Over the past six months, Snap’s shares (currently trading at $8.61) have posted a disappointing 18.4% loss while the S&P 500 was flat. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Snap, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Snap Not Exciting?

Despite the more favorable entry price, we're swiping left on Snap for now. Here are three reasons why we avoid SNAP and a stock we'd rather own.

1. Customer Spending Stalls, Engagement Falling?

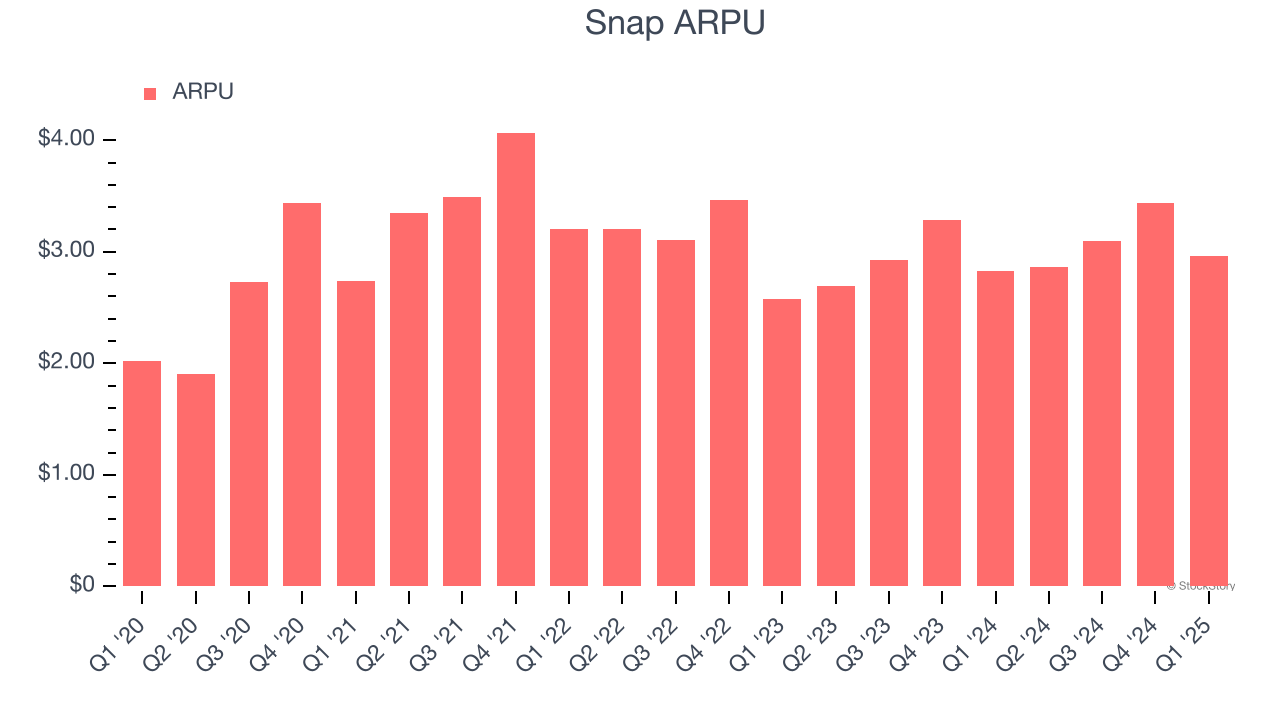

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Snap’s audience and its ad-targeting capabilities.

Snap’s ARPU has been roughly flat over the last two years. This isn’t great, but the increase in daily active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Snap tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

