Diversified manufacturing and supply chain services provider Park-Ohio (NASDAQ: PKOH) missed Wall Street’s revenue expectations in Q4 CY2024, with sales flat year on year at $388.4 million. Its non-GAAP profit of $0.67 per share was 8.1% above analysts’ consensus estimates.

Is now the time to buy Park-Ohio? Find out by accessing our full research report, it’s free.

Park-Ohio (PKOH) Q4 CY2024 Highlights:

- Revenue: $388.4 million vs analyst estimates of $405.9 million (flat year on year, 4.3% miss)

- Adjusted EPS: $0.67 vs analyst estimates of $0.62 (8.1% beat)

- Adjusted EBITDA: $37 million vs analyst estimates of $32.65 million (9.5% margin, 13.3% beat)

- Operating Margin: 3.7%, in line with the same quarter last year

- Free Cash Flow Margin: 4.5%, down from 5.7% in the same quarter last year

- Market Capitalization: $306 million

Company Overview

Based in Cleveland, Park-Ohio (NASDAQ: PKOH) provides supply chain management services, capital equipment, and manufactured components.

Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

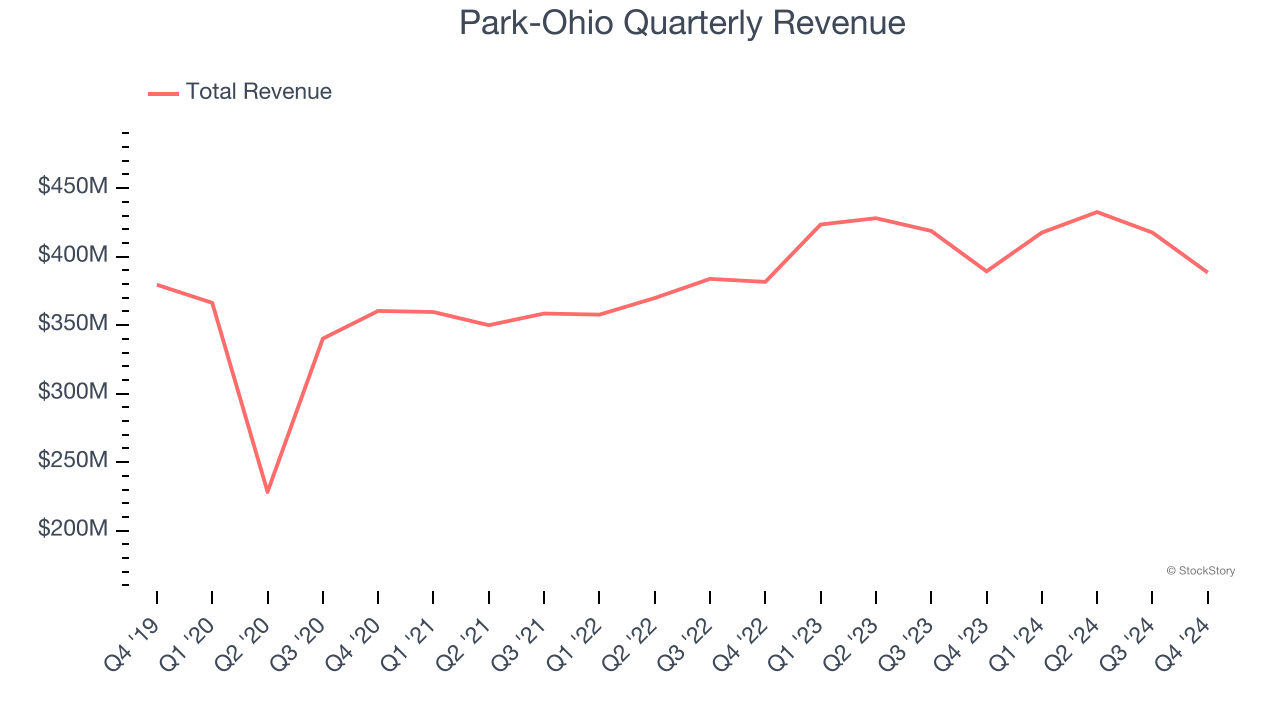

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Park-Ohio struggled to consistently increase demand as its $1.66 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

