Medical technology company Enovis Corporation (NYSE: ENOV) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 23.3% year on year to $561 million. On the other hand, the company’s full-year revenue guidance of $2.21 billion at the midpoint came in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.98 per share was 7% above analysts’ consensus estimates.

Is now the time to buy Enovis? Find out by accessing our full research report, it’s free.

Enovis (ENOV) Q4 CY2024 Highlights:

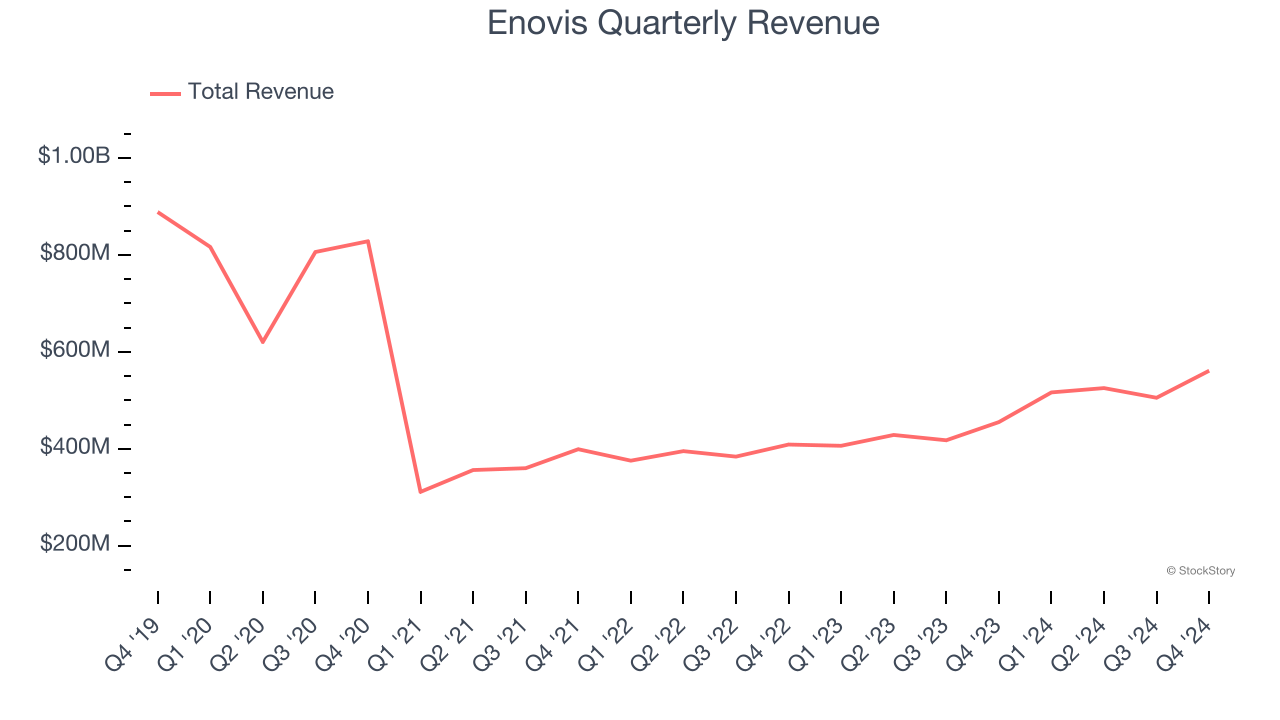

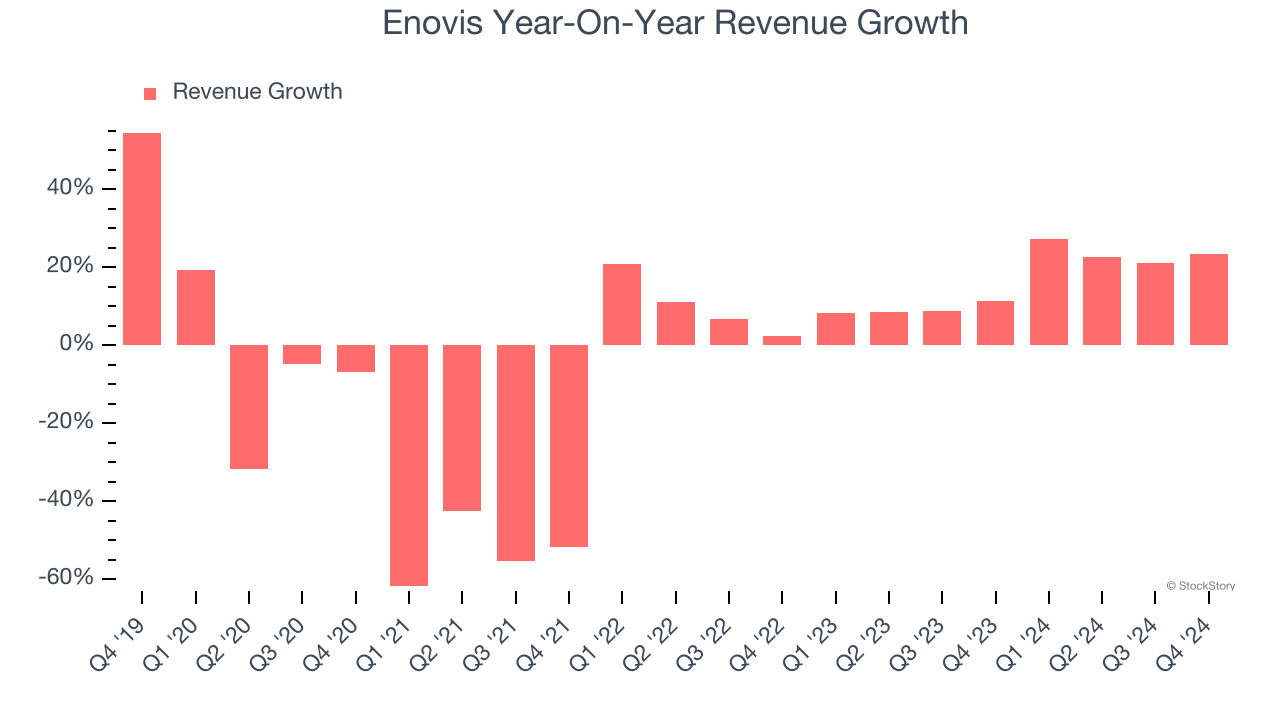

- Revenue: $561 million vs analyst estimates of $555.3 million (23.3% year-on-year growth, 1% beat)

