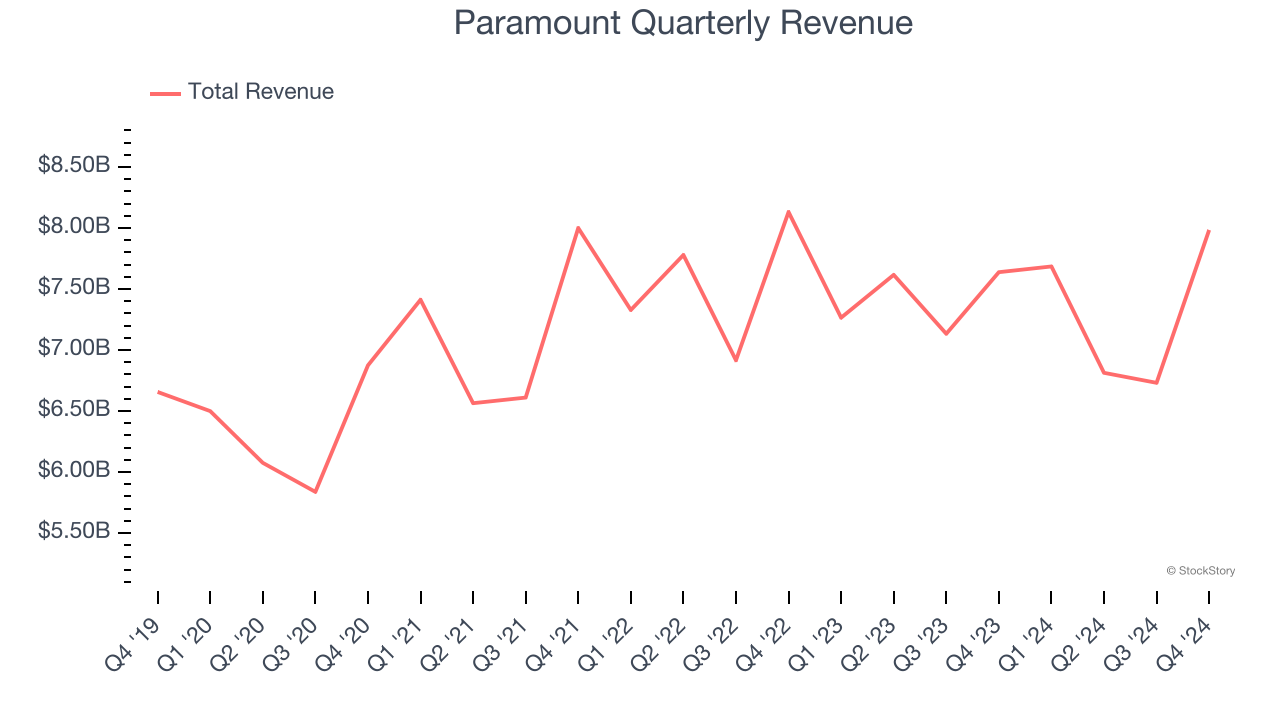

Multinational media and entertainment corporation Paramount (NASDAQ: PARA) fell short of the market’s revenue expectations in Q4 CY2024 as sales rose 4.5% year on year to $7.98 billion. Its non-GAAP loss of $0.11 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Paramount? Find out by accessing our full research report, it’s free.

Paramount (PARA) Q4 CY2024 Highlights:

- Revenue: $7.98 billion vs analyst estimates of $8.14 billion (4.5% year-on-year growth, 1.9% miss)

- Adjusted EPS: -$0.11 vs analyst estimates of $0.13 (significant miss)

- Adjusted EBITDA: $406 million vs analyst estimates of $549.3 million (5.1% margin, 26.1% miss)

