Off-price retail company TJX (NYSE: TJX) reported Q4 CY2024 results beating Wall Street’s revenue expectations, but sales were flat year on year at $16.35 billion. On the other hand, next quarter’s revenue guidance of $12.79 billion was less impressive, coming in 2.8% below analysts’ estimates. Its GAAP profit of $1.23 per share was 5.3% above analysts’ consensus estimates.

Is now the time to buy TJX? Find out by accessing our full research report, it’s free.

TJX (TJX) Q4 CY2024 Highlights:

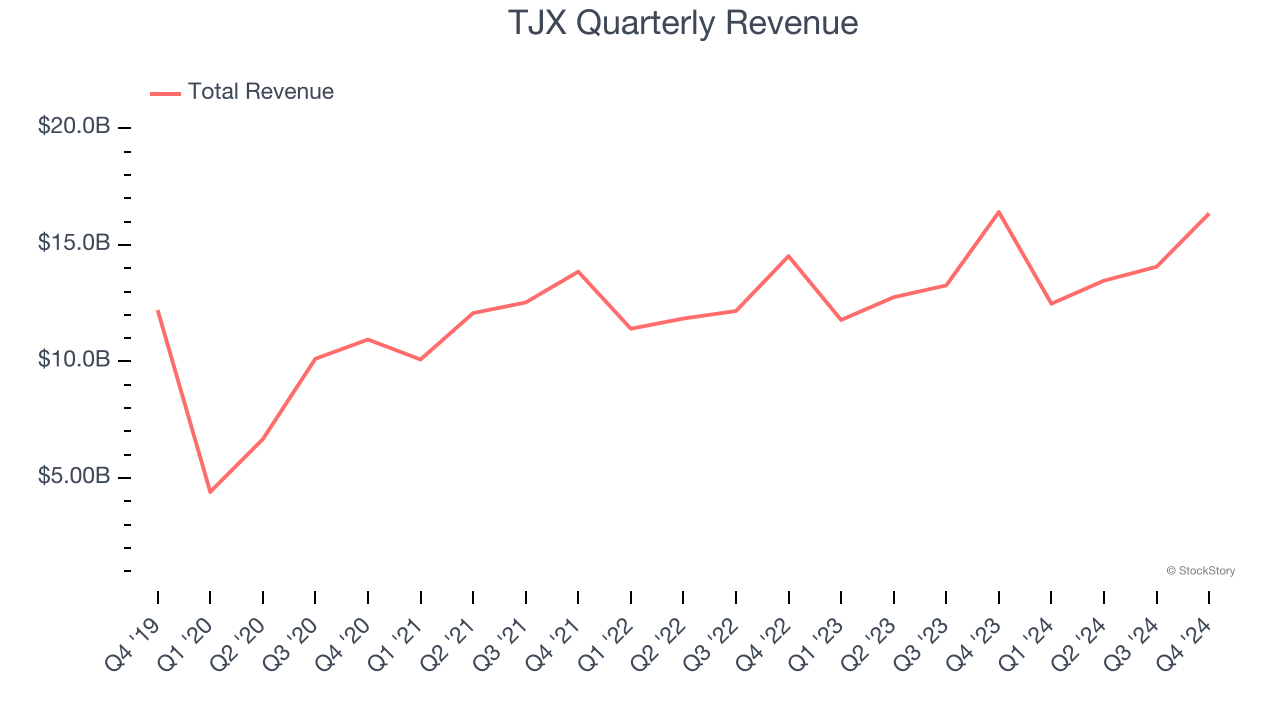

- Revenue: $16.35 billion vs analyst estimates of $16.19 billion (flat year on year, 1% beat)

- EPS (GAAP): $1.23 vs analyst estimates of $1.17 (5.3% beat)

- Adjusted EBITDA: $2.03 billion vs analyst estimates of $2.03 billion (12.4% margin, in line)

- Revenue Guidance for Q1 CY2025 is $12.79 billion at the midpoint, below analyst estimates of $13.16 billion

- EPS (GAAP) guidance for the upcoming financial year 2026 is $4.39 at the midpoint, missing analyst estimates by 4.7%

