As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q2. Today, we are looking at office & commercial furniture stocks, starting with MillerKnoll (NASDAQ: MLKN).

The sector faces a tepid outlook as workplace dynamics continue to evolve. Hybrid work means that enterprise demand for office furniture is lower. Consumer demand for the same products likely will not offset the loss from enterprises, as individual workers tend to have less space and need for the sector's wares. The Trump administration also possesses a high willingness to impose tariffs on key partners, which could result in retaliatory actions, all of which could pressure those selling furniture that may feature components or labor from overseas. Lastly, the COVID-19 pandemic showed that there is always a risk that something disrupts supply chains, and companies need contingency plans for this.

The 4 office & commercial furniture stocks we track reported a very strong Q2. As a group, revenues beat analysts’ consensus estimates by 3.9% while next quarter’s revenue guidance was 0.7% above.

Luckily, office & commercial furniture stocks have performed well with share prices up 17.8% on average since the latest earnings results.

MillerKnoll (NASDAQ: MLKN)

Created through the 2021 merger of industry icons Herman Miller and Knoll, MillerKnoll (NASDAQ: MLKN) designs, manufactures, and distributes interior furnishings for offices, healthcare facilities, educational settings, and homes worldwide.

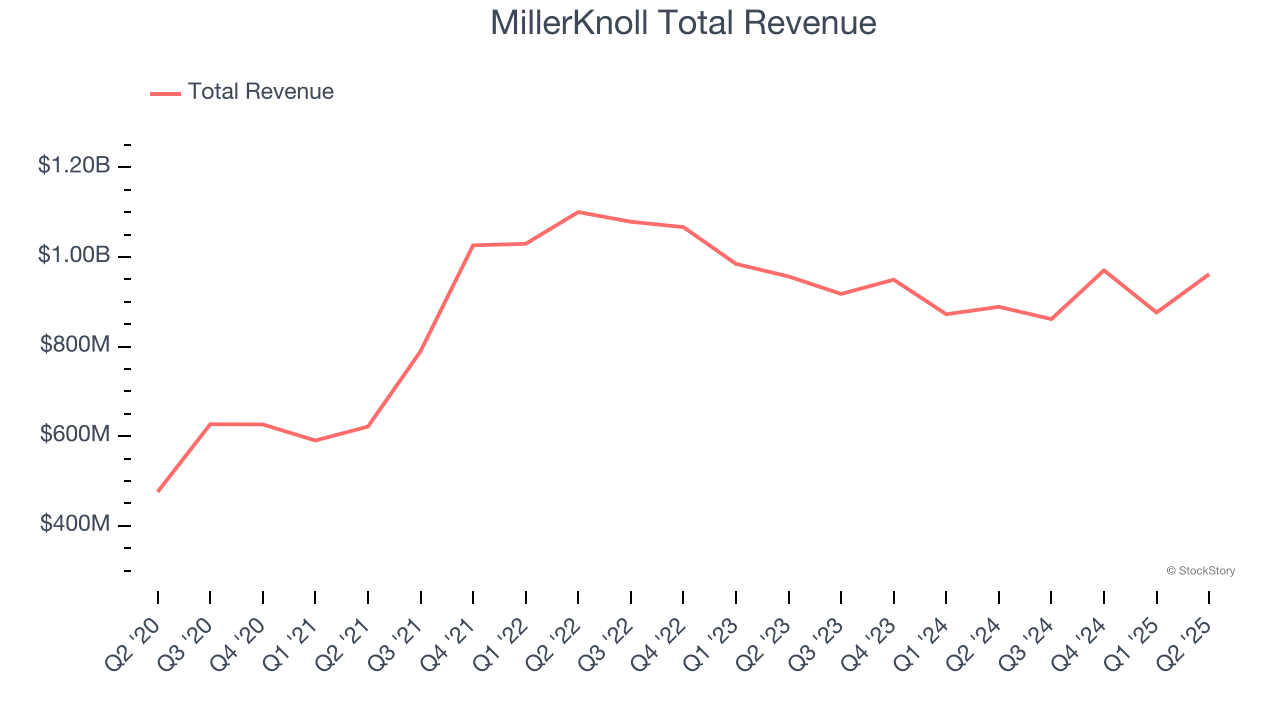

MillerKnoll reported revenues of $961.8 million, up 8.2% year on year. This print exceeded analysts’ expectations by 5.3%. Overall, it was a stunning quarter for the company with a solid beat of analysts’ EPS estimates and revenue guidance for next quarter exceeding analysts’ expectations.

MillerKnoll scored the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 12.1% since reporting and currently trades at $19.78.

Is now the time to buy MillerKnoll? Access our full analysis of the earnings results here, it’s free.