- Operating Margin: 1.6%, down from 5.3% in the same quarter last year

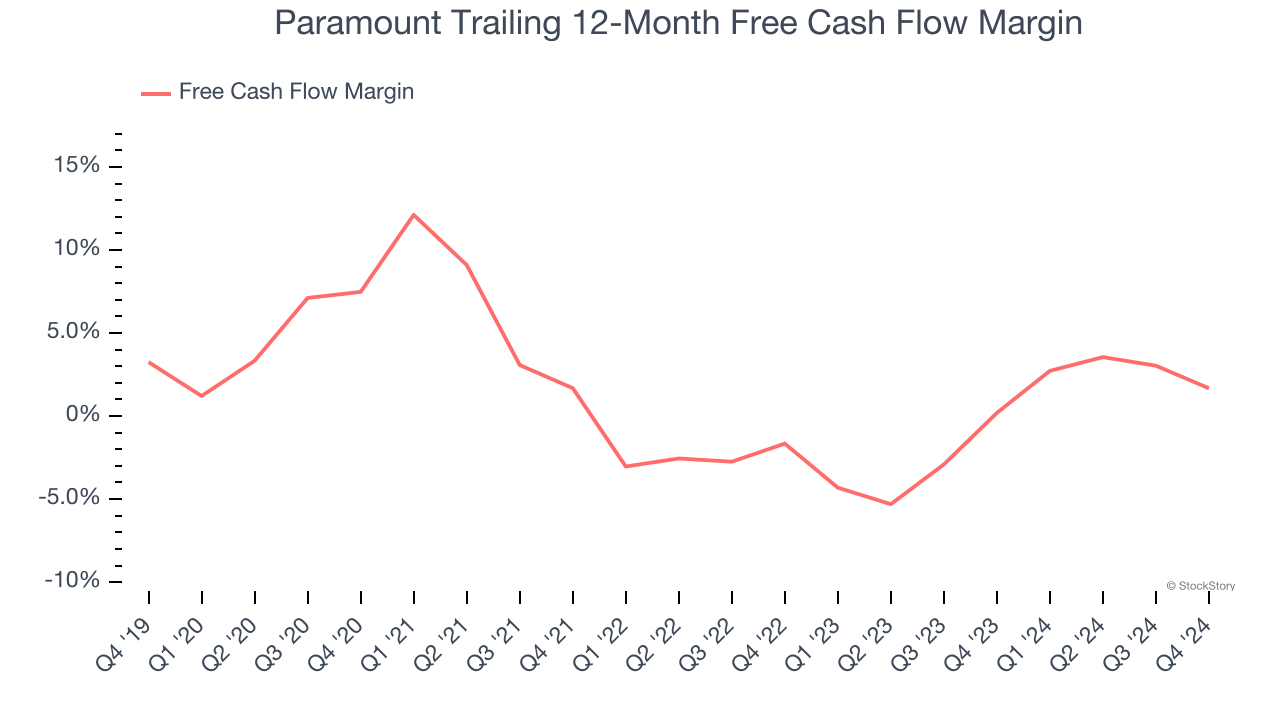

- Free Cash Flow Margin: 0.7%, down from 5.8% in the same quarter last year

- Market Capitalization: $8.13 billion

Company Overview

Owner of Spongebob Squarepants and formerly known as ViacomCBS, Paramount Global (NASDAQ: PARA) is a major media conglomerate offering television, film production, and digital content across various global platforms.

Broadcasting

Broadcasting companies have been facing secular headwinds in the form of consumers abandoning traditional television and radio in favor of streaming services. As a result, many broadcasting companies have evolved by forming distribution agreements with major streaming platforms so they can get in on part of the action, but will these subscription revenues be as high quality and high margin as their legacy revenues? Only time will tell which of these broadcasters will survive the sea changes of technological advancement and fragmenting consumer attention.

Sales Growth

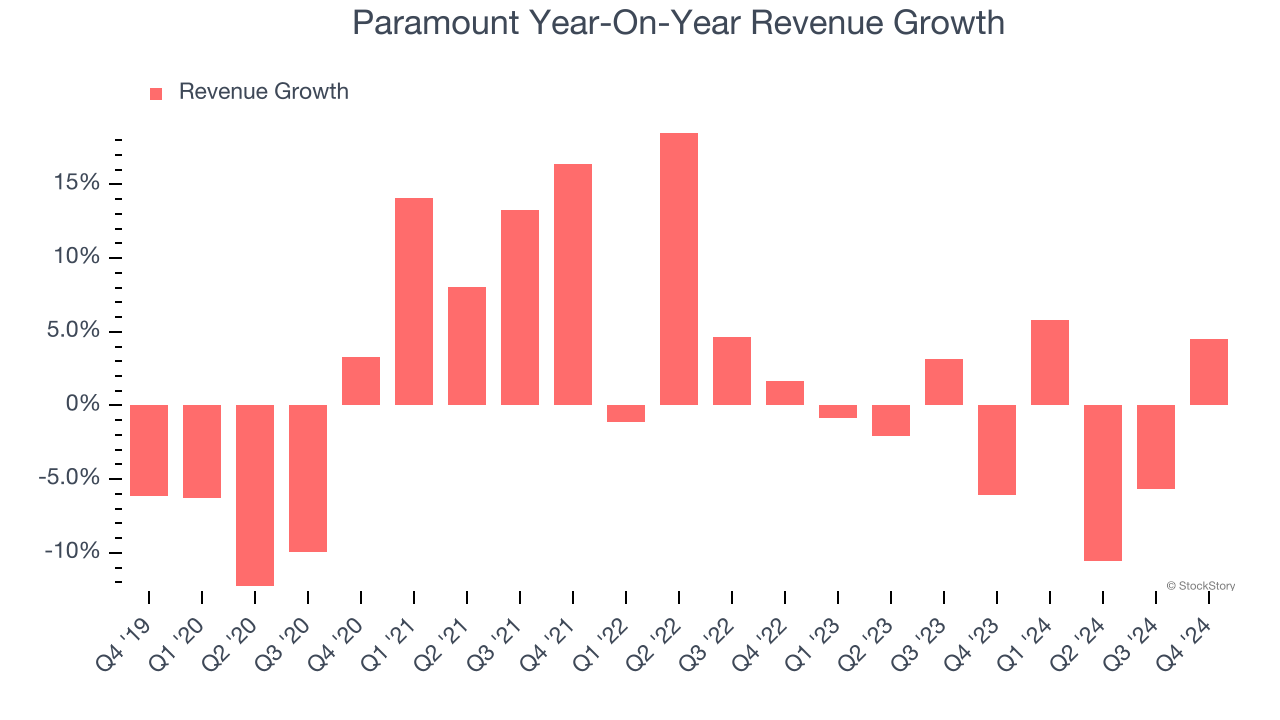

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Paramount grew its sales at a weak 1.6% compounded annual growth rate. This fell short of our benchmarks and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Paramount’s history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.6% annually.

Paramount also breaks out the revenue for its three most important segments: TV Media, Direct-to-Consumer, and Filmed Entertainment, which are 62.4%, 25.2%, and 13.5% of revenue. Over the last two years, Paramount’s Direct-to-Consumer revenue (streaming) averaged 25.6% year-on-year growth while its TV Media (broadcasting) and Filmed Entertainment (movies) revenues averaged 7% and 5.5% declines.

This quarter, Paramount’s revenue grew by 4.5% year on year to $7.98 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Paramount broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Paramount broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 5.1 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting Paramount’s free cash flow margin of 1.7% for the last 12 months to remain the same.

Key Takeaways from Paramount’s Q4 Results

We struggled to find many positives in these results as its revenue, EPS, and EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.5% to $11.07 immediately following the results.

Paramount’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.