Semrush’s stock price has taken a beating over the past six months, shedding 20.1% of its value and falling to $10.33 per share. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now the time to buy SEMR? Find out in our full research report, it’s free.

Why Are We Positive On SEMR?

Started by Oleg Shchegolev while still in university, Semrush (NYSE: SEMR) is a software-as-a-service platform that helps companies optimize their search engine and content marketing efforts.

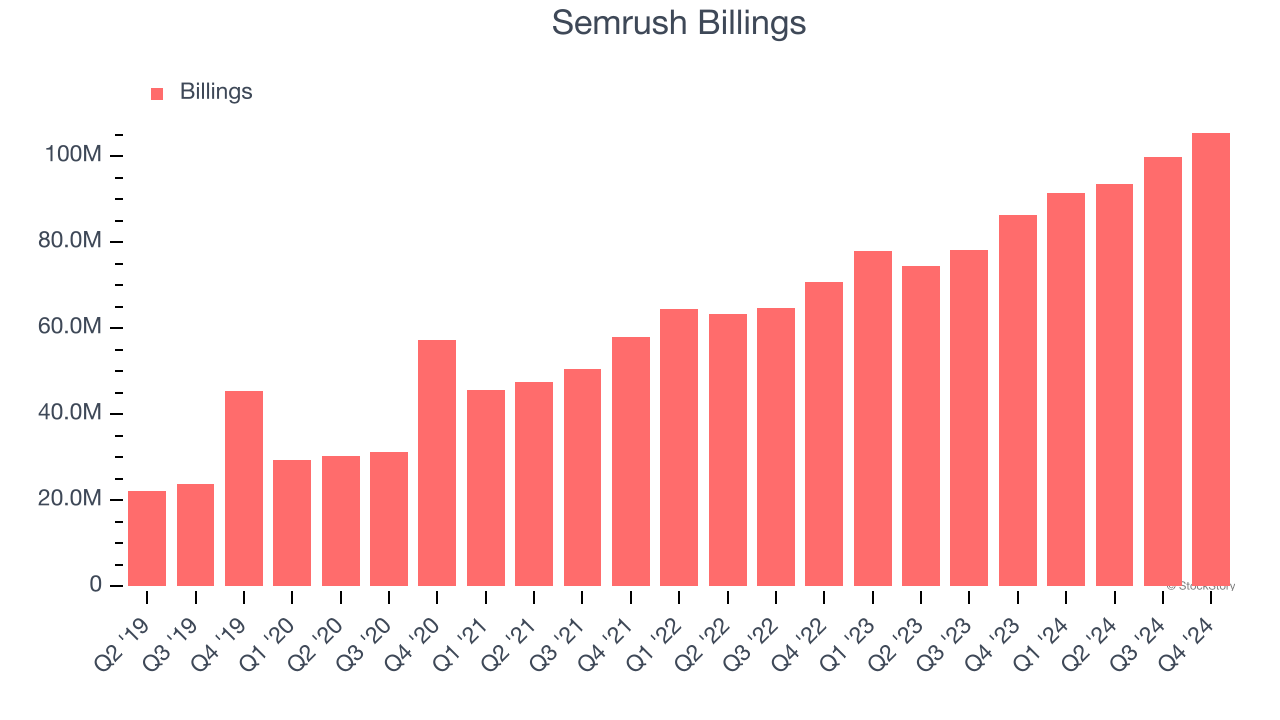

1. Billings Surge, Boosting Cash On Hand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Semrush’s billings punched in at $105.5 million in Q4, and over the last four quarters, its year-on-year growth averaged 23.2%. This performance was impressive, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