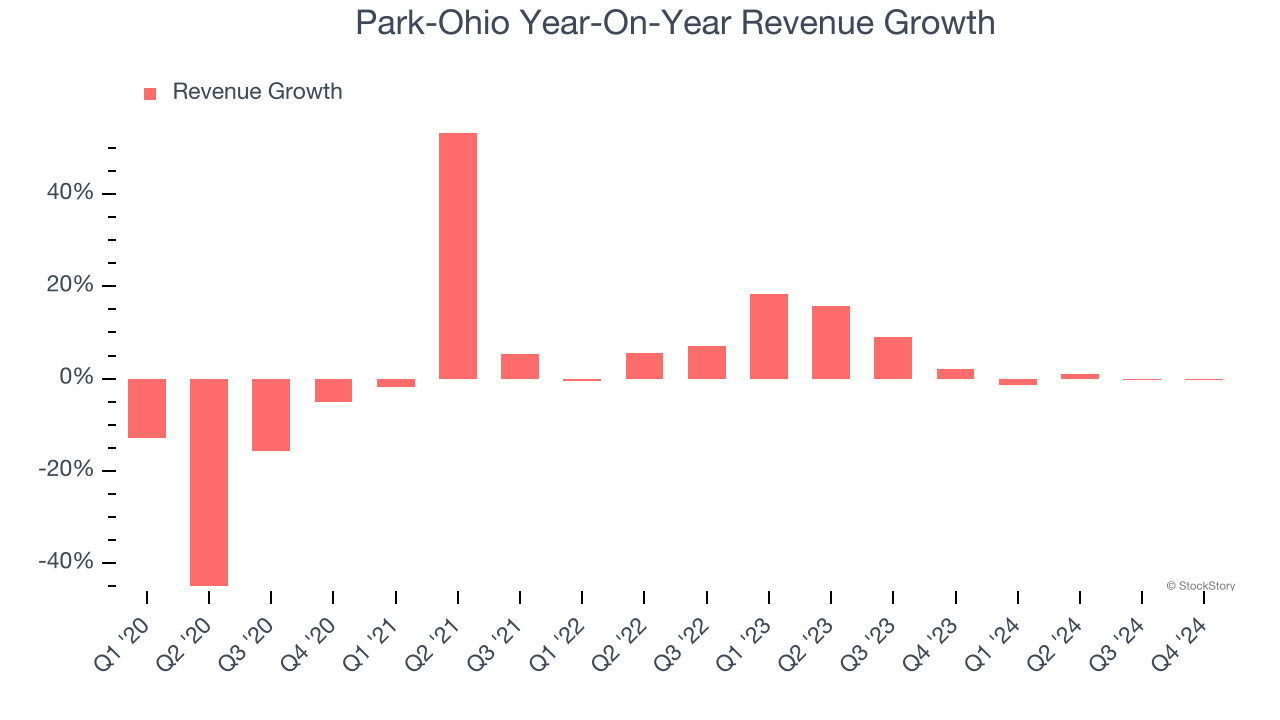

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Park-Ohio’s annualized revenue growth of 5.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Park-Ohio missed Wall Street’s estimates and reported a rather uninspiring 0.2% year-on-year revenue decline, generating $388.4 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, similar to its two-year rate. Although this projection suggests its newer products and services will spur better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

