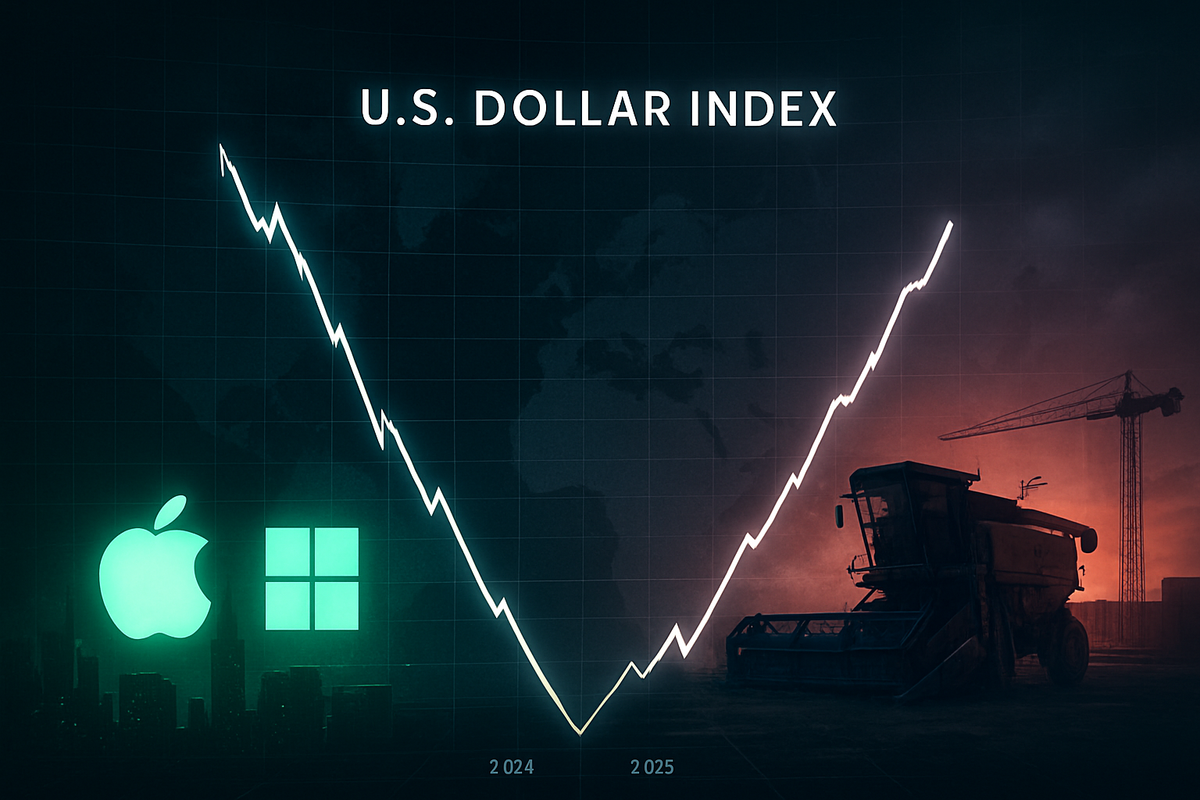

The U.S. financial landscape is currently grappling with a "V-shaped" whipsaw in the value of the U.S. Dollar Index (DXY), a move that has caught both Wall Street analysts and corporate treasurers off guard. After plunging to a four-year low of 95.5 on January 30, 2026, the greenback has staged a ferocious mid-February rebound, climbing back toward 98.0 in less than three weeks. This extreme volatility is sending shockwaves through the balance sheets of multinational corporations and further complicating an already fragile environment for American exporters.

The immediate implications are a double-edged sword: while the brief January dip provided a much-needed accounting "tailwind" for tech giants and consumer staples firms with heavy overseas exposure, the subsequent rebound has reignited fears of a "strong dollar" drag. For the broader market, this volatility is more than just a currency play; it reflects a deep-seated uncertainty regarding Federal Reserve policy, new trade tariffs, and the resilience of the U.S. economy in the face of shifting global alliances.

The January Flash Crash and the February Reversal

The timeline of this currency roller coaster began in late 2025, when a shift in Federal Reserve policy saw interest rates cut to the 3.25%–3.50% range to forestall a cooling labor market. This narrowing of interest rate differentials between the U.S. and its major trading partners triggered a massive capital outflow, culminating in a 10.7% slide for the DXY over the second half of 2025. By late January 2026, the index officially breached the key 97.0 support level, hitting its lowest point since early 2022. This "January Dip" was accelerated by policy uncertainty surrounding the administration's "Liberation Day" tariffs, which initially led markets to fear a period of global economic isolation.

However, the tide turned abruptly in the first two weeks of February. The rebound was catalyzed by several high-impact events: hawkish meeting minutes from the Federal Reserve suggesting that inflation remains "sticky" at 2.8%, and a forceful statement from the Treasury Department affirming a commitment to a "strong dollar" policy. By February 15, the DXY had erased nearly half of its January losses. Market participants, including major desks at Citi and Morgan Stanley, have described the move as a "regime shift," where currency values are no longer just reflecting interest rates but are acting as a real-time barometer for trade-war brinkmanship.