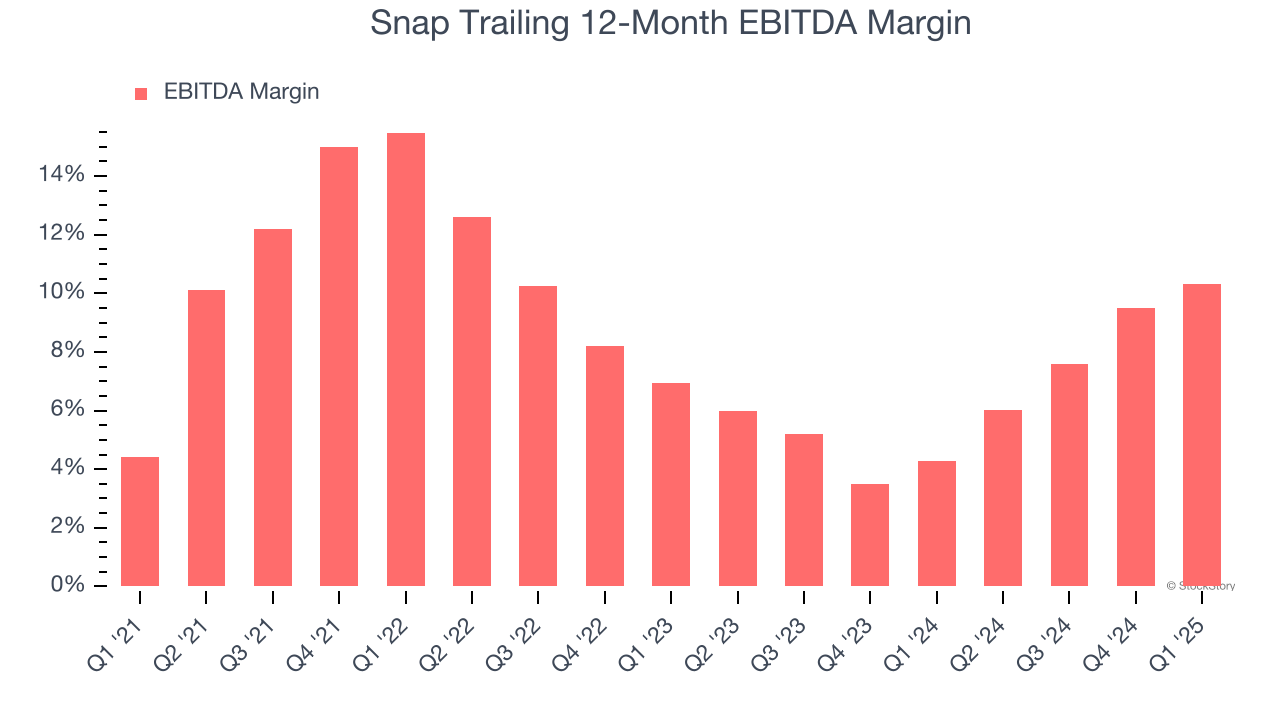

2. Shrinking EBITDA Margin

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Looking at the trend in its profitability, Snap’s EBITDA margin decreased by 5.2 percentage points over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 10.3%.

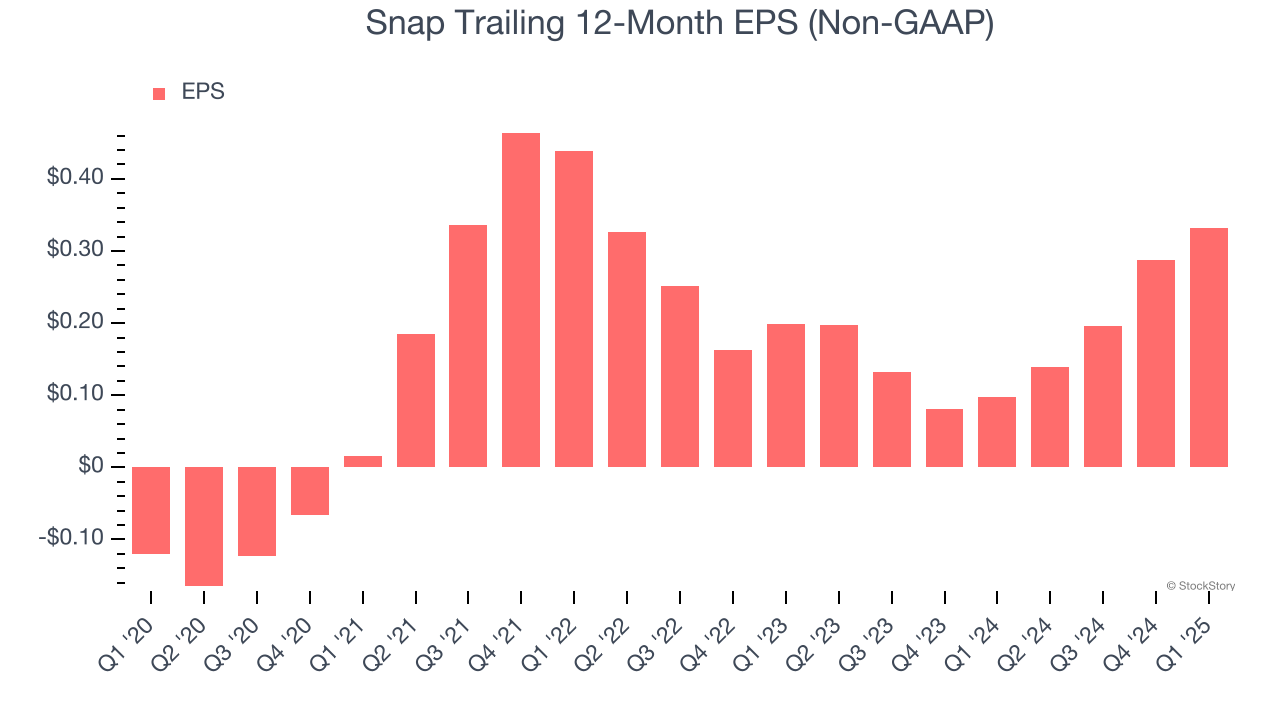

3. EPS Trending Down

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Snap, its EPS declined by 8.9% annually over the last three years while its revenue grew by 7.8%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Snap’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 22.4× forward EV/EBITDA (or $8.61 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d recommend looking at the Amazon and PayPal of Latin America.

Stocks We Like More Than Snap

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.