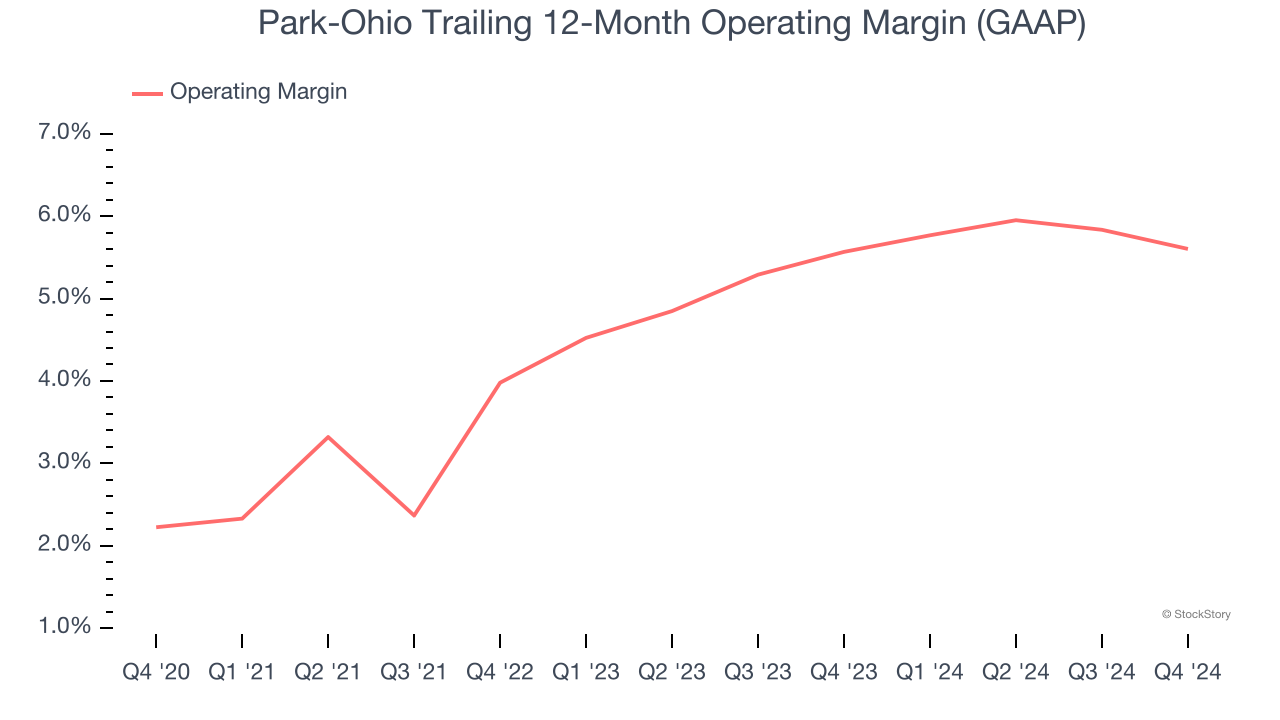

Park-Ohio was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.1% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Park-Ohio’s operating margin rose by 3.4 percentage points over the last five years.

In Q4, Park-Ohio generated an operating profit margin of 3.7%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

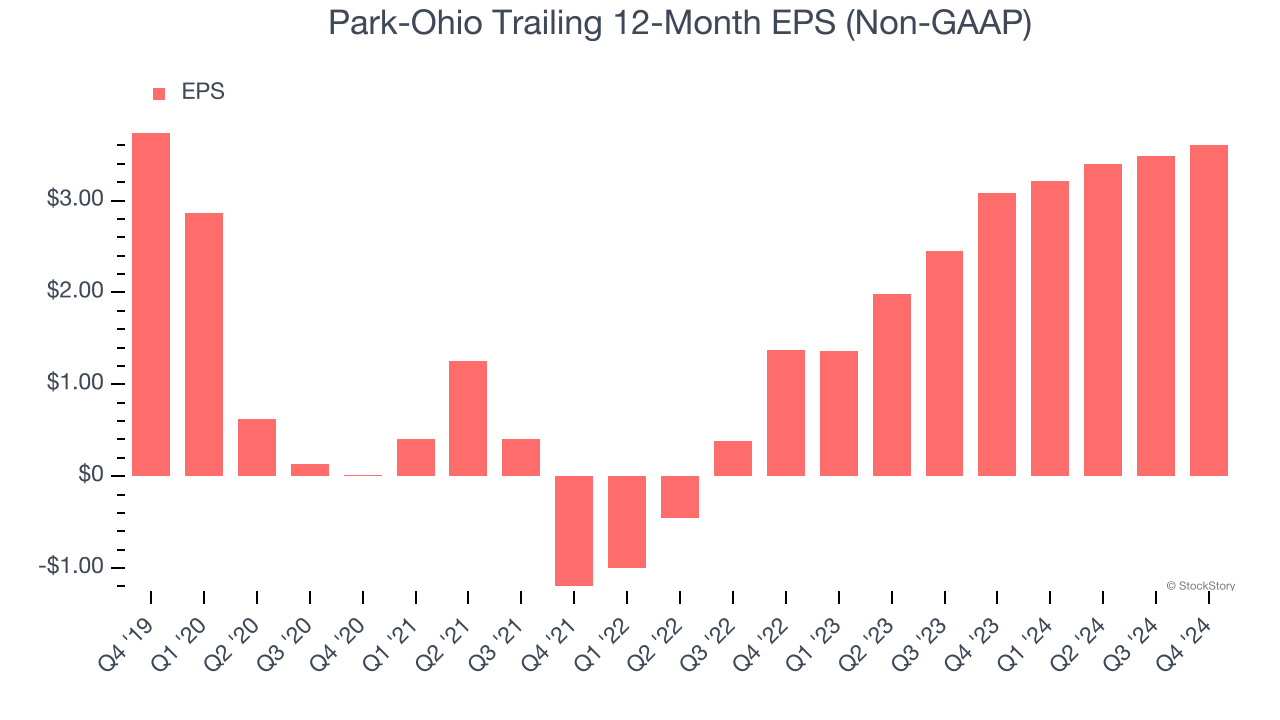

Park-Ohio’s EPS was flat over the last five years, just like its revenue. This performance was underwhelming across the board.

