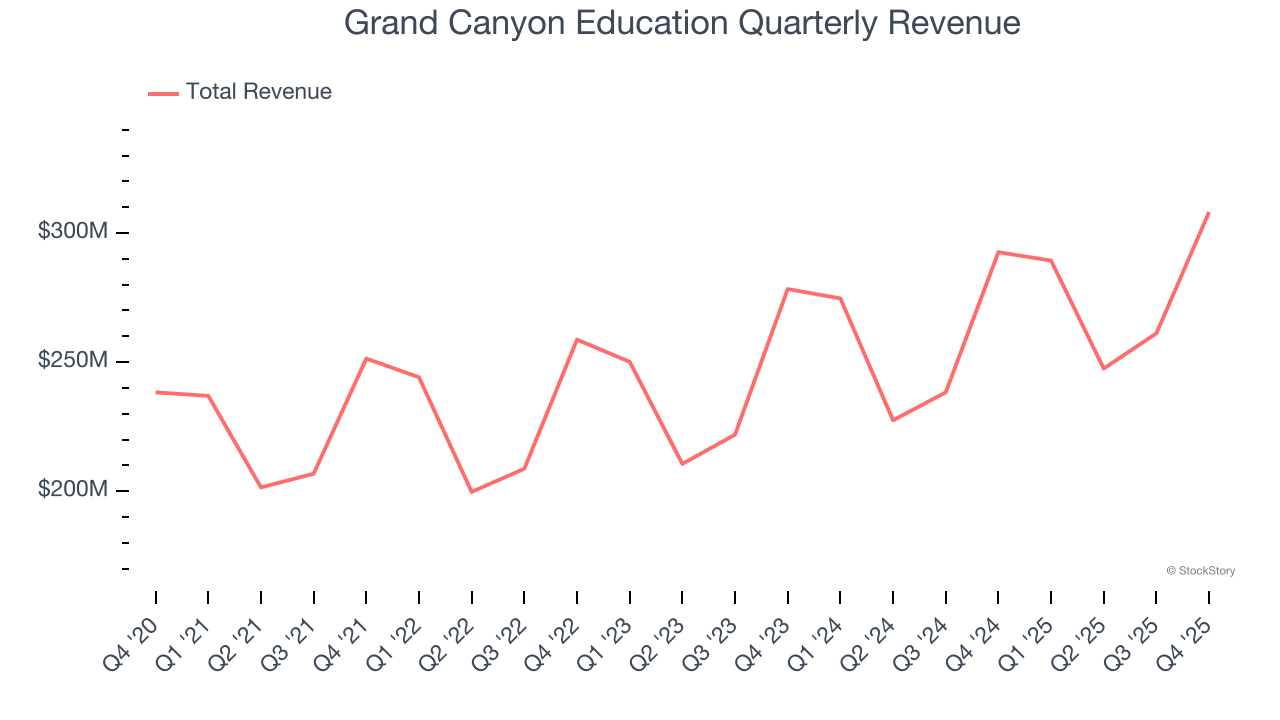

Higher education company Grand Canyon Education (NASDAQ: LOPE) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.3% year on year to $308.1 million. The company expects next quarter’s revenue to be around $333.8 million, coming in 7.9% above analysts’ estimates. Its GAAP profit of $3.14 per share was in line with analysts’ consensus estimates.

Is now the time to buy Grand Canyon Education? Find out by accessing our full research report, it’s free.

Grand Canyon Education (LOPE) Q4 CY2025 Highlights:

- Revenue: $308.1 million vs analyst estimates of $308.1 million (5.3% year-on-year growth, in line)

- EPS (GAAP): $3.14 vs analyst expectations of $3.13 (in line)

- Adjusted EBITDA: $123.3 million vs analyst estimates of $123.8 million (40% margin, in line)

- Revenue Guidance for Q1 CY2026 is $333.8 million at the midpoint, above analyst estimates of $309.3 million

- EPS (GAAP) guidance for the upcoming financial year 2026 is $9.86 at the midpoint, beating analyst estimates by 2%

