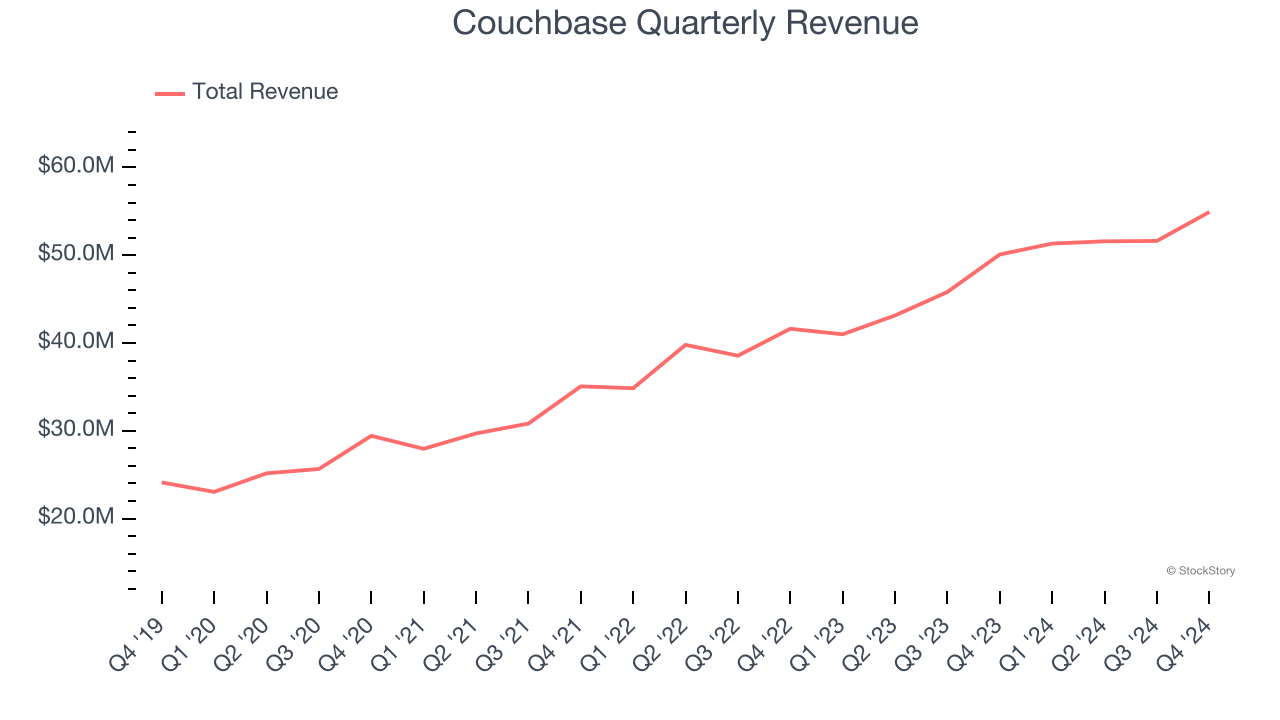

Database as a service company Couchbase (NASDAQ: BASE) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 9.6% year on year to $54.92 million. On the other hand, next quarter’s revenue guidance of $55.5 million was less impressive, coming in 1.9% below analysts’ estimates. Its non-GAAP loss of $0 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Couchbase? Find out by accessing our full research report, it’s free.

Couchbase (BASE) Q4 CY2024 Highlights:

- Revenue: $54.92 million vs analyst estimates of $53.25 million (9.6% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0 vs analyst estimates of -$0.08 (significant beat)

- Adjusted Operating Income: -$144,000 vs analyst estimates of -$5.12 million (-0.3% margin, 97.2% beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $230 million at the midpoint, missing analyst estimates by 2.8% and implying 9.8% growth (vs 16.8% in FY2025)

- Operating Margin: -28.8%, up from -45.1% in the same quarter last year

- Free Cash Flow was $3.98 million, up from -$17.3 million in the previous quarter

