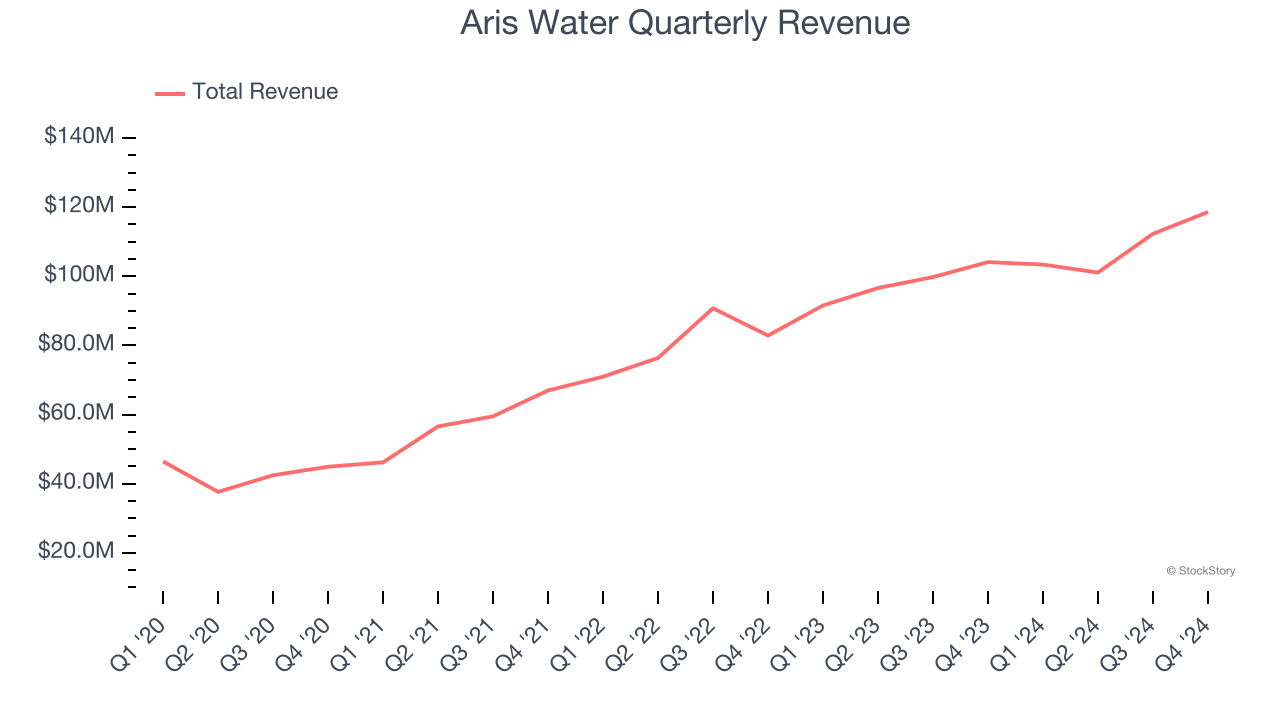

Water handling and recycling company Aris Water (NYSE: ARIS) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 13.9% year on year to $118.6 million. Its non-GAAP profit of $0.29 per share was 18.7% below analysts’ consensus estimates.

Is now the time to buy Aris Water? Find out by accessing our full research report, it’s free.

Aris Water (ARIS) Q4 CY2024 Highlights:

- Revenue: $118.6 million vs analyst estimates of $109.6 million (13.9% year-on-year growth, 8.2% beat)

- Adjusted EPS: $0.29 vs analyst expectations of $0.36 (18.7% miss)

- Adjusted EBITDA: $54.48 million vs analyst estimates of $53.62 million (45.9% margin, 1.6% beat)

- EBITDA guidance for the upcoming financial year 2025 is $225 million at the midpoint, in line with analyst expectations

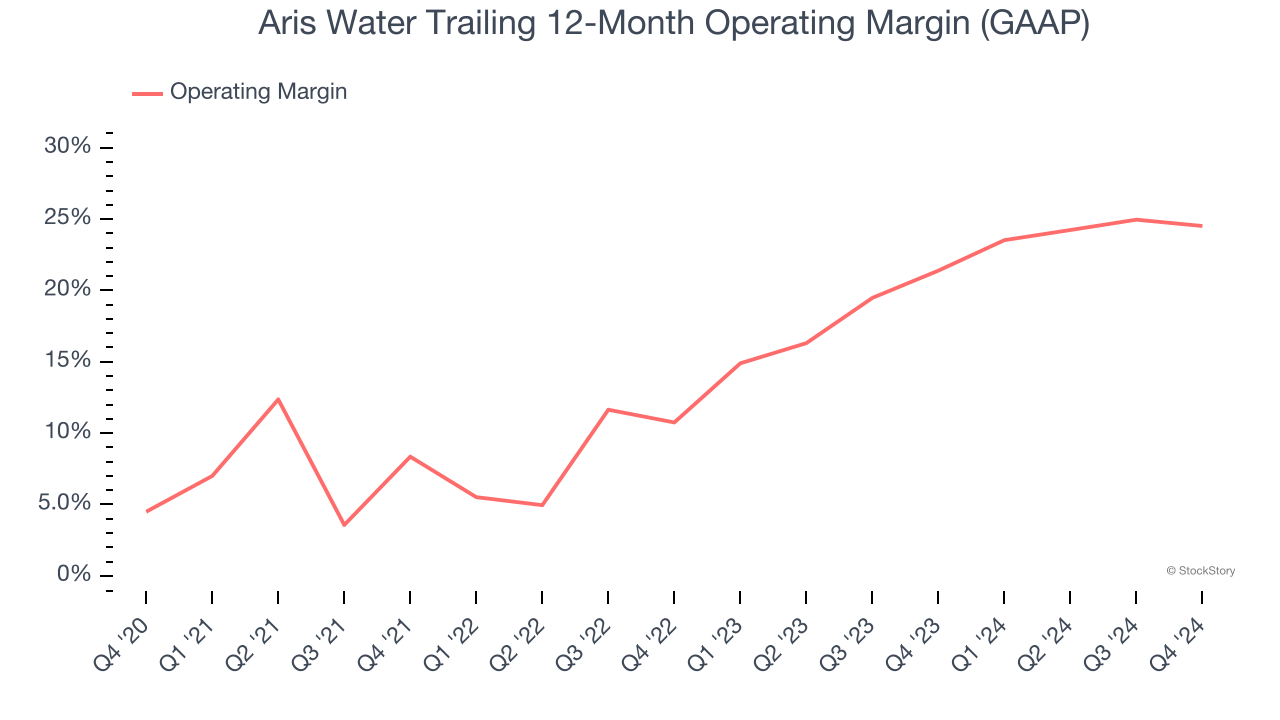

- Operating Margin: 22.5%, down from 24% in the same quarter last year

- Free Cash Flow was $54.87 million, up from -$6.51 million in the same quarter last year