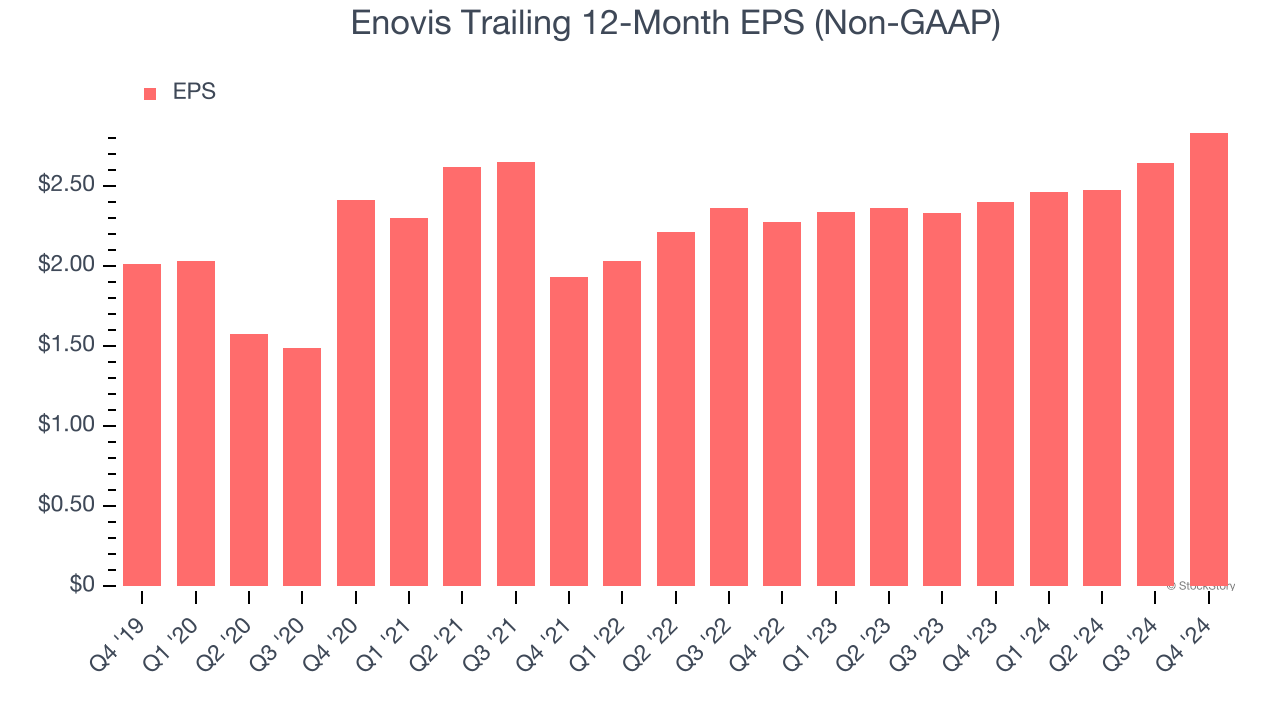

- Adjusted EPS: $0.98 vs analyst estimates of $0.92 (7% beat)

- Adjusted EBITDA: $112.9 million vs analyst estimates of $112.1 million (20.1% margin, 0.7% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $2.21 billion at the midpoint, missing analyst estimates by 0.8% and implying 4.6% growth (vs 23.5% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $3.18 at the midpoint, beating analyst estimates by 0.6%

- EBITDA guidance for the upcoming financial year 2025 is $410 million at the midpoint, below analyst estimates of $418.4 million