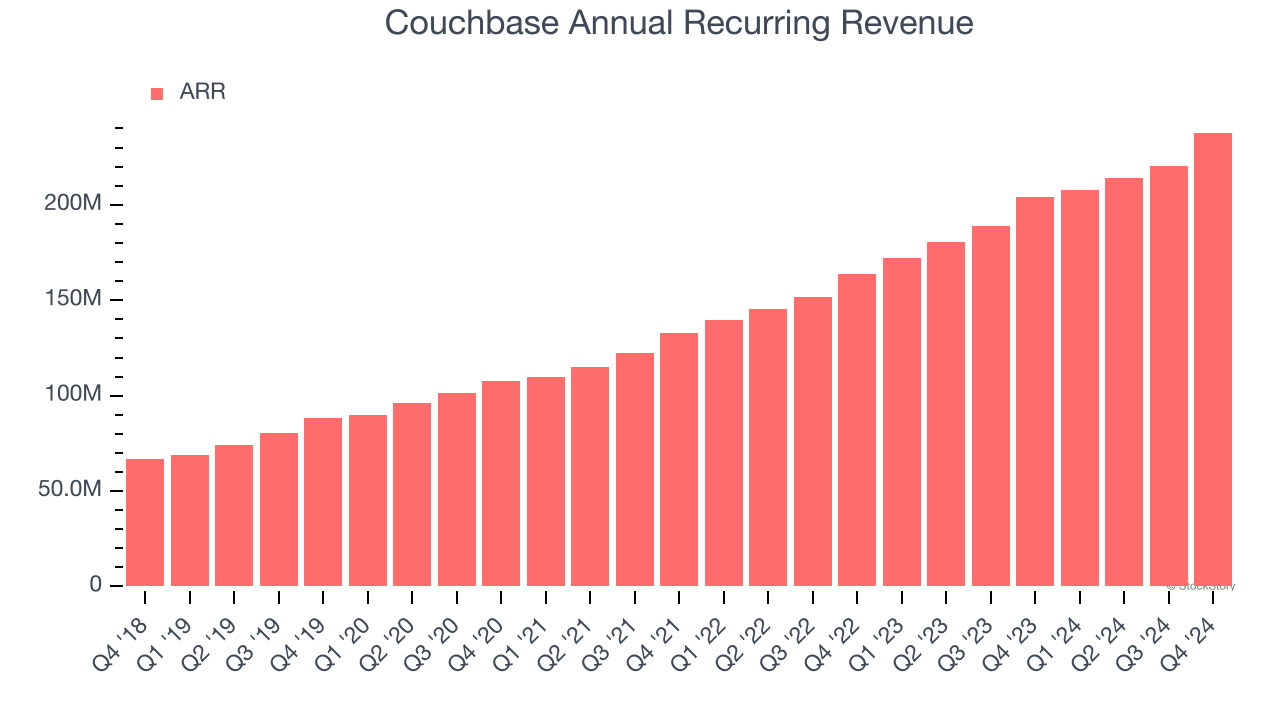

- Annual Recurring Revenue: $237.9 million at quarter end, up 16.5% year on year

- Market Capitalization: $866.4 million

"We finished fiscal 2025 on a strong note, including the highest quarterly free cash flow and net new ARR results in company history," said Matt Cain, Chair, President and CEO of Couchbase.

Company Overview

Formed in 2011 with the merger of Membase and CouchOne, Couchbase (NASDAQ: BASE) is a database-as-a-service platform that allows enterprises to store large volumes of semi-structured data.

Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Couchbase grew its sales at a 19.2% compounded annual growth rate.

This quarter, Couchbase reported year-on-year revenue growth of 9.6%, and its $54.92 million of revenue exceeded Wall Street’s estimates by 3.1%. Company management is currently guiding for a 8.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.2% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is healthy and indicates the market is factoring in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Couchbase’s ARR punched in at $237.9 million in Q4, and over the last four quarters, its growth was impressive as it averaged 18.1% year-on-year increases. This performance aligned with its total sales growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Couchbase a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s very expensive for Couchbase to acquire new customers as its CAC payback period checked in at 952.3 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from Couchbase’s Q4 Results

It was encouraging to see Couchbase beat analysts’ revenue expectations this quarter. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded up 4.6% to $17 immediately after reporting.

Is Couchbase an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.