Over the last six months, Ingersoll Rand shares have sunk to $82.99, producing a disappointing 8.8% loss - worse than the S&P 500’s 1.1% drop. This may have investors wondering how to approach the situation.

Given the weaker price action, is now an opportune time to buy IR? Find out in our full research report, it’s free.

Why Does Ingersoll Rand Spark Debate?

Started with the invention of the steam drill, Ingersoll Rand (NYSE: IR) provides mission-critical air, gas, liquid, and solid flow creation solutions.

Two Things to Like:

1. Skyrocketing Revenue Shows Strong Momentum

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Ingersoll Rand’s annualized revenue growth of 10.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

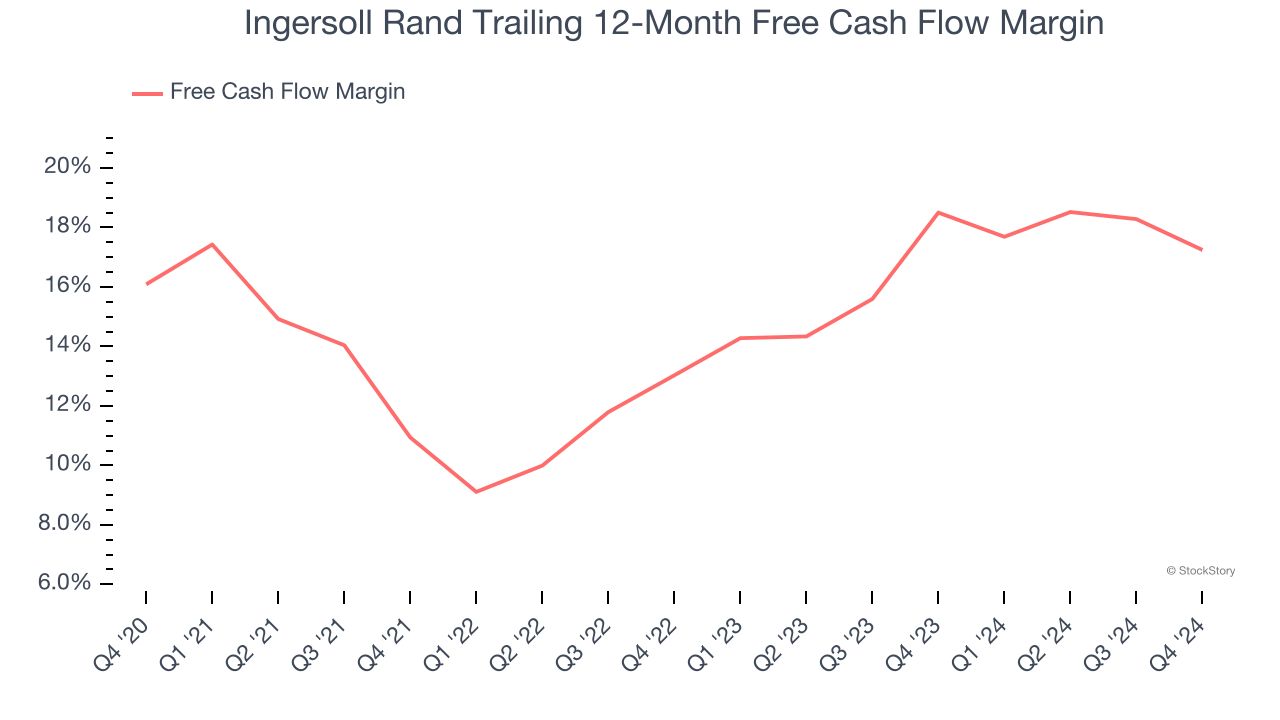

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Ingersoll Rand has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 15.4% over the last five years.

One Reason to be Careful:

Slow Organic Growth Suggests Waning Demand In Core Business

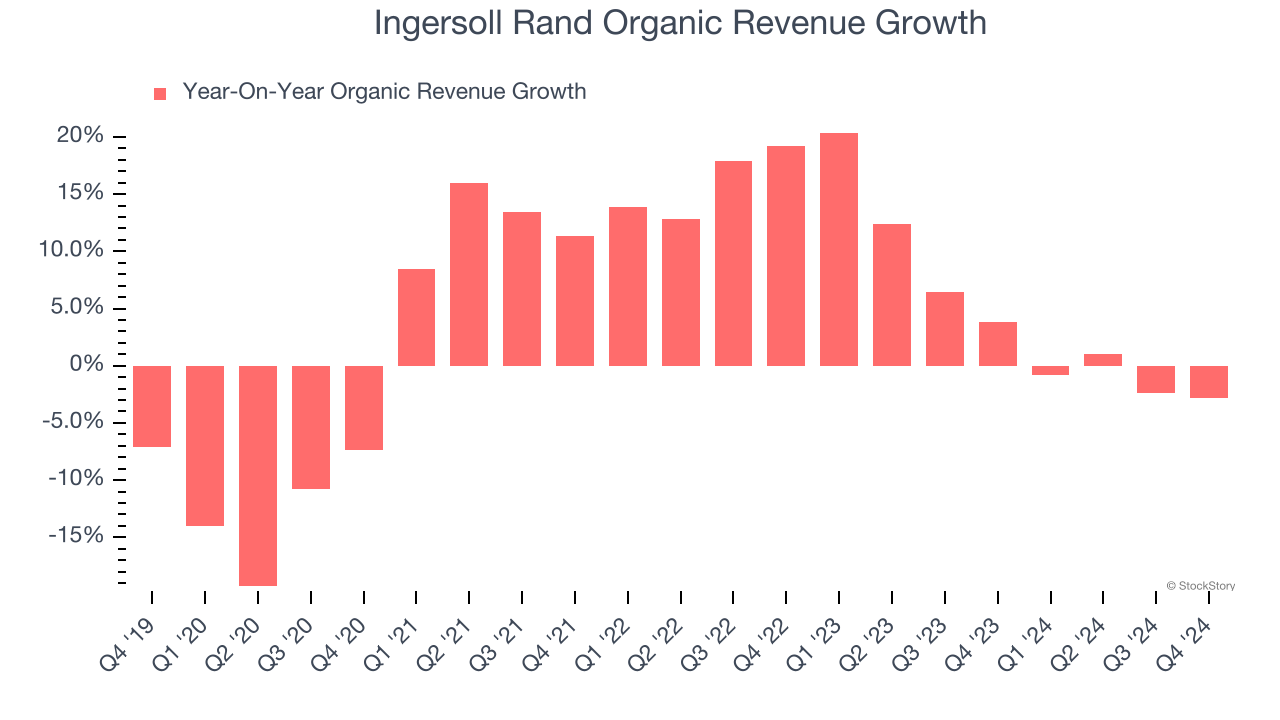

Investors interested in Gas and Liquid Handling companies should track organic revenue in addition to reported revenue. This metric gives visibility into Ingersoll Rand’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Ingersoll Rand’s organic revenue averaged 4.8% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Ingersoll Rand’s merits more than compensate for its flaws. With the recent decline, the stock trades at 23.7× forward price-to-earnings (or $82.99 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Ingersoll Rand

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.