Best Q2: HNI (NYSE: HNI)

With roots dating back to 1944 and a significant acquisition of Kimball International in 2023, HNI (NYSE: HNI) manufactures and sells office furniture systems, seating, and storage solutions, as well as residential fireplaces and heating products.

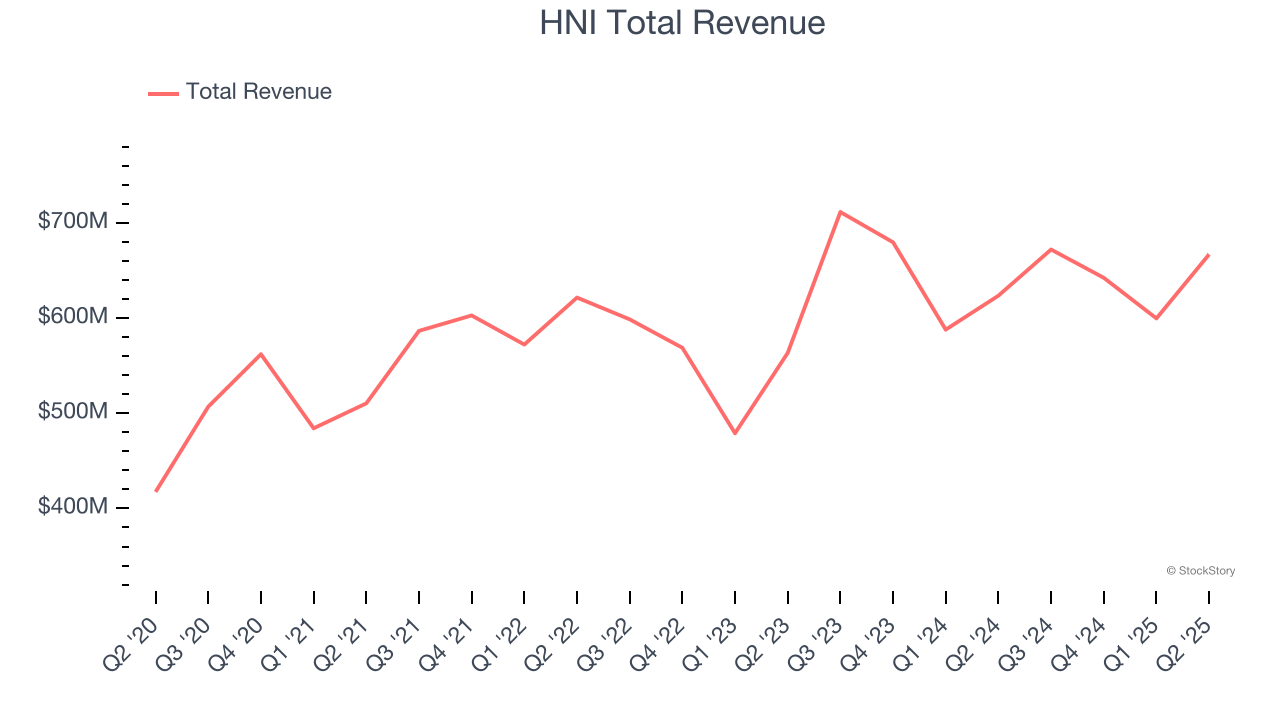

HNI reported revenues of $667.1 million, up 7% year on year, outperforming analysts’ expectations by 3.2%. The business had a stunning quarter with a solid beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 16% since reporting. It currently trades at $44.14.

Is now the time to buy HNI? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Steelcase (NYSE: SCS)

Founded in 1912 when metal office furniture was replacing wooden alternatives, Steelcase (NYSE: SCS) is a global office furniture manufacturer that designs and produces workplace solutions including desks, chairs, architectural products, and services.

Steelcase reported revenues of $779 million, up 7.1% year on year, exceeding analysts’ expectations by 2.5%. Still, it was a mixed quarter as it posted a significant miss of analysts’ EPS guidance for next quarter estimates.

Steelcase delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 50.6% since the results and currently trades at $16.01.

Read our full analysis of Steelcase’s results here.

Interface (NASDAQ: TILE)

Pioneering carbon-neutral flooring since its founding in 1973, Interface (NASDAQ: TILE) is a global manufacturer of modular carpet tiles, luxury vinyl tile (LVT), and rubber flooring that specializes in carbon-neutral and sustainable flooring solutions.

Interface reported revenues of $375.5 million, up 8.3% year on year. This result topped analysts’ expectations by 4.6%. It was a very strong quarter as it also recorded a solid beat of analysts’ EPS estimates and full-year revenue guidance topping analysts’ expectations.

Interface pulled off the fastest revenue growth among its peers. The stock is up 24.6% since reporting and currently trades at $25.71.

Read our full, actionable report on Interface here, it’s free.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.