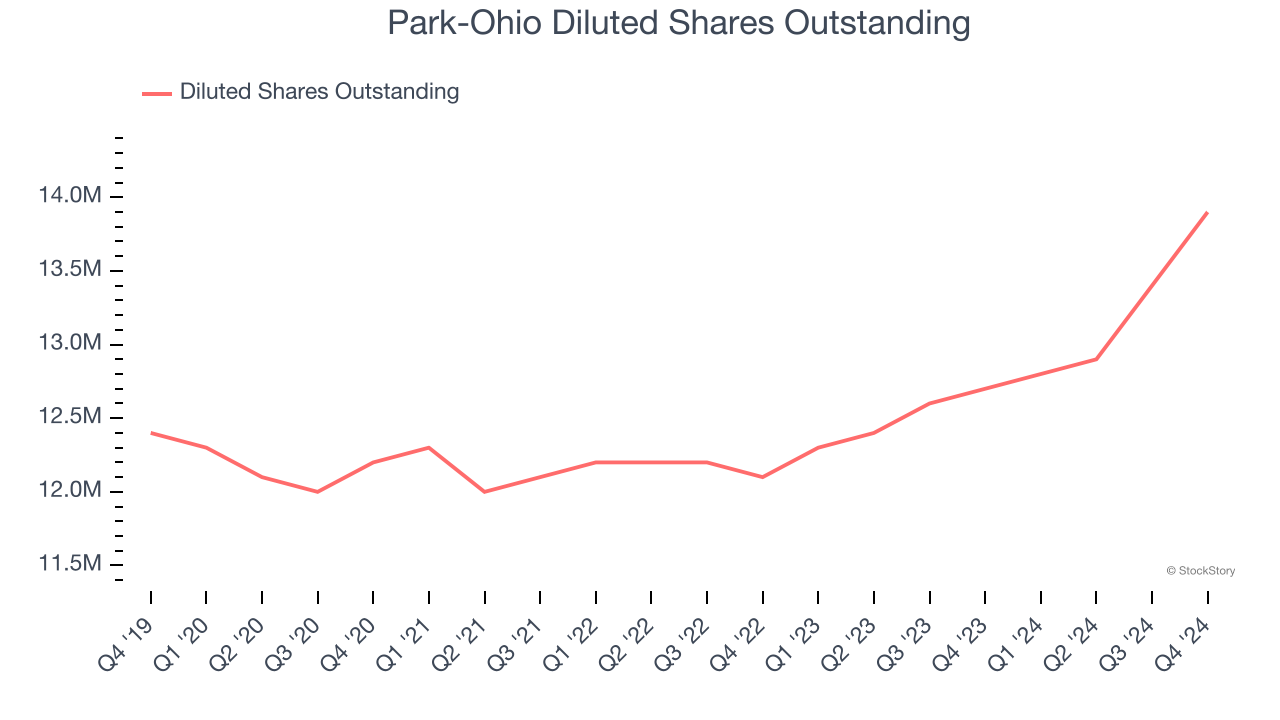

We can take a deeper look into Park-Ohio’s earnings to better understand the drivers of its performance. A five-year view shows Park-Ohio has diluted its shareholders, growing its share count by 12.1%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Park-Ohio, its two-year annual EPS growth of 62.3% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Park-Ohio reported EPS at $0.67, up from $0.54 in the same quarter last year. This print beat analysts’ estimates by 8.1%. Over the next 12 months, Wall Street expects Park-Ohio’s full-year EPS of $3.61 to grow 1.7%.

Key Takeaways from Park-Ohio’s Q4 Results

We were impressed by how significantly Park-Ohio beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed significantly. Overall, this quarter was mixed. The stock traded down 1.3% to $22.80 immediately following the results.

Is Park-Ohio an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.