Recreational vehicle (RV) and boat retailer Camping World (NYSE: CWH) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 8.6% year on year to $1.20 billion. Its non-GAAP loss of $0.47 per share was 13.3% above analysts’ consensus estimates.

Is now the time to buy Camping World? Find out by accessing our full research report, it’s free.

Camping World (CWH) Q4 CY2024 Highlights:

- Revenue: $1.20 billion vs analyst estimates of $1.13 billion (8.6% year-on-year growth, 6.6% beat)

- Adjusted EPS: -$0.47 vs analyst estimates of -$0.54 (13.3% beat)

- Adjusted EBITDA: -$2.49 million vs analyst estimates of -$5.61 million (-0.2% margin, 55.6% beat)

- Operating Margin: -1.3%, in line with the same quarter last year

- Free Cash Flow was -$186 million compared to -$267.9 million in the same quarter last year

- Market Capitalization: $1.25 billion

Marcus Lemonis, Chairman and Chief Executive Officer of CWH stated, “Our combined new and used same store unit sales grew for the second quarter in a row, with increased revenue, increased gross profit and improved adjusted EBITDA, a testament to our unwavering focus on product development, affordability, and used inventory procurement. We see green shoots unfolding across the broader RV landscape, supporting our expectation for more stable industry trends throughout 2025.”

Company Overview

Founded in 1966 as a single recreational vehicle (RV) dealership, Camping World (NYSE: CWH) still sells RVs along with boats and general merchandise for outdoor activities.

Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $6.1 billion in revenue over the past 12 months, Camping World is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Camping World’s 4.5% annualized revenue growth over the last five years (we compare to 2019 to normalize for COVID-19 impacts) was sluggish.

This quarter, Camping World reported year-on-year revenue growth of 8.6%, and its $1.20 billion of revenue exceeded Wall Street’s estimates by 6.6%.

Looking ahead, sell-side analysts expect revenue to grow 6.3% over the next 12 months, an acceleration versus the last five years. This projection is healthy and indicates its newer products will spur better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Store Performance

