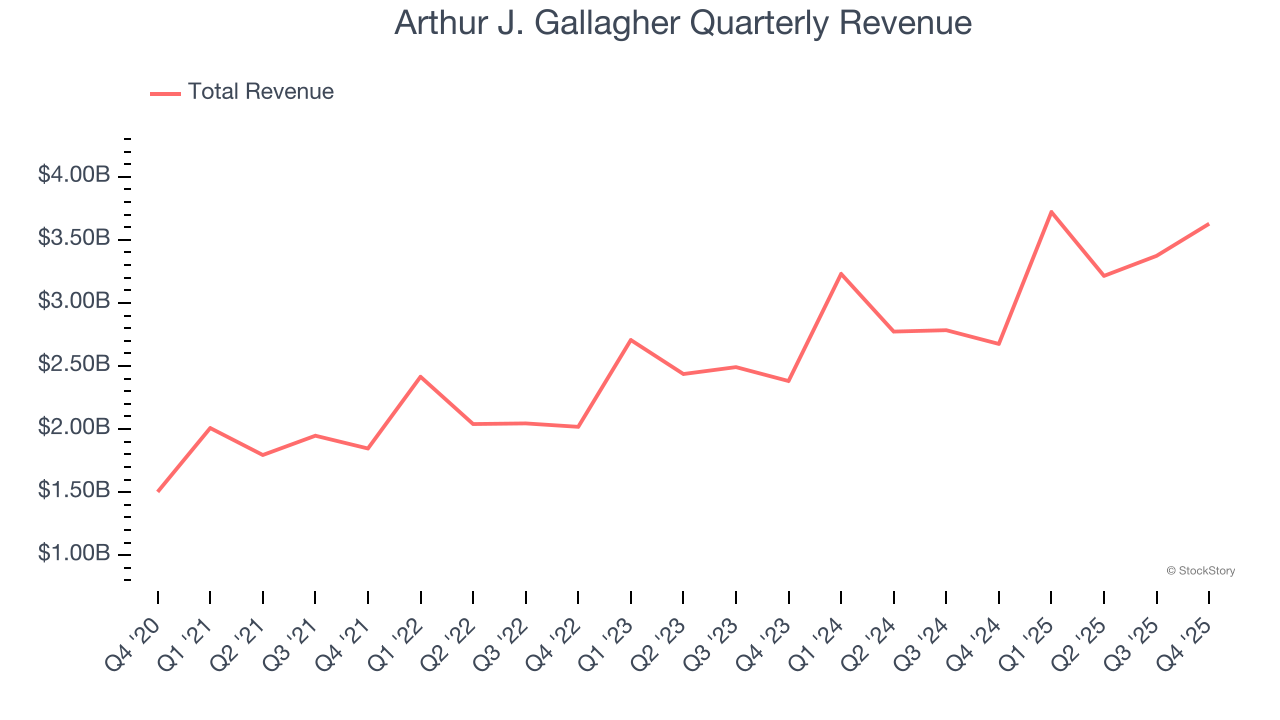

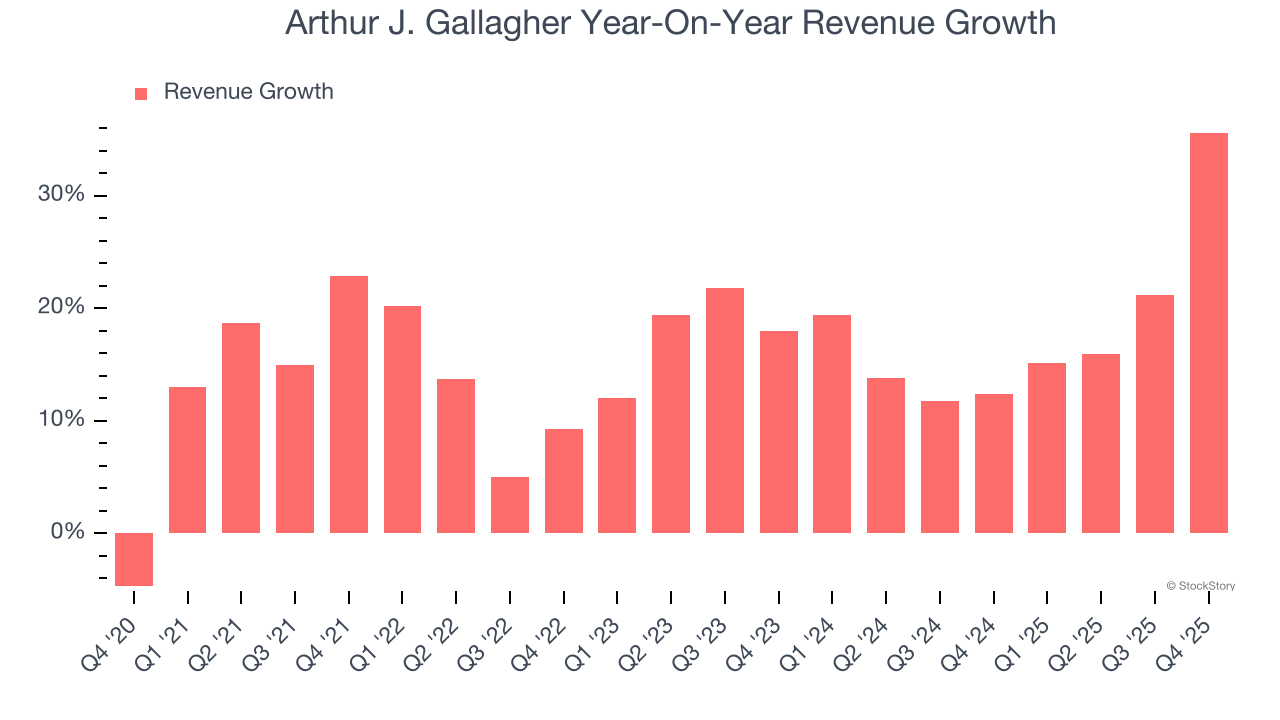

Insurance brokerage firm Arthur J. Gallagher (NYSE: AJG) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 35.6% year on year to $3.63 billion. Its non-GAAP profit of $2.38 per share was 1.4% above analysts’ consensus estimates.

Is now the time to buy Arthur J. Gallagher? Find out by accessing our full research report, it’s free.

Arthur J. Gallagher (AJG) Q4 CY2025 Highlights:

- Revenue: $3.63 billion vs analyst estimates of $3.6 billion (35.6% year-on-year growth, 0.7% beat)

- Adjusted EPS: $2.38 vs analyst estimates of $2.35 (1.4% beat)

- Adjusted EBITDA: $1.05 billion vs analyst estimates of $1.04 billion (28.9% margin, 0.6% beat)

- Market Capitalization: $62.24 billion

"We had an excellent fourth quarter and a terrific 2025!" said J. Patrick Gallagher, Jr., Chairman and CEO.

Company Overview

Founded in 1927 and operating in approximately 130 countries through direct operations and correspondent networks, Arthur J. Gallagher (NYSE: AJG) provides insurance brokerage, reinsurance, consulting, and third-party claims settlement services to businesses and individuals worldwide.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $13.94 billion in revenue over the past 12 months, Arthur J. Gallagher is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

As you can see below, Arthur J. Gallagher’s sales grew at an incredible 16.5% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Arthur J. Gallagher’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Arthur J. Gallagher’s annualized revenue growth of 18% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Arthur J. Gallagher reported wonderful year-on-year revenue growth of 35.6%, and its $3.63 billion of revenue exceeded Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to grow 22.6% over the next 12 months, an improvement versus the last two years. This projection is eye-popping for a company of its scale and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