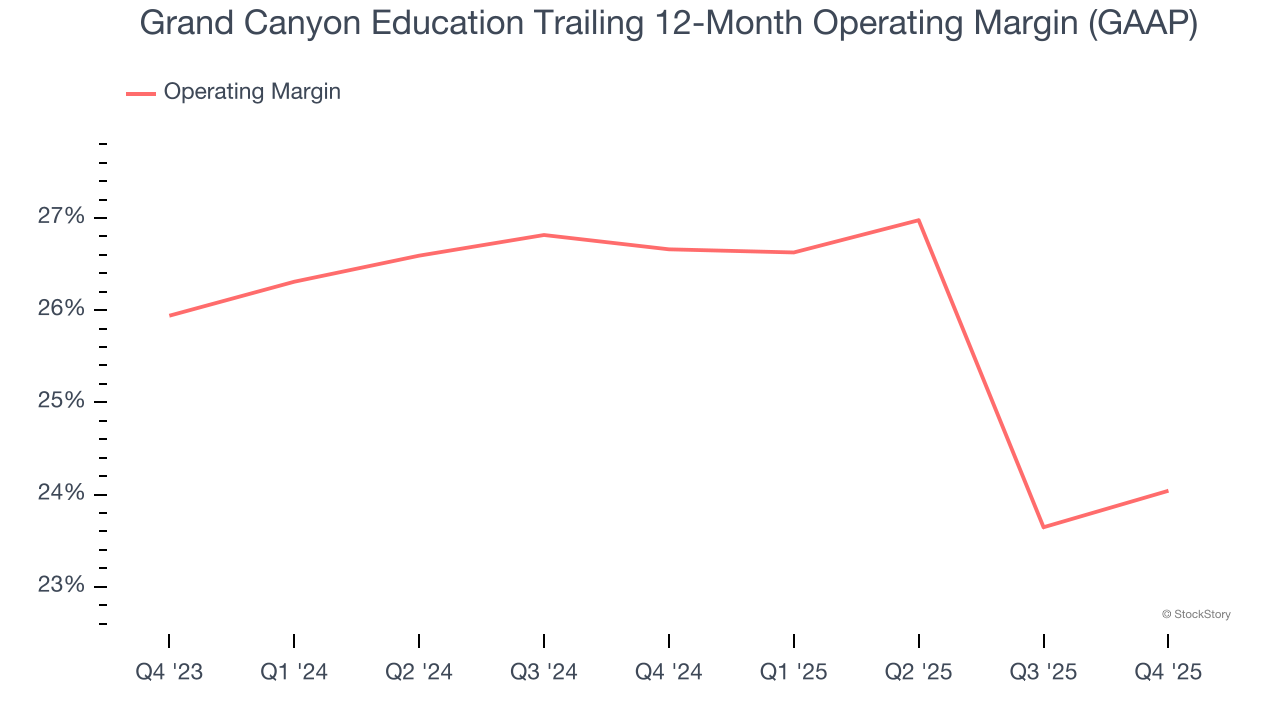

- Operating Margin: 35.1%, in line with the same quarter last year

- Free Cash Flow Margin: 39.9%, down from 43.1% in the same quarter last year

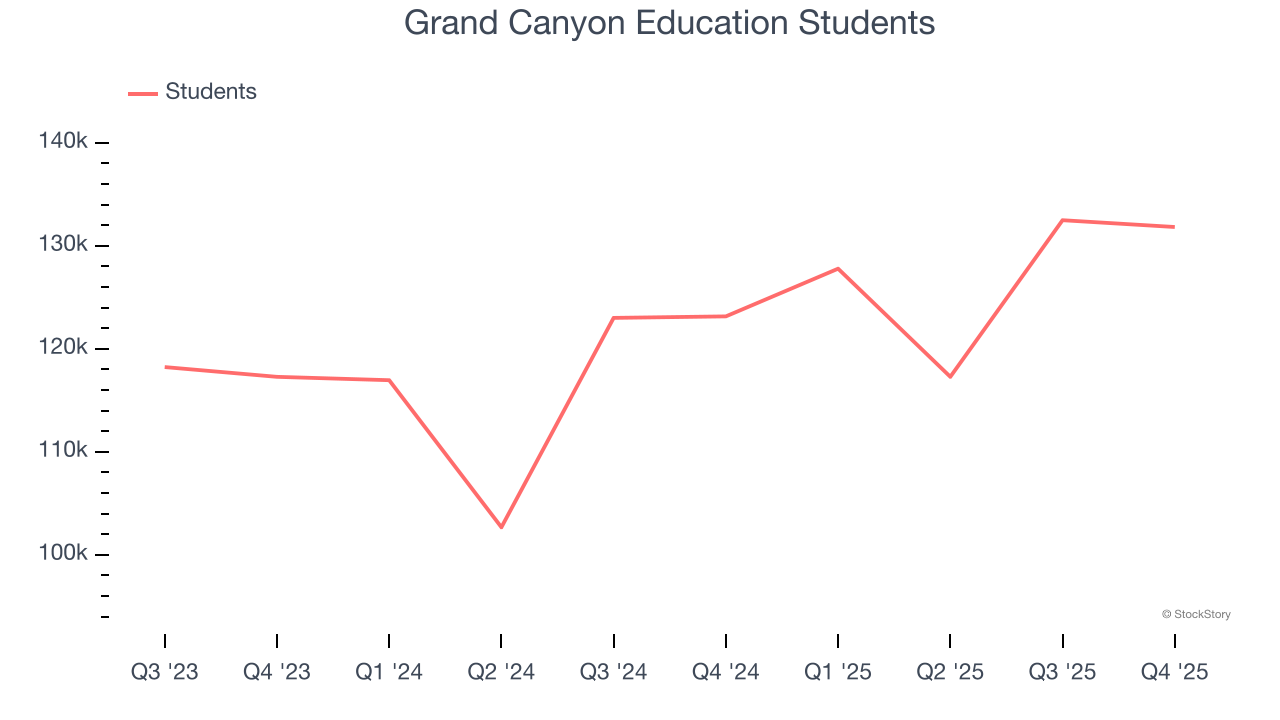

- Students: 131,826, up 8,677 year on year

- Market Capitalization: $4.49 billion

Company Overview

Founded in 1949, Grand Canyon Education (NASDAQ: LOPE) is an educational services