing hundreds of additional corporate roles and shuttering a major distribution hub as it battles the systemic pressures that have already claimed several of its former peers.

The immediate fallout includes the elimination of 628 positions, primarily centered at the company’s historic Deerfield headquarters and a logistics center in Houston, Texas. This latest round of cuts serves as a stark reminder that the "Big Three" era of retail pharmacy is effectively over. With Rite Aid having finished its total liquidation in late 2025 and CVS Health (NYSE: CVS) aggressively pivoting toward insurance and primary care, the once-ubiquitous neighborhood drugstore is being redesigned into a leaner, digital-first entity that prioritizes margin over geographic footprint.

The Shrinking Footprint: A Timeline of Retraction

The current wave of restructuring traces back to October 2024, when Walgreens — then a publicly traded component of the Nasdaq (formerly WBA) — admitted its business model was "non-sustainable." At that time, former CEO Tim Wentworth announced a plan to shutter 1,200 underperforming locations over three years. However, following the Sycamore Partners buyout last summer, the strategy has shifted from a gradual "right-sizing" to an aggressive surgical removal of unprofitable assets.

The newest cuts announced this month hit the corporate heart of the company. In Illinois, 469 roles were eliminated in a move to flatten management layers and reduce overhead. Simultaneously, the company confirmed the closure of its Houston distribution center, effective June 1, 2026, resulting in 159 job losses. These moves follow a chaotic 18-month period that saw the company struggle with low reimbursement rates from Pharmacy Benefit Managers (PBMs), high levels of retail "shrink" or theft, and a decline in discretionary "front-of-store" spending by inflation-weary consumers.

Key stakeholders, including new CEO Mike Motz, have signaled that the company’s survival depends on breaking its reliance on the traditional retail-plus-pharmacy format. By early 2026, Walgreens had already shuttered more than 500 of the 1,200 stores targeted in the 2024 plan. The focus has now turned to dividing the massive conglomerate into five standalone entities — including separate businesses for its U.K.-based Boots chain and its VillageMD clinical wing — to better manage the varying financial profiles of its assets.

The Winners and Losers of a Shifting Landscape

In the wake of Walgreens’ contraction, the primary "winner" appears to be Amazon (NASDAQ: AMZN). As physical stores vanish, Amazon Pharmacy has capitalized on the growing "pharmacy deserts" created by Walgreens' and CVS’s retreats. With its PillPack integration and aggressive Prime-member discounting, Amazon is capturing the high-margin, chronic-medication market that once formed the bedrock of the neighborhood drugstore.

CVS Health (NYSE: CVS) also stands to gain, though it faces its own restructuring hurdles. By leaning into its Aetna insurance vertical and HealthHUB clinics, CVS has insulated itself from the purely retail-driven volatility that nearly sank Walgreens. As Walgreens closes doors, CVS is often the last remaining national chain in many zip codes, giving it significant leverage in local markets even as it trims its own store count by hundreds of locations annually.

The clear "losers" in this event are the employees and the underserved communities. The loss of 628 specialized roles in Illinois and Texas marks a significant brain drain for the retail healthcare sector. More critically, the 1,200-store closure plan has disproportionately affected low-income urban and rural areas. For these populations, the loss of a Walgreens often means the loss of the only local provider for vaccinations, basic health screenings, and prescription medication, exacerbating the national "pharmacy desert" crisis.

Wider Significance: The Death of the Generalist Drugstore

Walgreens’ struggle is not an isolated corporate failure but a bellwether for the death of the generalist drugstore model. For decades, companies like Walgreens and the now-defunct Rite Aid relied on a high-volume, low-margin pharmacy counter to drive foot traffic for high-margin retail items like cosmetics and snacks. This "front-of-store" strategy has been decimated by the rise of e-commerce and discount retailers like Walmart (NYSE: WMT) and Target (NYSE: TGT).

The regulatory environment has also been a major catalyst. PBMs — the middlemen who negotiate drug prices — have consistently squeezed the margins that pharmacies receive for filling prescriptions. In some cases, pharmacies are reimbursed below their actual cost for life-saving medications. While Congress and the FTC have increased their scrutiny of PBM practices throughout 2025 and 2026, the policy shifts have come too late for Rite Aid and may be arriving too slowly to save the remaining brick-and-mortar retail pharmacy ecosystem in its current form.

What Comes Next: A Private Renaissance or a Slow Fade?

In the short term, Walgreens will continue its fragmentation. Under Sycamore Partners’ ownership, the market should expect the possible spin-off or sale of the Boots Group in the U.K. by the end of 2026. This would allow the U.S. operations to focus exclusively on a new "micro-fulfillment" model, where smaller, pharmacy-only kiosks replace the massive 15,000-square-foot stores that have become liabilities.

The long-term success of Walgreens depends on its ability to transition into a specialized healthcare services provider. By decoupling from its large retail footprints, the company hopes to lower its operational break-even point. However, the challenge will be competing with a resurgent independent pharmacy sector and tech-savvy disruptors like Mark Cuban’s Cost Plus Drug Company. If Walgreens cannot prove that its physical presence offers a clinical value that Amazon cannot replicate, further liquidations of its standalone businesses remain a distinct possibility.

Market Wrap-Up and Final Thoughts

The widening job cuts and store closures at Walgreens are the final chapters of a massive industry consolidation that began at the turn of the decade. The takeaway for the market is clear: the traditional "corner of happy and healthy" is no longer a viable real estate play in the age of digital healthcare and PBM-driven margin compression.

Moving forward, investors and analysts should watch for the performance of the remaining public players in the space. If Walgreens’ private equity-led pivot to smaller footprints and clinical services proves profitable, it may provide a roadmap for CVS Health’s own retail division. For the public, the era of the one-stop-shop drugstore is rapidly fading, replaced by a bifurcated system of mail-order convenience for some and increasing healthcare scarcity for others.

This content is intended for informational purposes only and is not financial advice.