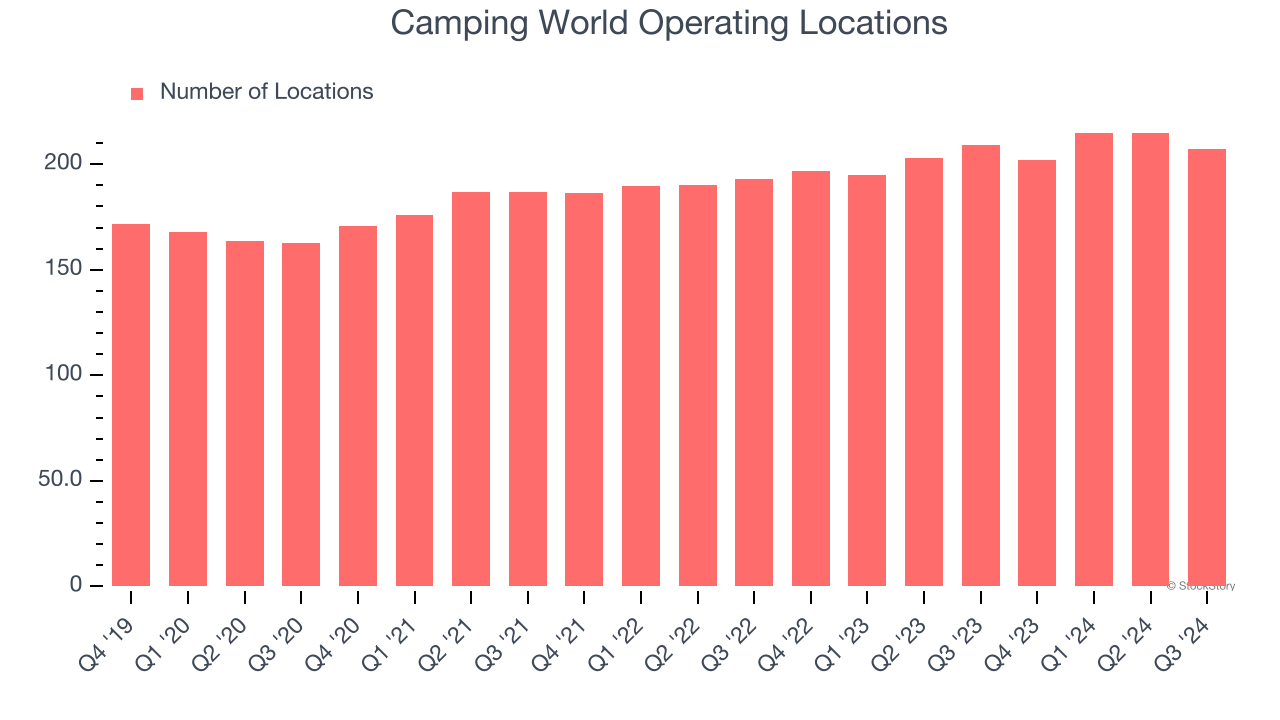

Number of Stores

Camping World opened new stores at a rapid clip over the last two years, averaging 5.1% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Camping World reports its store count intermittently, so some data points are missing in the chart below.

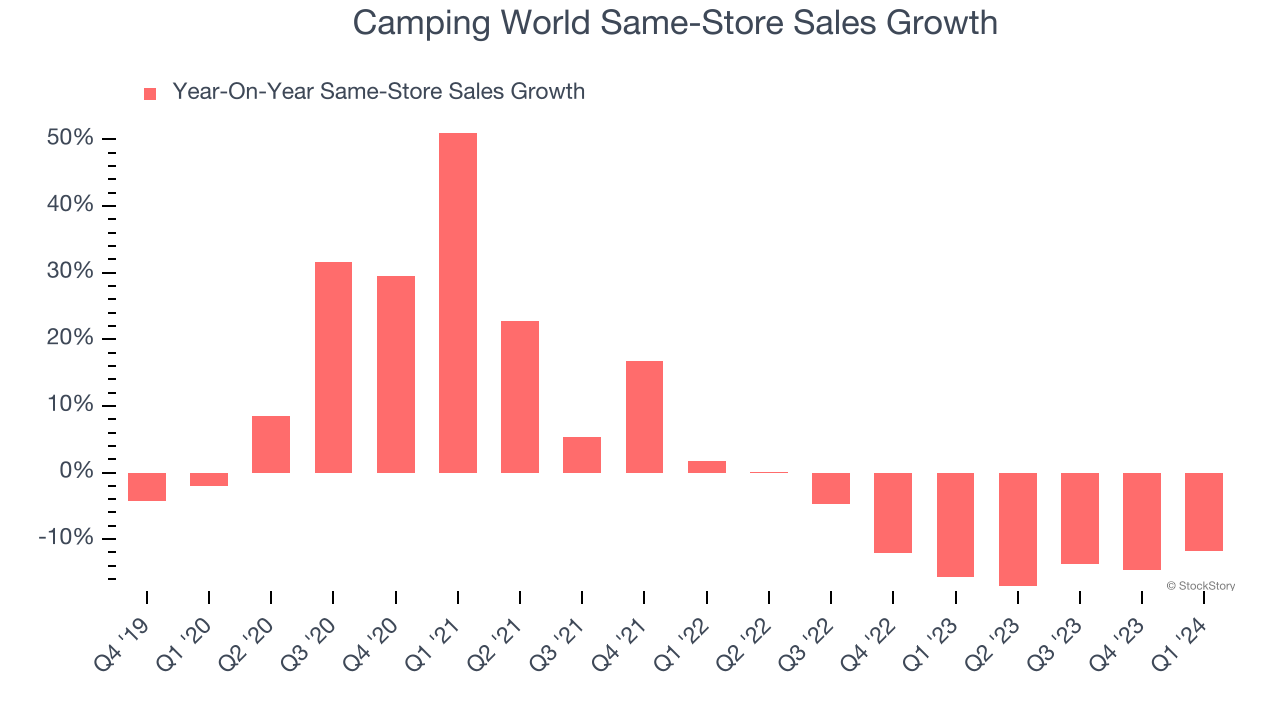

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Camping World’s demand has been shrinking over the last two years as its same-store sales have averaged 14.6% annual declines. This performance is concerning - it shows Camping World artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

Note that Camping World reports its same-store sales intermittently, so some data points are missing in the chart below.

Key Takeaways from Camping World’s Q4 Results

We were impressed by how significantly Camping World blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue and EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 3.5% to $21.50 immediately after reporting.

Camping World may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.