provider known for its operation at Grand Canyon University.

Revenue Growth

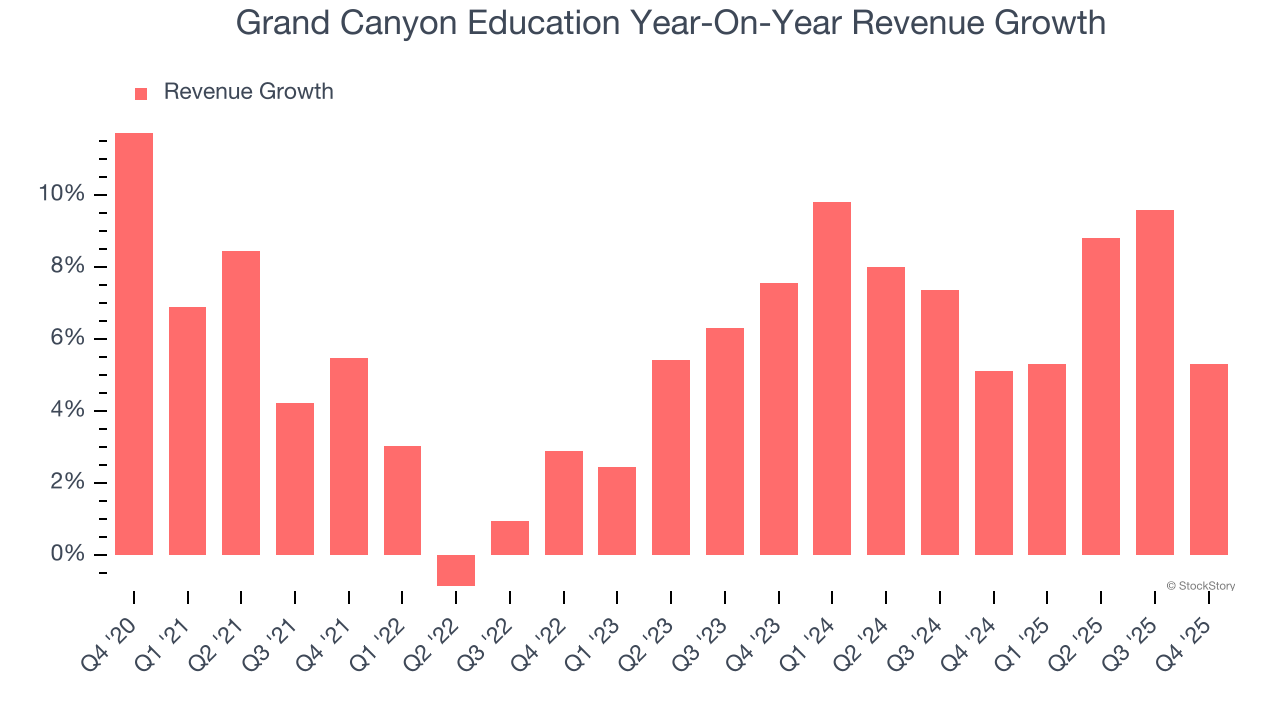

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Grand Canyon Education’s sales grew at a weak 5.6% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Grand Canyon Education’s annualized revenue growth of 7.3% over the last two years is above its five-year trend, which is encouraging.

