Seattle-based Weyerhaeuser Company (WY) is one of the world's largest owners of timberlands. With a market cap of $16.6 billion, the company controls approximately 10.4 million acres of timberlands in the U.S. and manages additional timberlands under long-term licenses in Canada.

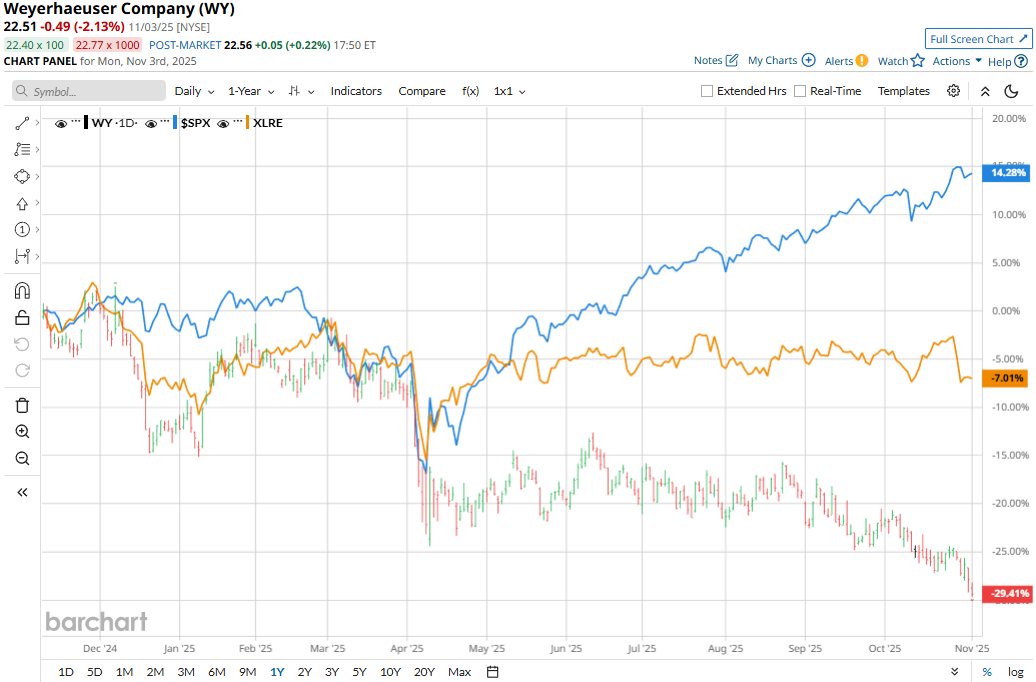

The real estate giant has significantly underperformed the broader market over the past year. WY stock prices have plummeted 20% in 2025 and 27.8% over the past 52 weeks, notably lagging behind the S&P 500 Index’s ($SPX) 16.5% gains in 2025 and 19.6% returns over the past year.

Narrowing the focus, Weyerhaeuser has also underperformed the sector-focused Real Estate Select Sector SPDR Fund’s (XLRE) marginal 39 bps uptick in 2025 and 4.5% decline over the past year.

Weyerhaeuser’s stock prices declined 2.2% in the trading session following the release of its mixed Q3 results on Oct. 30. The company’s net sales increased 2.1% year-over-year to $1.7 billion, beating the consensus estimates by 4.1%. Meanwhile, its EPS increased 20% year-over-year to $0.06, beating the consensus estimates of negative $0.07 by a huge margin.

However, the growth in EPS came from an extraordinary operating income; Weyerhaeuser’s actual profitability has gone for a toss. It's already a low gross margin, shrunk by almost 3% compared to the year-ago quarter to 11.9%, making investors jittery.

For the full fiscal 2025, ending in December, analysts expect WY to deliver an EPS of $0.08, down 84.9% year-over-year. On the positive note, the company has a robust earnings surprise history. It has met or surpassed the Street’s bottom-line estimates in each of the past four quarters.

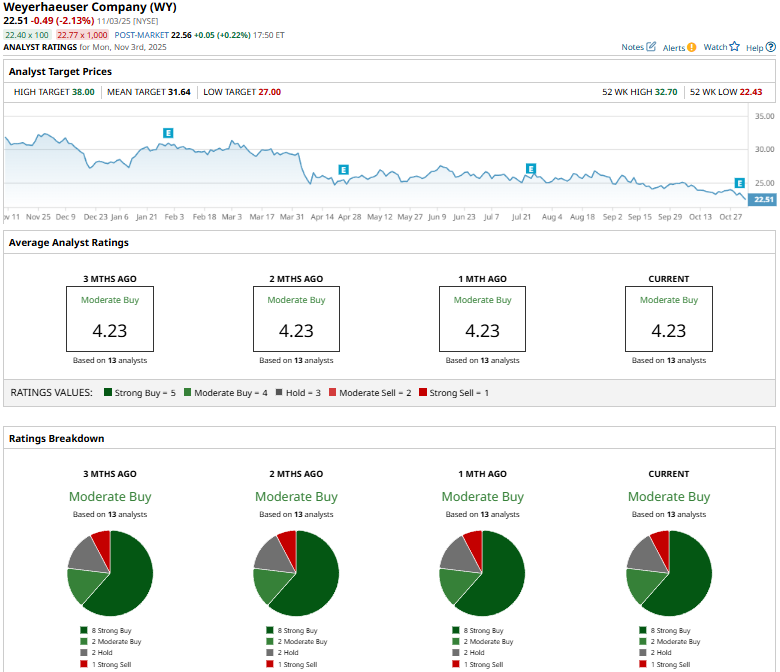

Among the 13 analysts covering the WY stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buys,” two “Moderate Buys,” two “Holds,” and one “Strong Sell.”

This configuration has remained static over the past three months.

On Nov. 3, DA Davidson analyst Kurt Yinger reiterated a “Buy” rating on WY, but reduced the price target from $35 to $31.

WY’s mean price target of $31.64 represents a premium of 40.6% from current price levels. Meanwhile, the street-high target of $38 suggests a notable potential upside of 68.8%.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart