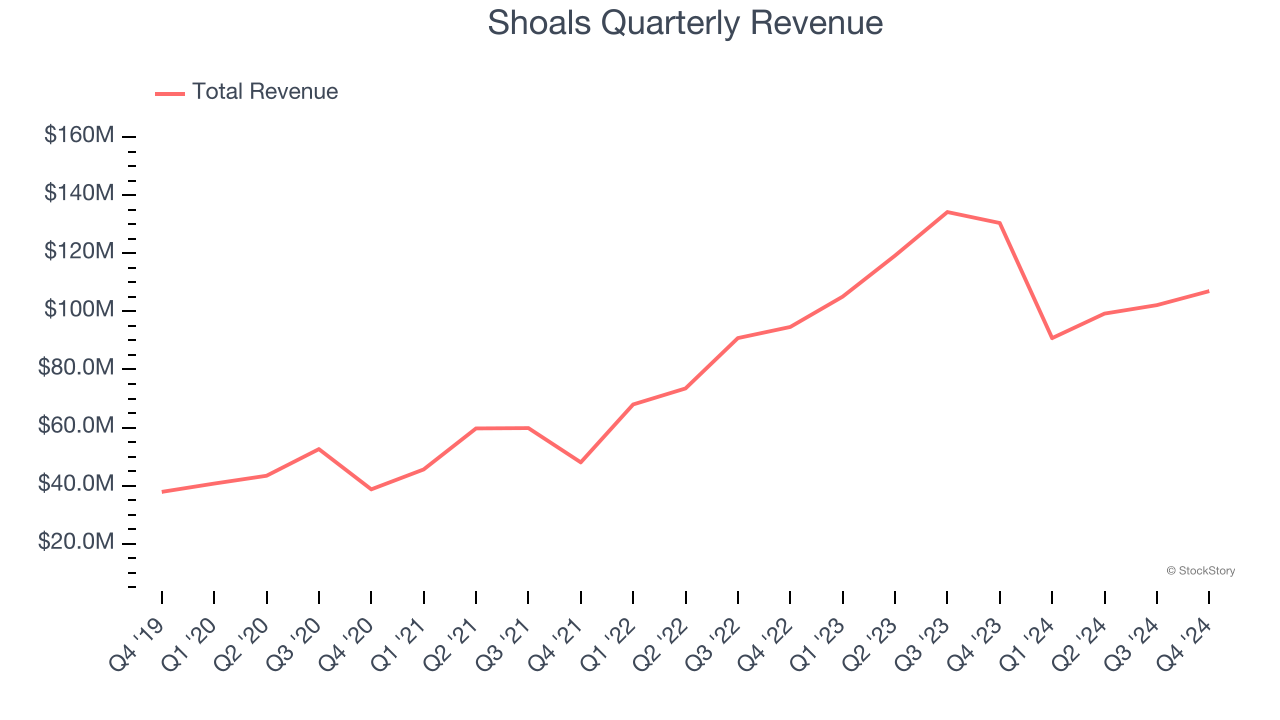

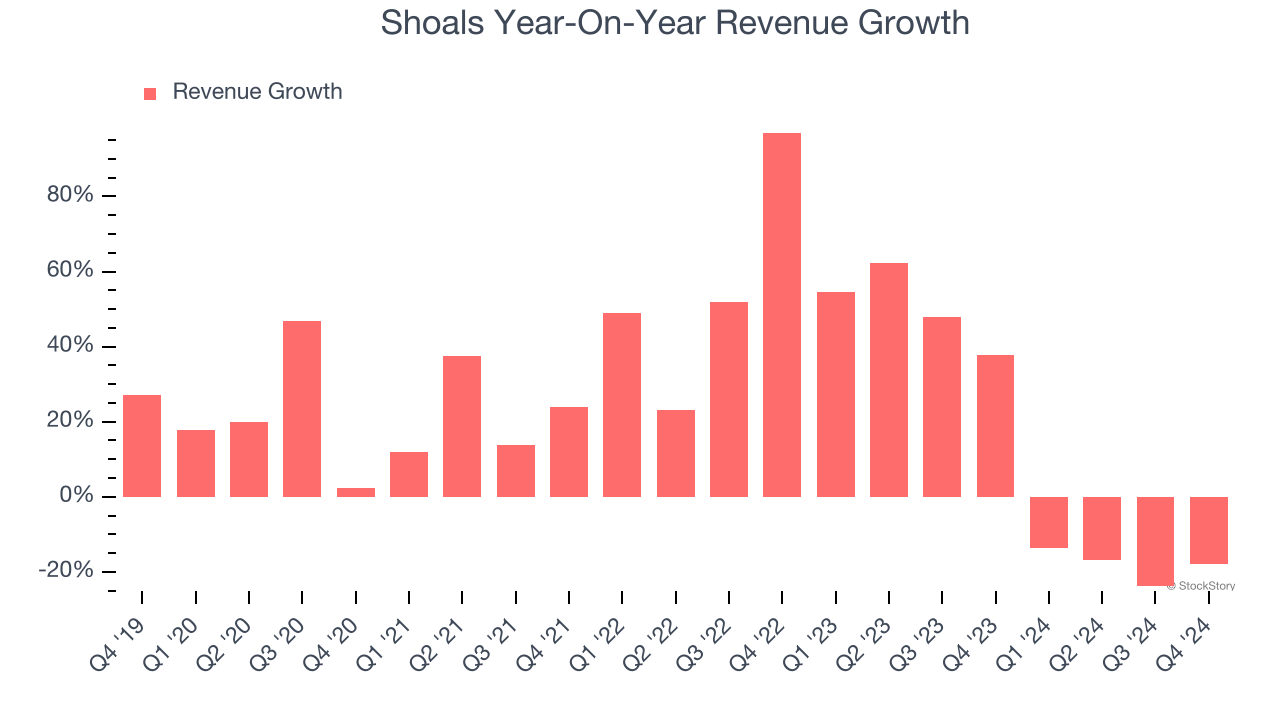

Solar energy systems company Shoals (NASDAQ: SHLS) announced better-than-expected revenue in Q4 CY2024, but sales fell by 18% year on year to $107 million. On the other hand, next quarter’s revenue guidance of $75 million was less impressive, coming in 25% below analysts’ estimates. Its non-GAAP profit of $0.08 per share was 16.7% below analysts’ consensus estimates.

Is now the time to buy Shoals? Find out by accessing our full research report, it’s free.

Shoals (SHLS) Q4 CY2024 Highlights:

- Revenue: $107 million vs analyst estimates of $102 million (18% year-on-year decline, 4.9% beat)

- Adjusted EPS: $0.08 vs analyst expectations of $0.10 (16.7% miss)

- Adjusted EBITDA: $26.41 million vs analyst estimates of $25.22 million (24.7% margin, 4.7% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $430 million at the midpoint, missing analyst estimates by 3% and implying 7.7% growth (vs -18% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $107.5 million at the midpoint, below analyst estimates of $118.6 million

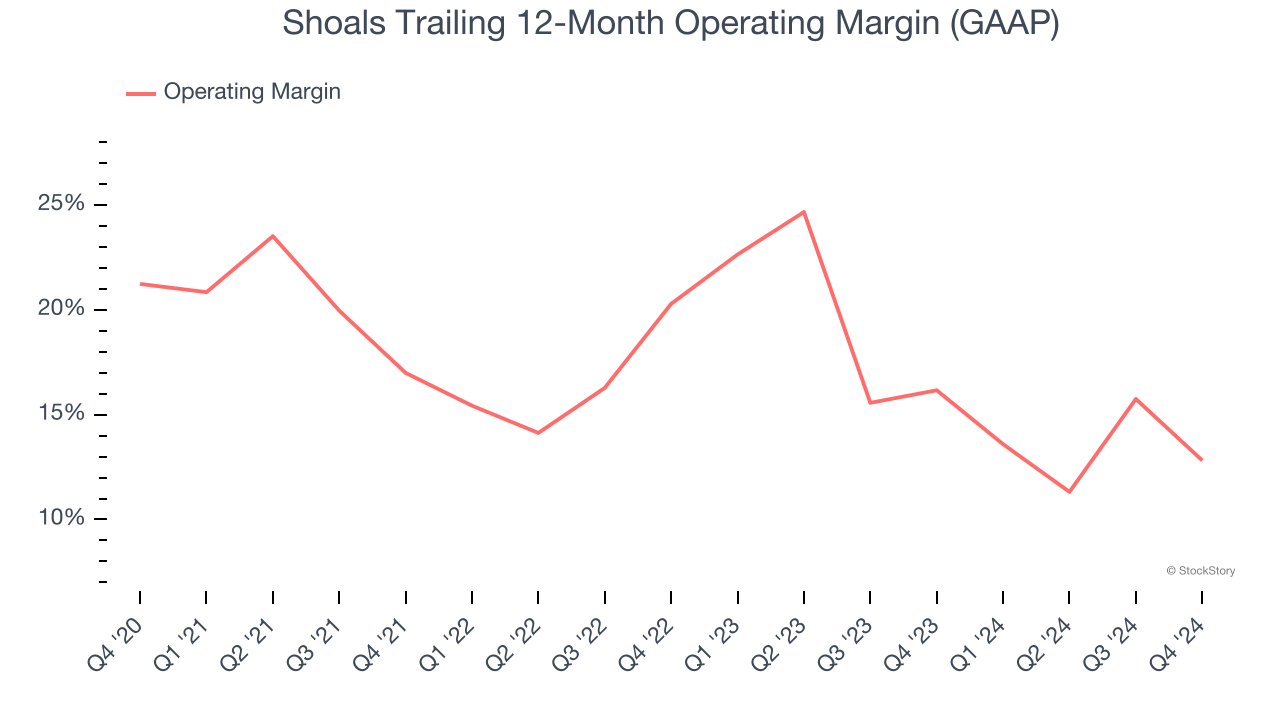

- Operating Margin: 15.4%, down from 24.4% in the same quarter last year

- Free Cash Flow Margin: 11.6%, down from 18% in the same quarter last year

- Backlog: $634.7 million at quarter end, in line with the same quarter last year

- Market Capitalization: $746.8 million

“2024 proved to be an unpredictable year for the US utility scale solar industry. A rapidly shifting political landscape, supply chain and regulatory bottlenecks, and persistently high interest rates, drove unprecedented disruption within our markets. However, 2024 was also a year of exciting operational and commercial process improvements that are beginning to yield results,” said Brandon Moss, CEO of Shoals.