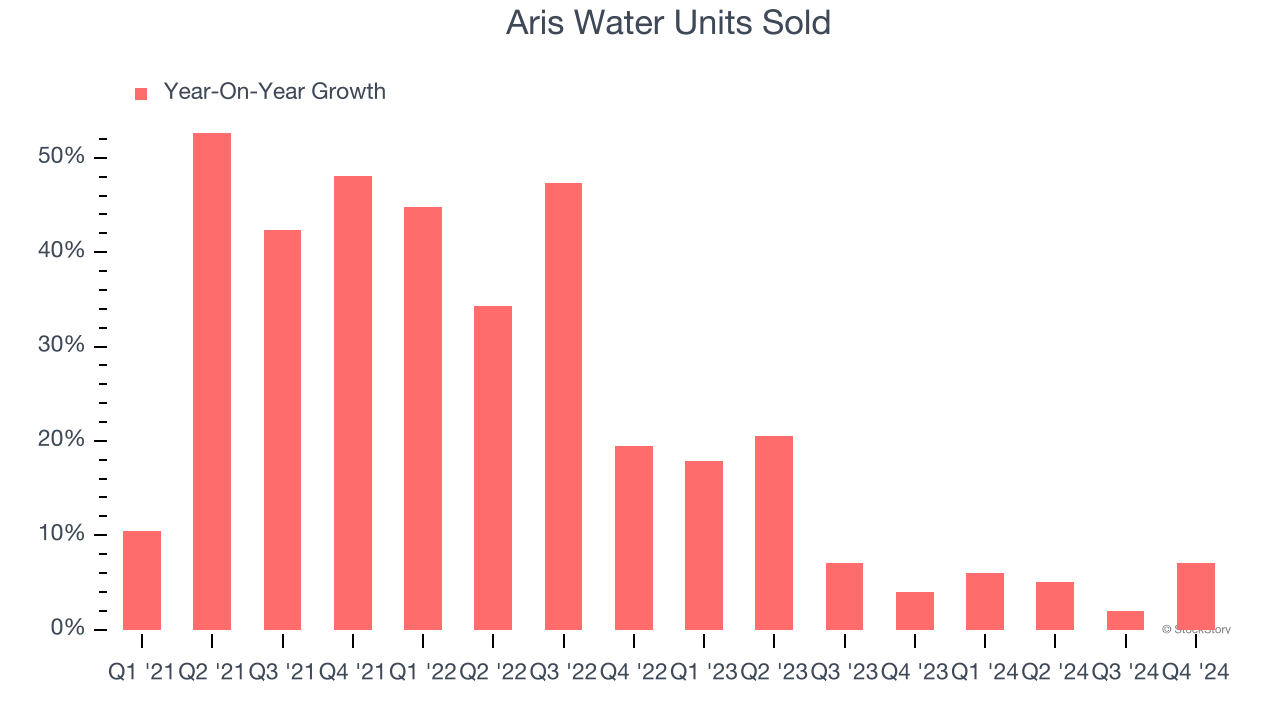

- Sales Volumes rose 7% year on year (4% in the same quarter last year)

- Market Capitalization: $791.9 million

“Aris had a remarkable fourth quarter and a great year in which we successfully grew both volumes and profitability. We achieved Adjusted EBITDA at the top end of our increased guidance and are now delivering on our goal of increasing shareholder returns by raising our dividend to $0.14 per share, representing a 33% increase. We are extremely proud of what our team accomplished in 2024 and believe we will continue our strong performance in our core business. We are also making progress in mineral extraction, beneficial reuse, and the development of technologies for the treatment of wastewater outside the oil and gas industry,” said Amanda Brock, President and CEO of Aris.

Company Overview

Primarily serving the oil and gas industry, Aris Water (NYSE: ARIS) is a provider of water handling and recycling solutions.

Air and Water Services

Many air and water services are statutorily mandated or non-discretionary. This means recurring revenues are often earned through contracts, making for more predictable top-line trends. Additionally, there has been an increasing focus on emissions and water conservation over the last decade, driving innovation in the sector and demand for new services. On the other hand, air and water services companies are at the whim of economic cycles. Interest rates, for example, can greatly impact manufacturing or industrial processes that drive incremental demand for these companies’ offerings.

Sales Growth

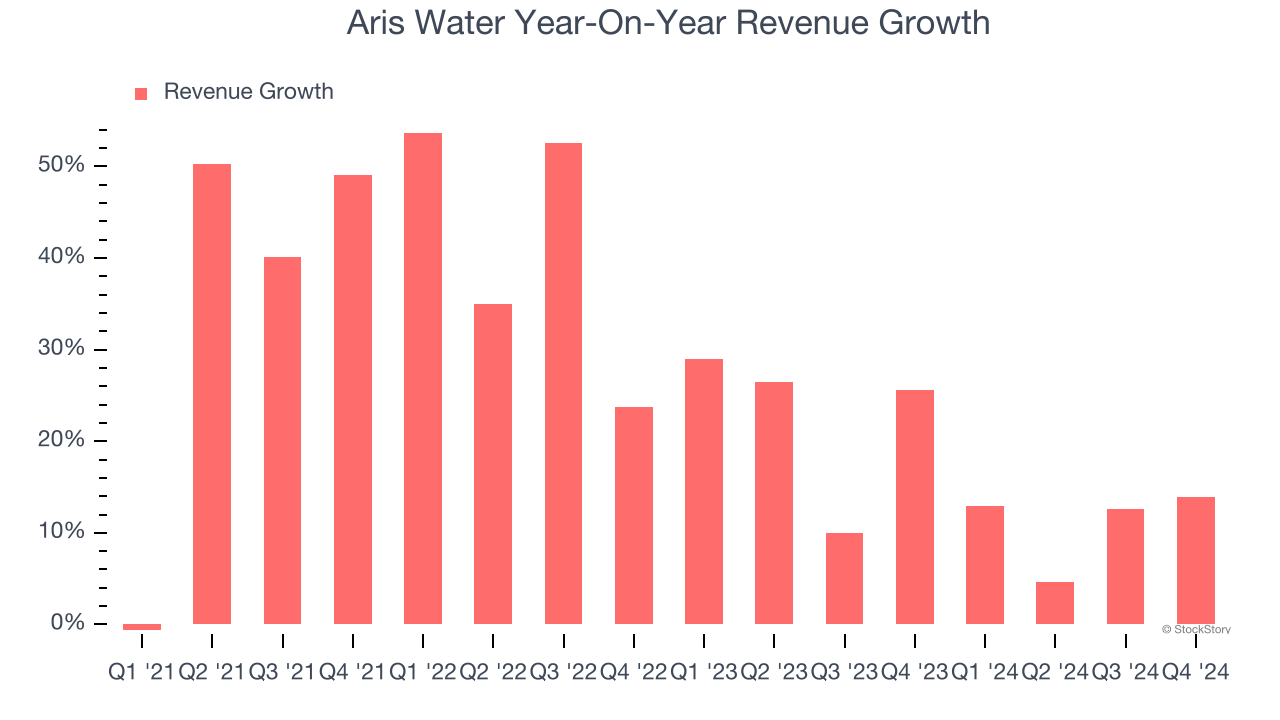

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Aris Water’s sales grew at an incredible 26.2% compounded annual growth rate over the last four years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Aris Water’s annualized revenue growth of 16.5% over the last two years is below its four-year trend, but we still think the results were good and suggest demand was strong.