The initial reaction from industry was one of guarded optimism followed by swift defensive positioning. While the ISM Manufacturing PMI rose to 52.6 in January—its first expansionary reading in a year—the data revealed that this growth was largely driven by domestic restocking and "tariff hedging" rather than a true revival in export demand. As the dollar strengthened again in February, corporate hedging strategies were put to the test, with many firms rushing to lock in exchange rates before the greenback could climb further.

Winners and Losers: A Tale of Two Sectors

The volatility has created a stark divide between "currency winners"—primarily large-cap tech and consumer staples—and "currency losers," which include the capital-intensive agricultural and industrial sectors. Microsoft (NASDAQ: MSFT) emerged as a notable beneficiary of the January weakness. In its Q2 FY2026 report, the software giant noted that the softening dollar provided a 2% tailwind to its headline revenue of $81.3 billion, allowing it to beat analyst expectations even as domestic enterprise spending showed signs of cooling. Similarly, Apple (NASDAQ: AAPL) reported record holiday-quarter revenue of $143.7 billion, citing "favorable currency exchange rates" in Europe and Greater China as a primary driver of its 38% growth in those regions.

On the other side of the ledger, the industrial and agricultural sectors are reeling. Caterpillar (NYSE: CAT) posted record quarterly revenue of $19.1 billion in January, but management warned that the favorable 1% currency impact seen in late 2025 is already being eclipsed by the rising cost of imported components and the renewed strength of the dollar in February. Even more distressed is the agricultural giant Archer-Daniels-Midland (NYSE: ADM), which recently reported its weakest Q4 adjusted profit since 2019. ADM’s Ag Services and Oilseeds segment saw a staggering 31% decline in operating profit, as the yo-yoing dollar made U.S. soybeans less competitive against cheaper supplies from Brazil and Argentina.

Farm equipment leader Deere & Co (NYSE: DE) also highlighted the precarious nature of the current market. Despite an earnings beat in early February, the company warned of $1.2 billion in annual tariff-related costs. For Deere, a strong dollar is a double-whammy: it makes their high-tech tractors more expensive for foreign buyers while the underlying commodities those farmers sell are priced in a currency that is becoming increasingly volatile.

Wider Significance and Historical Precedents

The current volatility fits into a broader trend of "de-dollarization" and the weaponization of trade policy. The 10% universal import tariff introduced in 2025 has effectively raised the "real" cost of the dollar for trading partners, leading to a fragmented global market. Historically, this level of volatility—a 4-year low followed by a sharp V-shaped recovery—is reminiscent of the mid-1980s following the Plaza Accord, though the drivers today are fiscal spending and trade barriers rather than coordinated central bank intervention.

The ripple effects are extending to the U.S. government’s own policy toolkit. The "One Big Beautiful Bill Act," which fueled massive fiscal spending in 2025, has created a situation where the Fed must balance supporting growth against the inflationary pressures of a devalued currency. Furthermore, the $12 billion "Farmer Bridge Assistance" (FBA) program serves as an admission that currency and trade volatility have pushed the American agricultural sector to a breaking point, with some industry groups reporting $50 billion in accumulated losses over the last three years.

The Path Ahead: Strategic Pivots and Scenarios

In the short term, investors should expect "sticky" volatility. The Federal Reserve appears unwilling to commit to further deep cuts if the dollar remains weak enough to import inflation through higher commodity prices. Conversely, a dollar that is too strong could choke off the nascent recovery in manufacturing. Many multinational corporations are already executing strategic pivots, moving toward "regionalized supply chains" where production and sales happen within the same currency bloc to minimize exchange rate risk.

For the remainder of 2026, two primary scenarios emerge. In the first, the "V-shaped" recovery continues, with the DXY returning to the 100-105 range as the U.S. economy outperforms Europe and Japan, providing a headwind for S&P 500 earnings in the second half of the year. In the second scenario, a "policy rupture" occurs if trade tensions with major partners like the EU or China escalate further, potentially leading to a "flight to safety" that sends the dollar even higher, regardless of domestic economic health.

Summary of Market Outlook

The "Great Dollar Whipsaw" of early 2026 serves as a stark reminder that in a period of aggressive fiscal and trade policy, currency is the ultimate shock absorber. The move to a four-year low provided a brief earnings "sugar high" for the likes of Microsoft and Apple, but the structural challenges facing exporters like ADM and Deere & Co suggest that the broader economy is still struggling to find its footing in a high-tariff, high-volatility world.

Moving forward, the market will be hyper-focused on the 100.0 level on the DXY. If the index sustains a move above this mark, expect a renewed wave of earnings downgrades for multinationals later this year. Investors should keep a close eye on the "sticky" inflation data and any further "strong dollar" rhetoric from the Treasury, as these will be the primary signals for the next leg of this volatile journey.

This content is intended for informational purposes only and is not financial advice.