- Operating Margin: 11.3%, in line with the same quarter last year

- Free Cash Flow Margin: 13.4%, similar to the same quarter last year

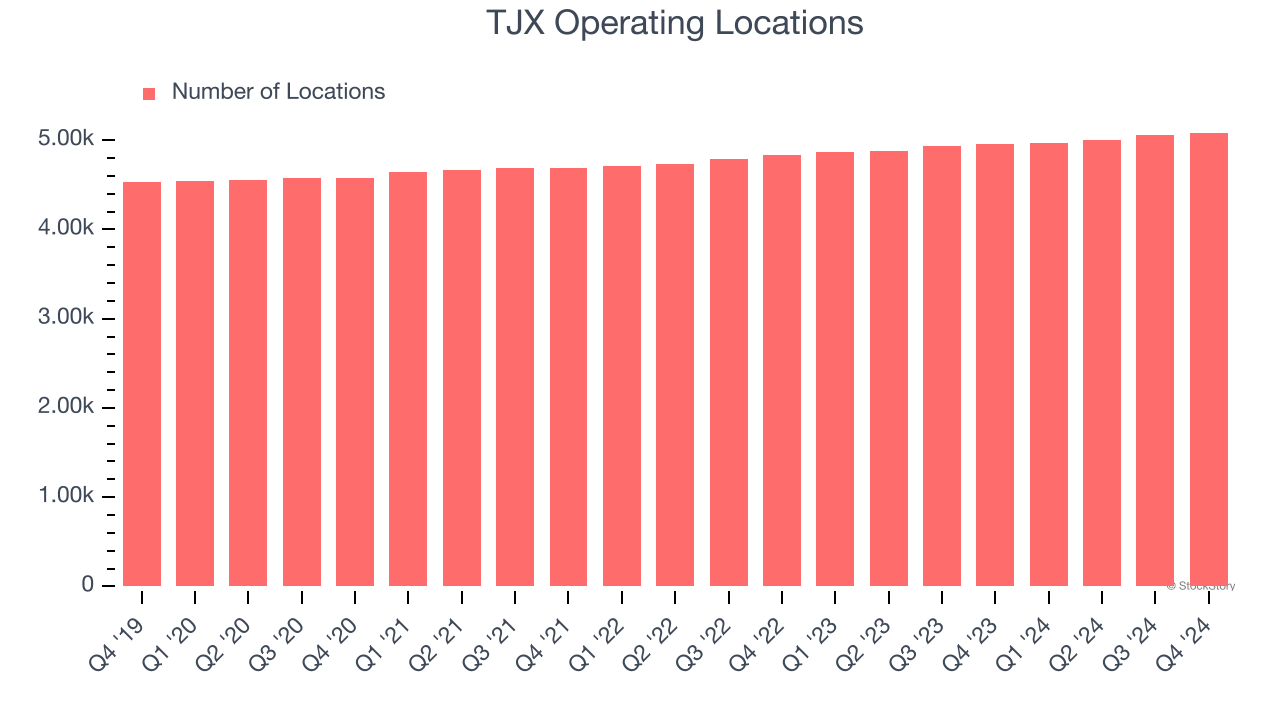

- Locations: 5,085 at quarter end, up from 4,954 in the same quarter last year

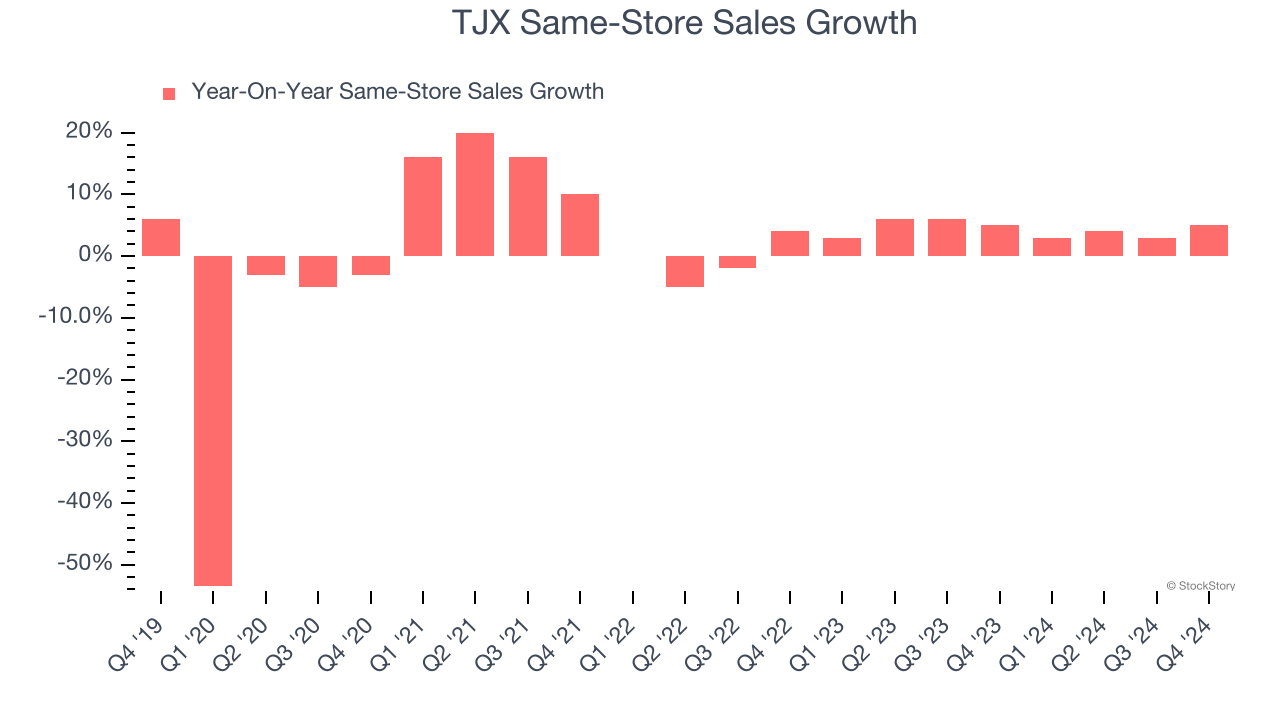

- Same-Store Sales rose 5% year on year, in line with the same quarter last year

- Market Capitalization: $137.9 billion

Ernie Herrman, Chief Executive Officer and President of The TJX Companies, Inc., stated, “I am very proud of the performance of our hard-working Associates in 2024. We delivered outstanding top-and bottom-line results that exceeded our guidance for the year. We surpassed $56 billion in annual sales, drove a 4% comparable store sales increase, significantly increased profitability, and opened our 5,000th store during the year. Further, each of our divisions saw strong, consistent full year comp store sales growth of 4% or above. Our fourth quarter sales, profitability, and earnings per share were all well above our expectations. I am particularly pleased that our overall comp store sales growth of 5% for the quarter was due to strong increases in comp sales and customer transactions at every division. Throughout the year, we offered our wide range of customers compelling values on good, better, and best brands and on-point fashions, and an exciting treasure-hunt shopping experience. As we begin a new year, we are confident that remaining focused on the off-price fundamentals of our great company will continue to serve us well, as it has over many decades, and as always, we will strive to beat our plans. Longer term, we see many opportunities to successfully grow our business and deliver value to even more consumers around the world.”

Company Overview

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

Discount Retailer

Discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, clothes, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $56.36 billion in revenue over the past 12 months, TJX is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it's harder to find incremental growth when you've penetrated most of the market.

As you can see below, TJX’s 6.2% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, TJX’s $16.35 billion of revenue was flat year on year but beat Wall Street’s estimates by 1%. Company management is currently guiding for a 2.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, similar to its five-year rate. This projection is particularly healthy for a company of its scale and implies the market is forecasting success for its products.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Store Performance

Number of Stores

TJX sported 5,085 locations in the latest quarter. Over the last two years, it has opened new stores quickly, averaging 2.7% annual growth. This was faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

TJX’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.4% per year. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives TJX multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, TJX’s same-store sales rose 5% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from TJX’s Q4 Results

We enjoyed seeing TJX beat analysts’ revenue and gross margin expectations this quarter. On the other hand, its EPS guidance for next quarter and the full year both fell short of Wall Street’s estimates. The market seems to be focused on the good quarter and forgiving the soft guidance, and shares traded up 2.7% to $126.10 immediately after reporting.

Big picture, is TJX a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.