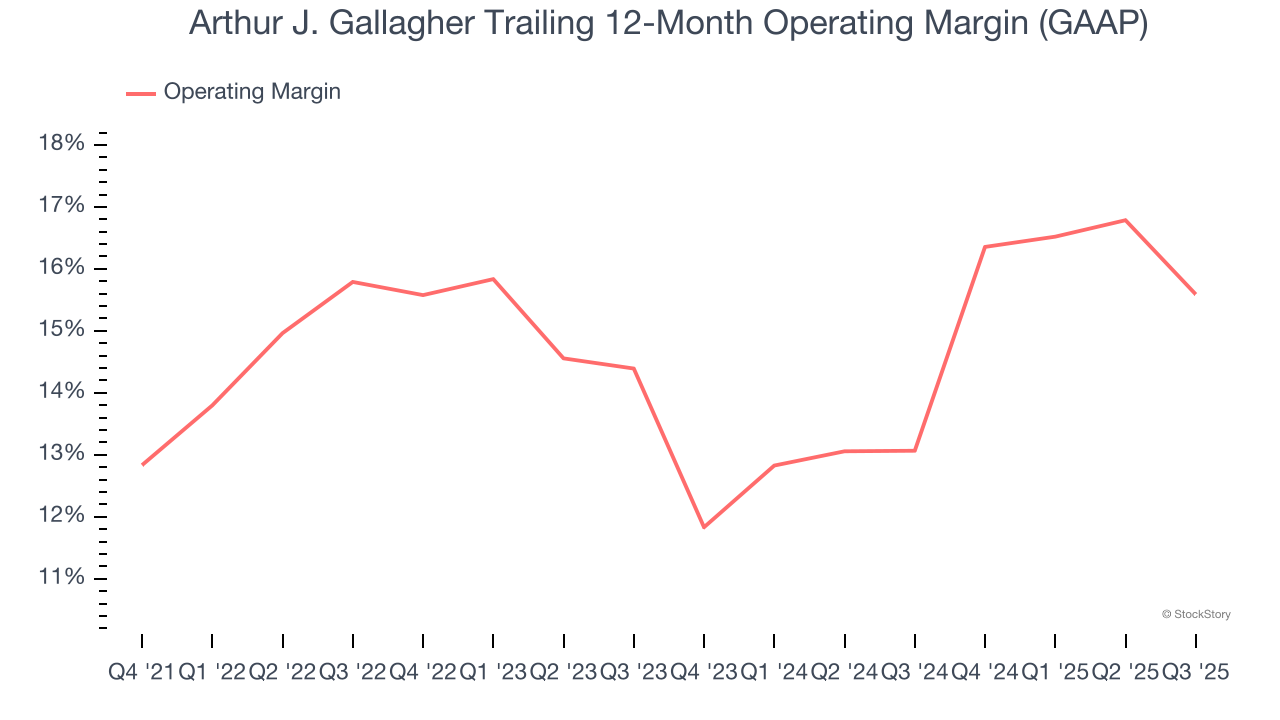

Operating Margin

Arthur J. Gallagher has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 14.7%.

Analyzing the trend in its profitability, Arthur J. Gallagher’s operating margin rose by 1.4 percentage points over the last five years, as its sales growth gave it operating leverage.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