Aris Water also reports its number of units sold. Over the last two years, Aris Water’s units sold averaged 8.7% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Aris Water reported year-on-year revenue growth of 13.9%, and its $118.6 million of revenue exceeded Wall Street’s estimates by 8.2%.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Aris Water has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Aris Water’s operating margin rose by 20 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Aris Water generated an operating profit margin of 22.5%, down 1.5 percentage points year on year. Since Aris Water’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

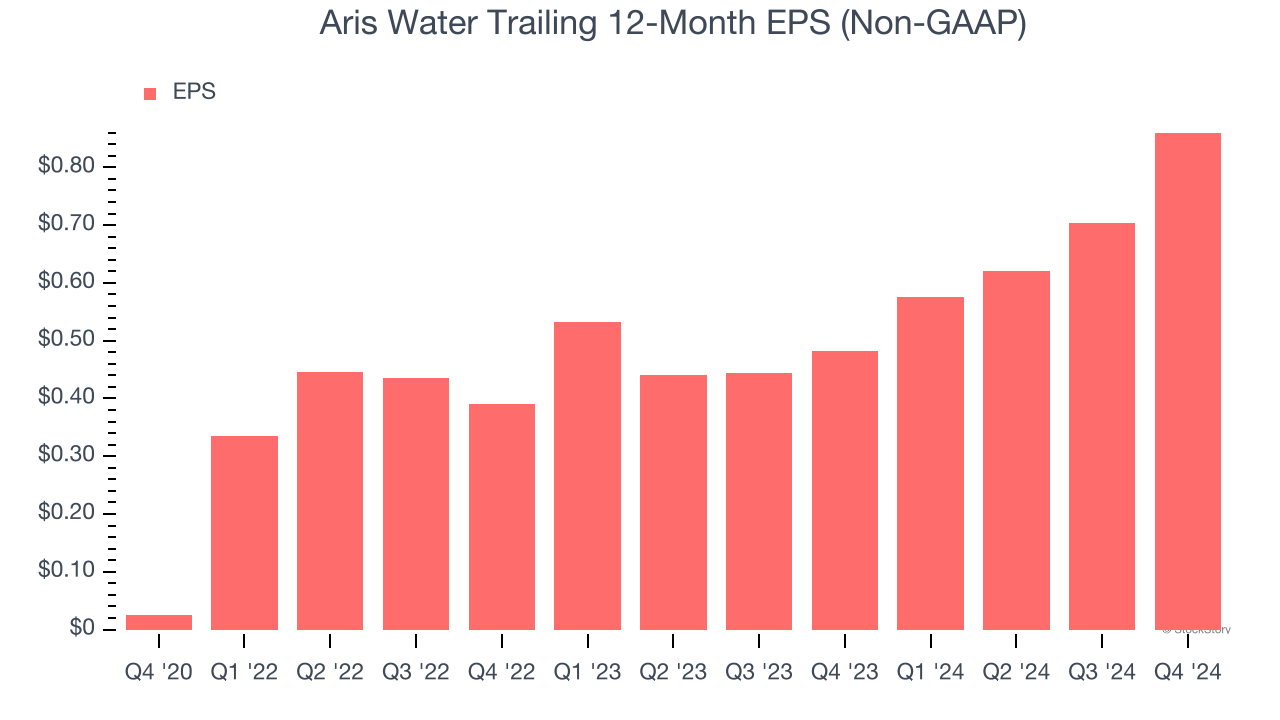

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Aris Water’s EPS grew at an astounding 141% compounded annual growth rate over the last four years, higher than its 26.2% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Aris Water, its two-year annual EPS growth of 48.2% was lower than its four-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Aris Water reported EPS at $0.29, up from $0.13 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Aris Water’s full-year EPS of $0.86 to grow 104%.

Key Takeaways from Aris Water’s Q4 Results

We were impressed by how significantly Aris Water blew past analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS missed significantly and its EBITDA guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.6% to $25.25 immediately after reporting.

Is Aris Water an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.