Harley-Davidson currently trades at $33.90 per share and has shown little upside over the past six months, posting a small loss of 2.5%. The stock also fell short of the S&P 500’s 13% gain during that period.

Is now the time to buy Harley-Davidson, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We're swiping left on Harley-Davidson for now. Here are three reasons why you should be careful with HOG and a stock we'd rather own.

Why Do We Think Harley-Davidson Will Underperform?

Founded in 1903, Harley-Davidson (NYSE: HOG) is an American motorcycle manufacturer known for its heavyweight motorcycles designed for cruising on highways.

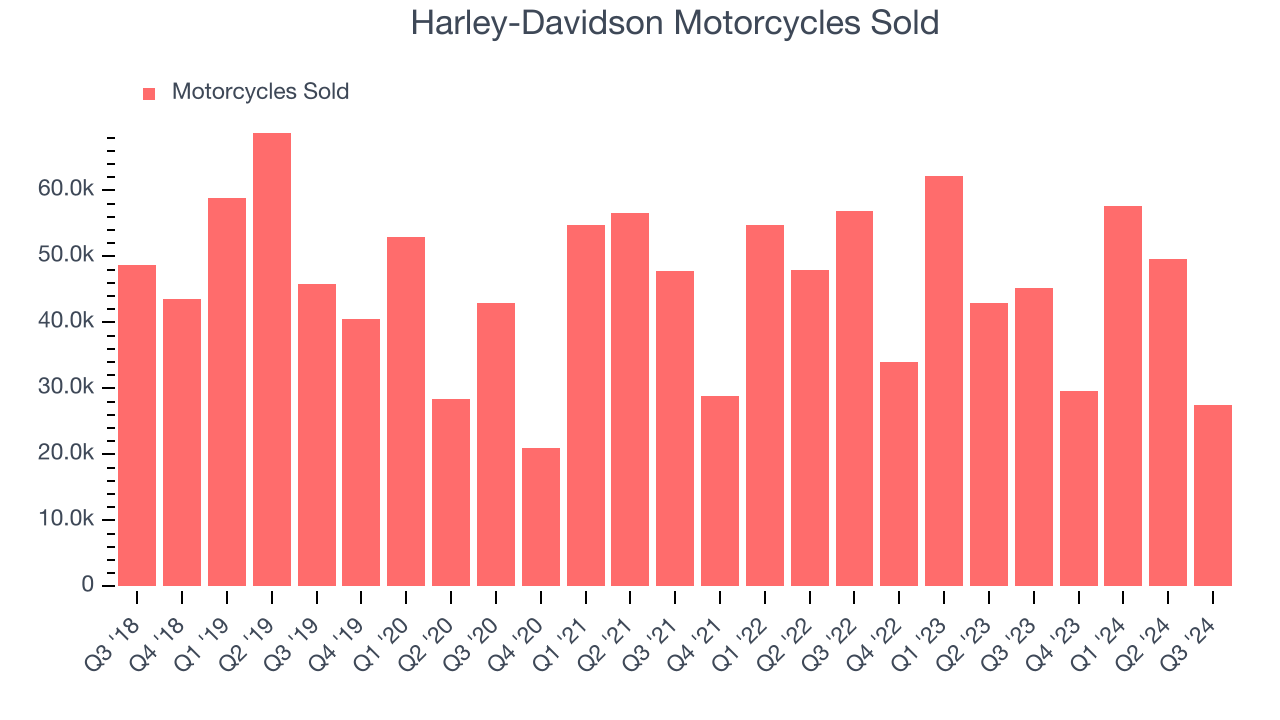

1. Decline in Motorcycles Sold Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Harley-Davidson, our preferred volume metric is motorcycles sold). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Harley-Davidson’s motorcycles sold came in at 27,520 in the latest quarter, and over the last two years, averaged 5.4% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Harley-Davidson might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Harley-Davidson’s revenue to drop by 19.8%, a decrease from its flat sales for the past two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

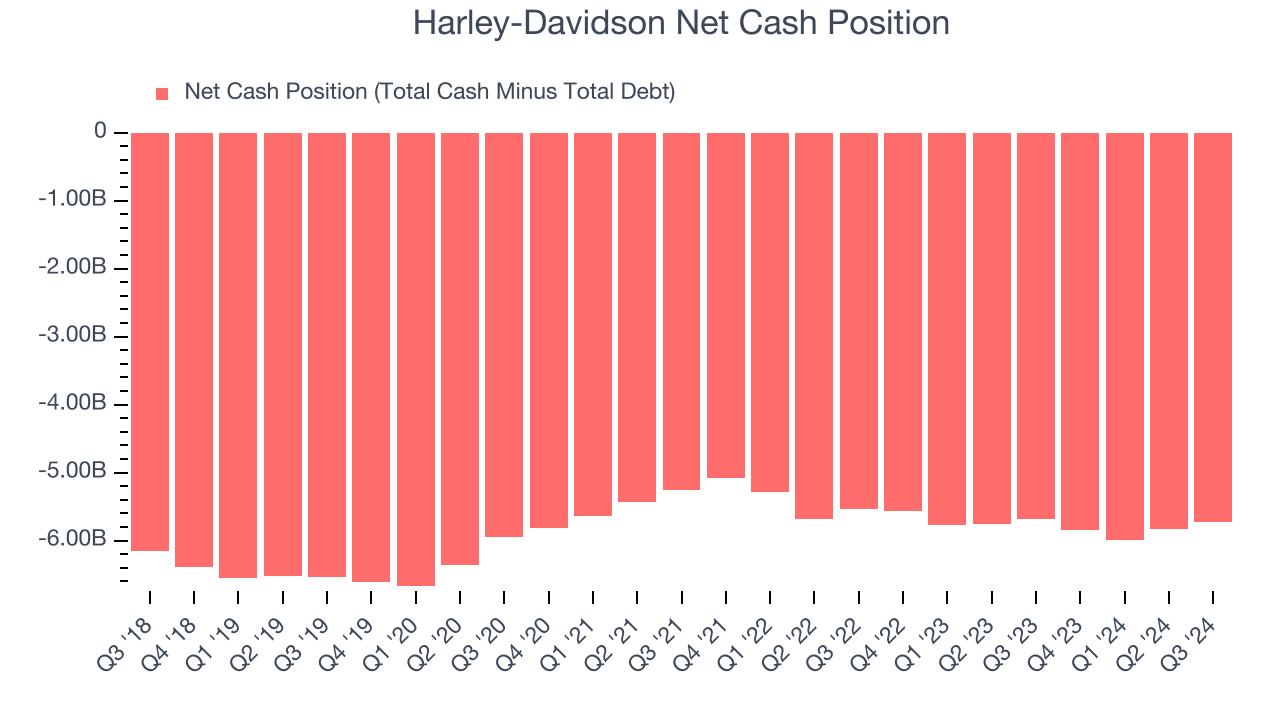

3. High Debt Levels Increase Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Harley-Davidson’s $7.98 billion of debt exceeds the $2.24 billion of cash on its balance sheet. Furthermore, its 8x net-debt-to-EBITDA ratio (based on its EBITDA of $708.6 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Harley-Davidson could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Harley-Davidson can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Harley-Davidson falls short of our quality standards. With its shares lagging the market recently, the stock trades at 7.8x forward price-to-earnings (or $33.90 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. Let us point you toward Microsoft, the most dominant software business in the world.

Stocks We Would Buy Instead of Harley-Davidson

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.