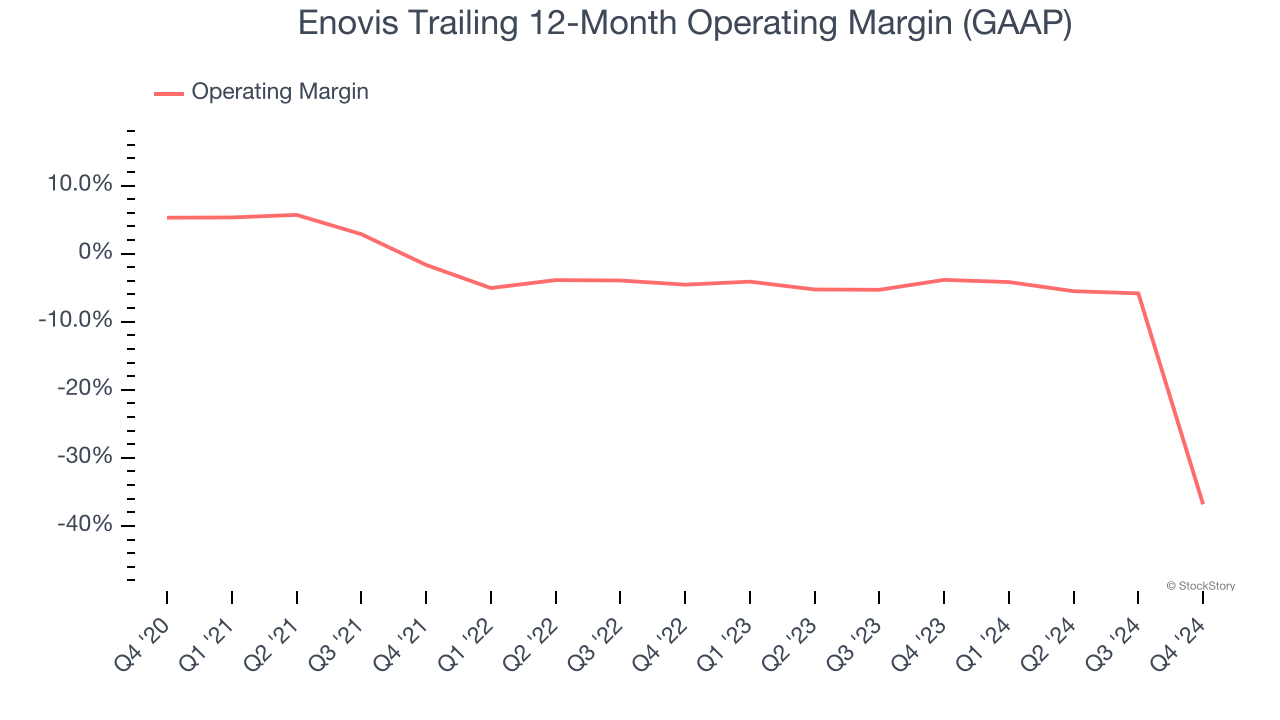

- Operating Margin: -118%, down from -1.3% in the same quarter last year (due to $645 million one-time impairment charge)

- Free Cash Flow Margin: 6.3%, down from 8.9% in the same quarter last year

- Market Capitalization: $2.39 billion

“Our performance in 2024 marks a transformational year for the Company as we executed our integration plans and solidified our ability to deliver sustainable high-single-digit organic growth and year-over-year margin expansion,” said Matt Trerotola, Chief Executive Officer of Enovis.

Company Overview

Originally founded in 1995 as diversified industrial company Colfax Corporation, Enovis Corporation (NYSE: ENOV) focuses on medical technology for orthopedic care, rehabilitation, and surgical products.

Medical Devices & Supplies - Specialty

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Enovis struggled to consistently generate demand over the last five years as its sales dropped at a 8.7% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Enovis’s annualized revenue growth of 16.1% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Enovis reported robust year-on-year revenue growth of 23.3%, and its $561 million of revenue topped Wall Street estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is above the sector average and implies the market sees some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Enovis’s high expenses have contributed to an average operating margin of negative 7.8% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Enovis’s operating margin decreased by 42.1 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 32.3 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Enovis generated a negative 118% operating margin due to $645 million one-time impairment charge.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Enovis’s EPS grew at a solid 7.1% compounded annual growth rate over the last five years, higher than its 8.7% annualized revenue declines. However, we take this with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, Enovis reported EPS at $0.98, up from $0.79 in the same quarter last year. This print beat analysts’ estimates by 7%. Over the next 12 months, Wall Street expects Enovis’s full-year EPS of $2.83 to grow 10.5%.

Key Takeaways from Enovis’s Q4 Results

It was encouraging to see Enovis beat analysts’ revenue and EPS expectations this quarter. On the other hand, its full-year revenue guidance slightly missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter featuring some areas of strength but also some blemishes. The stock traded up 1.4% to $42.69 immediately following the results.

So do we think Enovis is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.