Grand Canyon Education also discloses its number of students, which reached 131,826 in the latest quarter. Over the last two years, Grand Canyon Education’s students averaged 7.9% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Grand Canyon Education grew its revenue by 5.3% year on year, and its $308.1 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 15.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.8% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Grand Canyon Education’s operating margin has shrunk over the last 12 months and averaged 25.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Grand Canyon Education generated an operating margin profit margin of 35.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

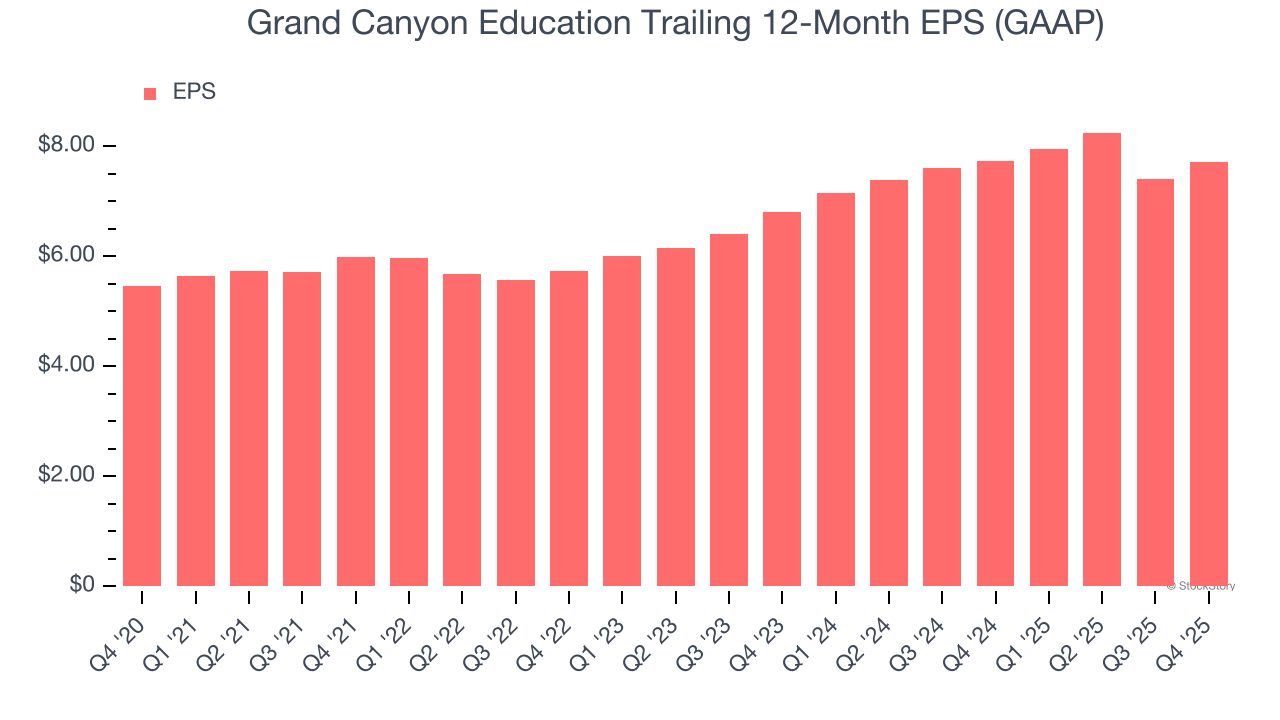

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Grand Canyon Education’s weak 7.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, Grand Canyon Education reported EPS of $3.14, up from $2.84 in the same quarter last year. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Grand Canyon Education’s Q4 Results

We were impressed by Grand Canyon Education’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 3.2% to $162.50 immediately following the results.

Is Grand Canyon Education an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).