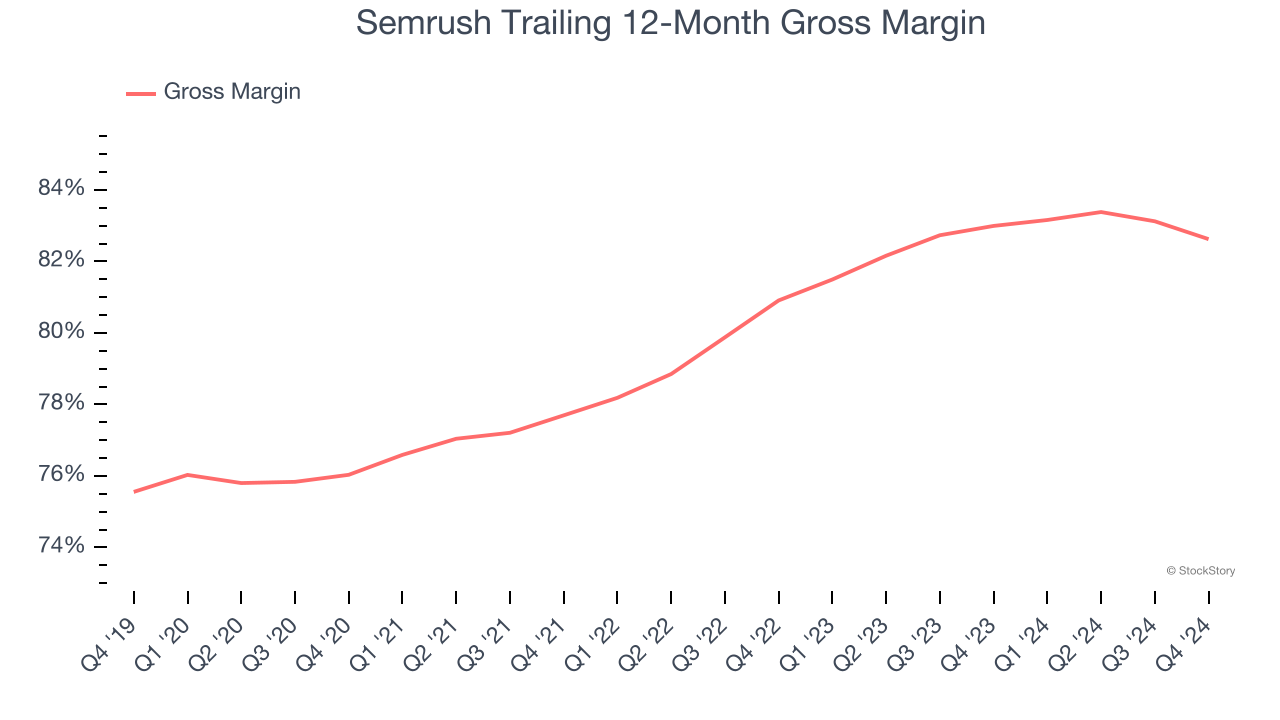

2. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Semrush’s gross margin is one of the best in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 82.6% gross margin over the last year. That means Semrush only paid its providers $17.38 for every $100 in revenue.

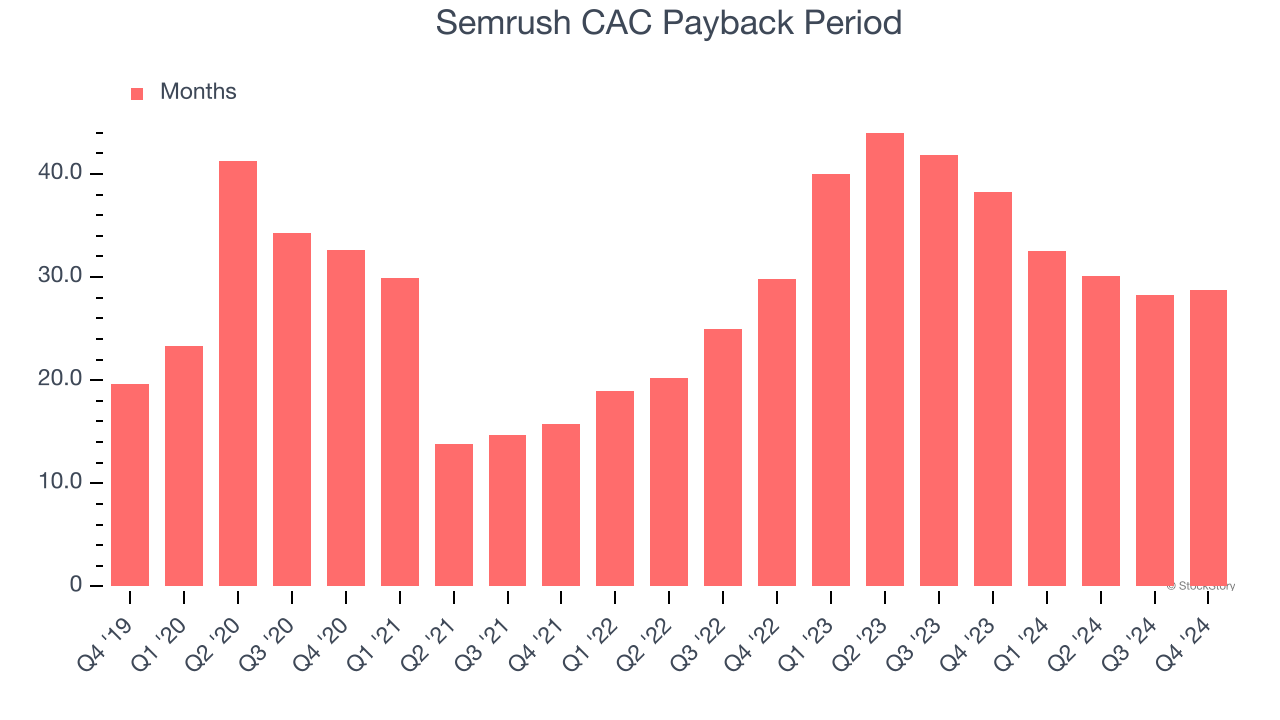

3. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Semrush is very efficient at acquiring new customers, and its CAC payback period checked in at 28.7 months this quarter. The company’s rapid sales cycles stem from its strong brand reputation and self-serve model, where it can onboard many small customers with little to no oversight. These dynamics give Semrush more resources to pursue new product initiatives so it can potentially move up market and serve enterprise clients, which can provide a second leg of growth.

Final Judgment

These are just a few reasons why we think Semrush is a great business. With the recent decline, the stock trades at 3.5× forward price-to-sales (or $10.33 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Semrush

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.