Company Overview

Started in Huntsville, Alabama, Shoals (NASDAQ: SHLS) designs and manufactures products that make solar energy systems work more efficiently.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Shoals’s sales grew at an incredible 22.5% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Shoals’s annualized revenue growth of 10.5% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong. Shoals’s recent history shows it’s one of the better Renewable Energy businesses as many of its peers faced declining sales because of cyclical headwinds.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Shoals’s backlog reached $634.7 million in the latest quarter and was flat over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Shoals was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Shoals’s revenue fell by 18% year on year to $107 million but beat Wall Street’s estimates by 4.9%. Company management is currently guiding for a 17.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.8% over the next 12 months, similar to its two-year rate. This projection is admirable and implies the market sees success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Shoals has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Shoals’s operating margin decreased by 8.4 percentage points over the last five years. This raises an eyebrow about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Shoals generated an operating profit margin of 15.4%, down 9 percentage points year on year. Since Shoals’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

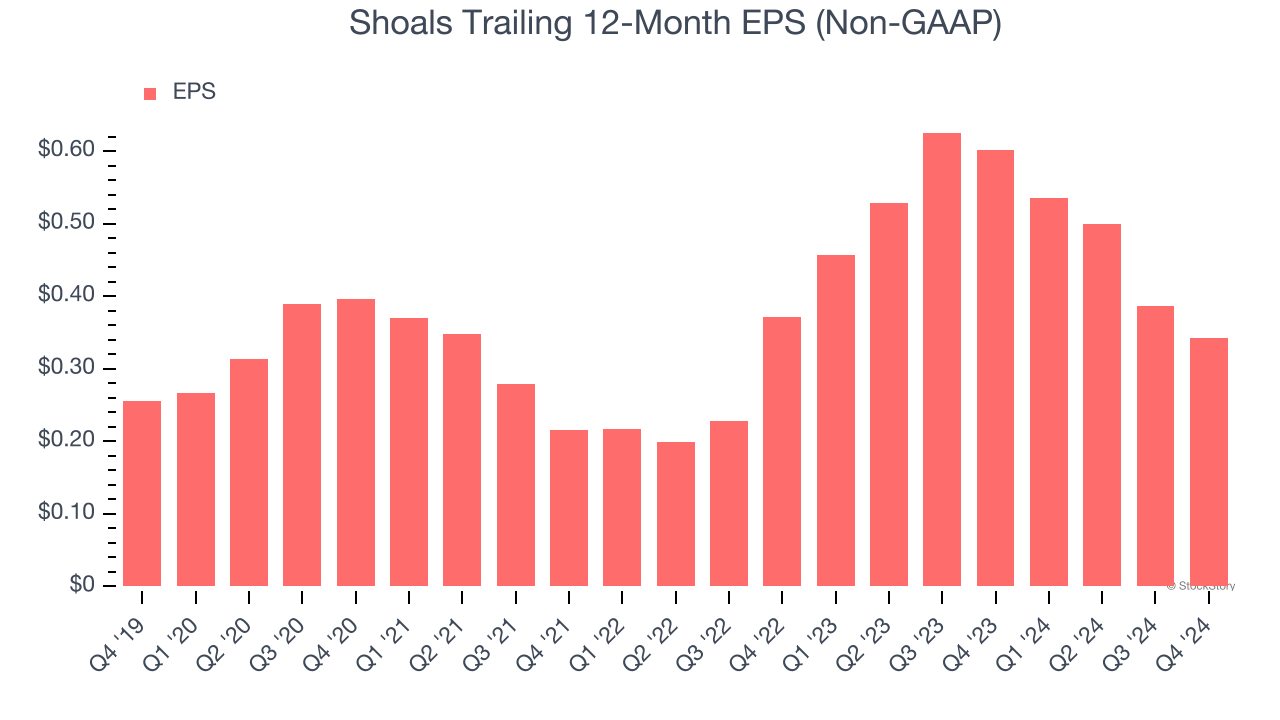

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Shoals’s EPS grew at an unimpressive 6% compounded annual growth rate over the last five years, lower than its 22.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Shoals’s earnings to better understand the drivers of its performance. As we mentioned earlier, Shoals’s operating margin declined by 8.4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Shoals, its two-year annual EPS declines of 4.1% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Shoals reported EPS at $0.08, down from $0.12 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Shoals to perform poorly. Analysts forecast its full-year EPS of $0.34 will hit $0.44.

Key Takeaways from Shoals’s Q4 Results

We were impressed by how significantly Shoals blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed significantly and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.1% to $4.26 immediately following the results.

Shoals’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.