Coconut water company The Vita Coco Company (NASDAQ: COCO) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 19.9% year on year to $127.3 million. On the other hand, the company’s full-year revenue guidance of $562.5 million at the midpoint came in 1.2% below analysts’ estimates. Its GAAP profit of $0.06 per share was in line with analysts’ consensus estimates.

Is now the time to buy Vita Coco? Find out by accessing our full research report, it’s free.

Vita Coco (COCO) Q4 CY2024 Highlights:

- Revenue: $127.3 million vs analyst estimates of $121.9 million (19.9% year-on-year growth, 4.4% beat)

- EPS (GAAP): $0.06 vs analyst estimates of $0.06 (in line)

- Adjusted EBITDA: $7.73 million vs analyst estimates of $6.05 million (6.1% margin, 27.8% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $562.5 million at the midpoint, missing analyst estimates by 1.2% and implying 9% growth (vs 5.3% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $89 million at the midpoint, below analyst estimates of $91.54 million

- Operating Margin: 3.4%, down from 5.1% in the same quarter last year

- Free Cash Flow Margin: 5.3%, down from 34.9% in the same quarter last year

- Sales Volumes rose 19.3% year on year (3% in the same quarter last year)

- Market Capitalization: $2.16 billion

Martin Roper, the Company’s Chief Executive Officer, said, “Our exceptionally strong shipment performance in the fourth quarter benefited from retailer and distributor inventory levels rebuilding after the shortages of the prior quarter. We are pleased with our current inventory levels and excited by the current scan growth and indications from retailers of increased points of distribution in the coming resets. Collectively, we believe that this should help us deliver high teens branded growth in 2025."

Company Overview

Founded in 2004 followed by a 2021 IPO, The Vita Coco Company (NASDAQ: COCO) offers coconut water products that are a natural way to quench thirst.

Beverages, Alcohol, and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $516 million in revenue over the past 12 months, Vita Coco is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the other hand, it can grow faster because it’s working from a smaller revenue base and has a longer runway of untapped store chains to sell into.

As you can see below, Vita Coco grew its sales at a decent 10.8% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Vita Coco reported year-on-year revenue growth of 19.9%, and its $127.3 million of revenue exceeded Wall Street’s estimates by 4.4%.

Looking ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, similar to its three-year rate. This projection is admirable and indicates the market is baking in success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

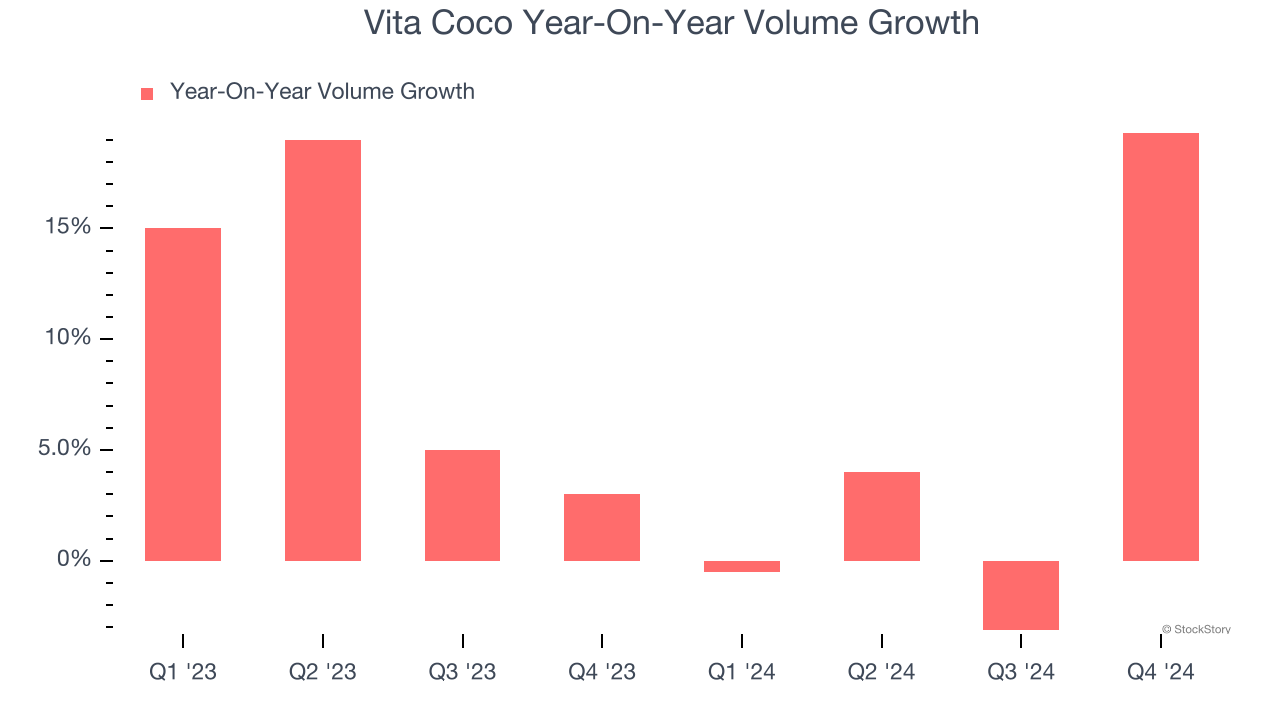

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Vita Coco’s average quarterly volume growth was a robust 7.7% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Vita Coco’s Q4 2024, sales volumes jumped 19.3% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Vita Coco’s Q4 Results

We liked that Vita Coco beat revenue and EBITDA expectations this quarter. On the other hand, its full-year revenue guidance slightly missed and its gross margin fell short of Wall Street’s estimates. Overall, this quarter could have been better. Shares traded down 5.2% to $36.26 immediately after reporting.

Is Vita Coco an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.