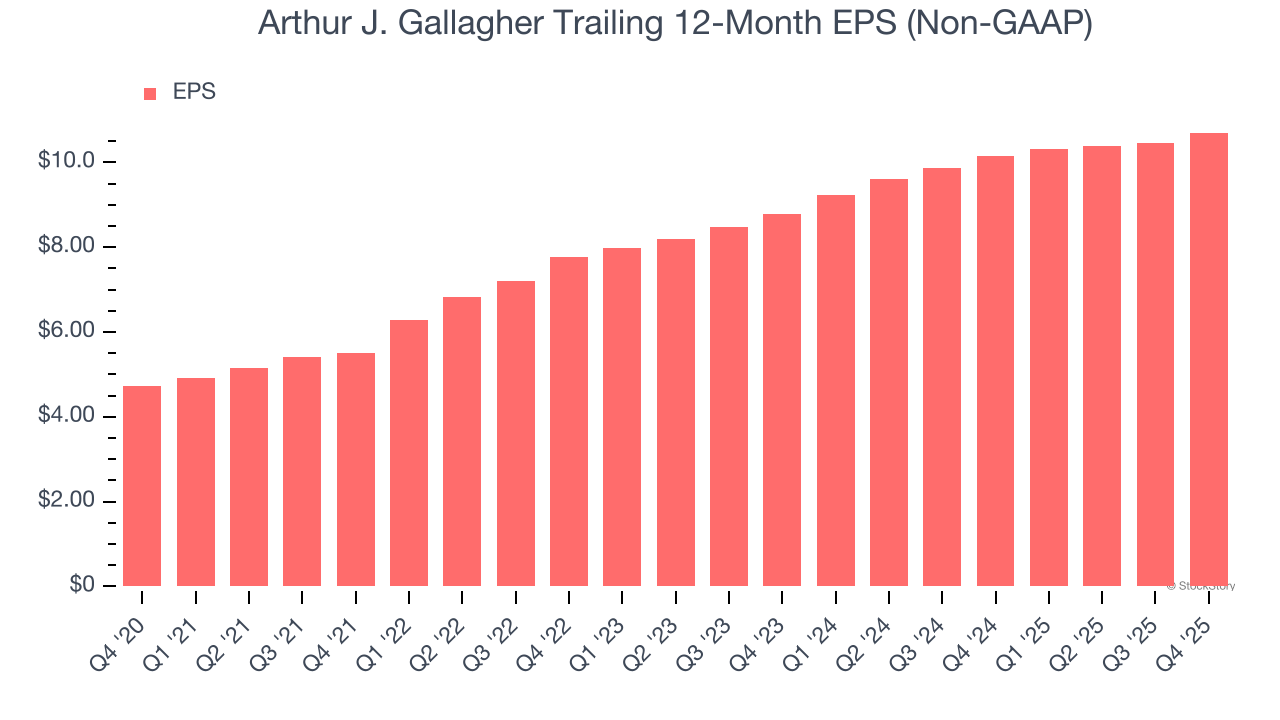

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Arthur J. Gallagher’s astounding 17.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Although it performed well, Arthur J. Gallagher’s two-year annual EPS growth of 10.4% lower than its 18% two-year revenue growth.

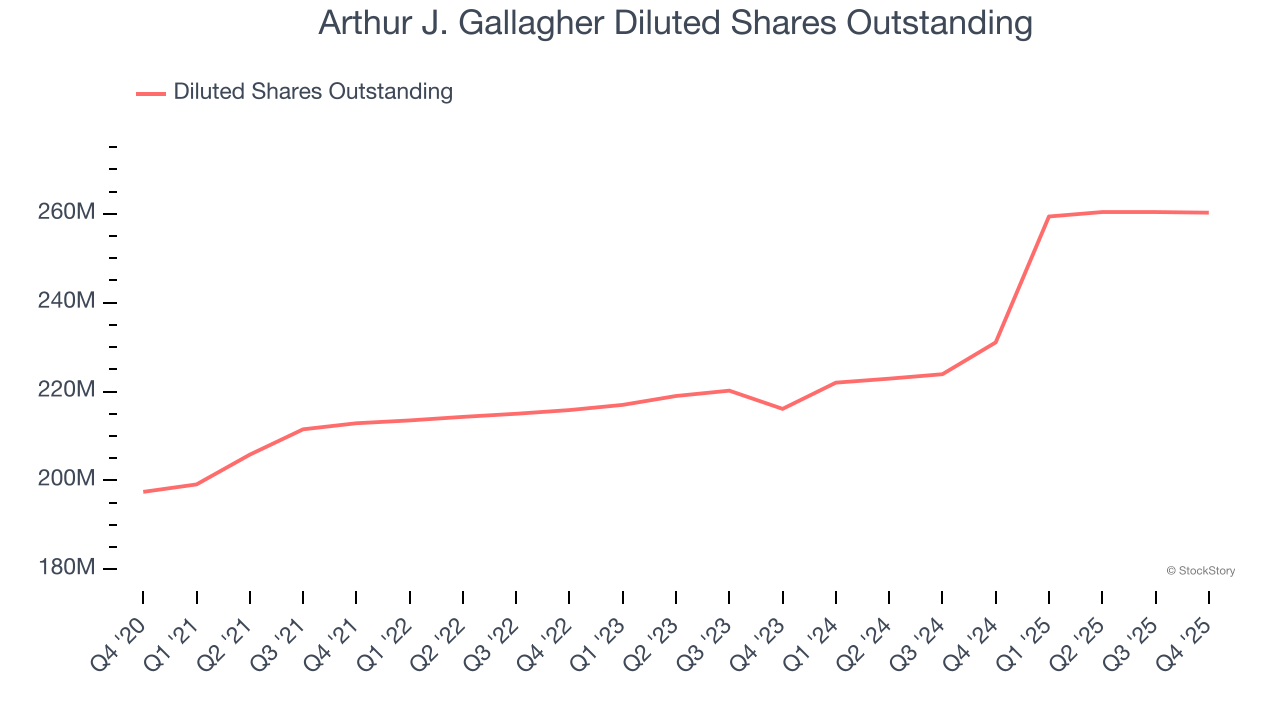

We can take a deeper look into Arthur J. Gallagher’s earnings quality to better understand the drivers of its performance. A two-year view shows Arthur J. Gallagher has diluted its shareholders, growing its share count by 20.4%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Arthur J. Gallagher reported adjusted EPS of $2.38, up from $2.13 in the same quarter last year. This print beat analysts’ estimates by 1.4%. Over the next 12 months, Wall Street expects Arthur J. Gallagher’s full-year EPS of $10.70 to grow 23.9%.

Key Takeaways from Arthur J. Gallagher’s Q4 Results

It was good to see Arthur J. Gallagher narrowly top analysts’ revenue expectations this quarter, leading to an EPS beat. Overall, this print had some key positives. The stock traded up 1.7% to $249.91 immediately following the results.

Is Arthur J. Gallagher an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).